- IUL policies offer permanent life insurance with cash value growth tied to a stock market index — like the S&P 500 — giving you upside potential without direct market exposure.

- A built-in floor (usually 0%) means your cash value won’t decrease during a market downturn, but caps and participation rates limit how much you can earn in a strong bull market.

- IUL is especially powerful for high earners who’ve maxed out their 401(k) or IRA and need another tax-advantaged vehicle for long-term wealth building.

- Unlike term life, IUL lasts your entire life and builds real financial assets you can access while still alive — but it requires active management to stay effective.

- Keep reading to find out exactly who benefits most from IUL, and the one major drawback most agents won’t tell you upfront.

IUL Gives You Life Insurance and a Shot at Real Wealth Growth

“indexed universal life insurance …” from www.insure.com and used with no modifications.

Most life insurance policies do one thing — pay out when you die. Indexed universal life insurance (IUL) is built to do a lot more than that.

An IUL policy is a form of permanent life insurance that combines a guaranteed death benefit with a cash value component that can grow based on the performance of a stock market index. You get protection for your family and a financial asset that builds over time — all inside a single policy. For people serious about financial freedom, that dual function is exactly what makes IUL worth understanding deeply.

It sits in an interesting middle ground in the insurance world. It’s more flexible than whole life insurance, offers more downside protection than variable universal life (VUL), and goes far beyond what a standard universal life policy can do. But it’s also more complex than all of them — which is why most people either overlook it or misunderstand it entirely.

How Indexed Universal Life Insurance Actually Works

IUL works like any universal life policy at its core: you pay premiums, the insurer covers the cost of your death benefit, and whatever’s left over builds as cash value. What makes it different is how that cash value grows.

Where Your Premium Money Goes

Every premium payment you make gets split into two places. One portion covers the actual cost of insurance — this is what funds your death benefit payout. The remaining amount flows into your policy’s cash value account, where it has the opportunity to grow over time.

The cost of insurance isn’t fixed. It changes as you age, which means as you get older, more of your premium goes toward coverage and less feeds the cash value. This is one of the reasons IUL policies require active monitoring — the balance between cost of insurance and cash value growth shifts throughout the life of the policy.

How Cash Value Gets Tied to a Market Index

Your cash value doesn’t get invested directly into the stock market. Instead, your insurer credits interest to your account based on the performance of an index — most commonly the S&P 500, though some policies also offer Nasdaq 100, Russell 2000, or international index options. If you’re considering life insurance options, understanding accidental death and dismemberment insurance might also be beneficial.

This distinction matters enormously. Because you’re not actually in the market, you’re not exposed to direct investment losses. The index performance simply acts as a measuring stick for how much interest gets credited to your cash value during a given period — typically calculated annually. For those considering life insurance options, understanding the pros and cons of different policies can be crucial. Learn more about guaranteed issue life insurance to make informed decisions.

The Floor and Cap: Your Safety Net and Growth Limit

This is where IUL gets its defining characteristic. Every IUL policy sets a floor — the minimum interest rate credited to your account, regardless of market performance. Most policies set this at 0%, meaning in a year where the index drops 30%, your cash value stays flat instead of declining.

But that protection comes with a trade-off. Insurers also set a cap — the maximum rate of interest you can earn in a given period. If your policy has a 10% cap and the S&P 500 returns 24% that year, you only get credited 10%. The insurer keeps the difference, and that’s how they fund your downside protection. Some policies also use a participation rate — for example, at an 80% participation rate, a 15% index gain would only credit your account 12%.

| Feature | Whole Life | Universal Life | IUL | Variable UL (VUL) |

|---|---|---|---|---|

| Coverage Duration | Lifetime | Lifetime | Lifetime | Lifetime |

| Cash Value Growth | Fixed/Guaranteed | Insurer-set rate | Index-linked | Market-invested |

| Downside Protection | Yes | Yes | Yes (floor) | No |

| Upside Potential | Low | Low | Moderate | High |

| Premium Flexibility | Fixed | Flexible | Flexible | Flexible |

| Complexity | Low | Moderate | High | Very High |

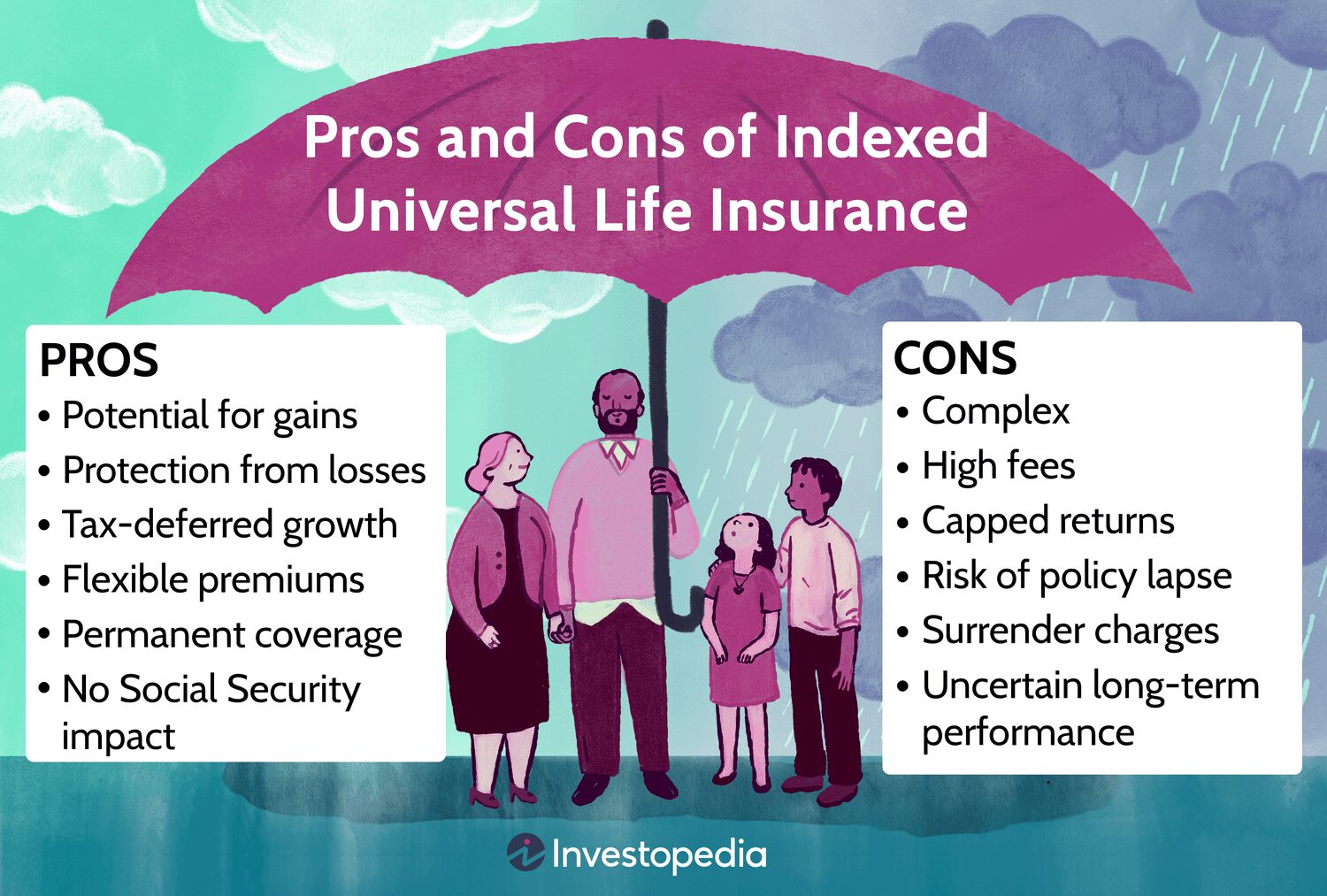

The Core Benefits of an IUL Policy

Understanding what an IUL can do for you — beyond the surface-level pitch — requires looking at each benefit in specific terms.

1. Lifelong Death Benefit Protection

Unlike term life insurance, which expires after 10, 20, or 30 years, an IUL policy is designed to last your entire life as long as the policy remains funded. Your beneficiaries receive the death benefit regardless of when you pass — whether that’s next year or 40 years from now. You can also adjust the death benefit amount over time as your financial situation evolves.

2. Flexible Premiums You Can Adjust Over Time

One of IUL’s most practical advantages is premium flexibility. Unlike whole life insurance with its rigid fixed payments, IUL allows you to raise or lower your premiums within certain limits — and in some cases, even skip payments temporarily if your cash value is sufficient to cover the cost of insurance.

This makes IUL useful for business owners and entrepreneurs whose income fluctuates year to year. In a strong income year, you can overfund the policy to accelerate cash value growth. In a leaner year, the policy can sustain itself without lapsing.

3. Tax-Deferred Cash Value Growth

The cash value inside an IUL policy grows on a tax-deferred basis — meaning you don’t owe taxes on the interest credited each year. Even better, when structured correctly, withdrawals and policy loans taken from the cash value can be accessed income-tax-free. This is a significant advantage over a traditional brokerage account or even a 401(k), where distributions in retirement are taxed as ordinary income.

4. Downside Protection With a Loss Floor

The floor is arguably IUL’s most compelling feature for risk-conscious investors. When the market index your policy tracks drops — even significantly — your cash value doesn’t follow it down. The 0% floor means the worst outcome in a bad market year is simply zero growth, not a loss. That’s a fundamentally different risk profile than any direct market investment.

Consider what happened during the 2008 financial crisis, when the S&P 500 dropped over 38% in a single year. An IUL policyholder with a 0% floor would have seen zero change to their cash value that year. Someone with a VUL policy or a standard brokerage account lost nearly 40% of their portfolio value. That protection compounds over time — you’re never recovering from a loss, which means your money starts each new crediting period from a higher base.

5. Access to Cash Value While You’re Still Alive

Your IUL policy’s cash value isn’t locked away until death. You can access it through withdrawals or policy loans while you’re still alive — and when structured properly, those distributions can be completely income-tax-free. This living benefit is one of the core reasons IUL shows up in serious retirement planning conversations. You’re building an asset you can actually use during your lifetime, not just leaving something behind.

Who Actually Benefits Most From an IUL Policy

“Why an Index Universal Life May be What …” from www.linkedin.com and used with no modifications.

IUL isn’t the right fit for everyone — and anyone who tells you otherwise is selling, not advising. But for the right financial profile, it’s one of the most versatile tools available.

High Earners Who Have Maxed Out Their 401(k) or IRA

If you’re already maxing out your 401(k) at $23,000 per year (2024 limit) and your Roth IRA at $7,000 — and you’re still looking for more tax-advantaged growth — IUL becomes a very serious option. There are no IRS contribution limits on how much you can put into a life insurance policy, which means high earners can funnel significant capital into a tax-sheltered, index-linked vehicle that also provides a death benefit. It’s one of the few remaining tools that offers tax-free access to growth without income restrictions.

People Who Want Permanent Coverage With Growth Potential

If your goal is lifelong coverage — not just protecting your family for the next 20 years — and you want that coverage to build financial value over time, IUL delivers both. Term life is cheaper, but it expires. Whole life is permanent, but its growth potential is limited and its premiums are rigid. IUL sits in the sweet spot for people who want flexibility, permanence, and the potential for meaningful cash value accumulation.

Business owners are another strong fit. IUL can be used for key person insurance, executive benefit plans, or as a component of a buy-sell agreement — all while building tax-deferred cash value that the business can access if needed. The flexibility of IUL premiums also aligns well with the variable cash flow reality of running a business.

The Real Drawbacks You Need to Know Before Buying

IUL has real, significant benefits — but it also has real, significant drawbacks that don’t always get the same airtime. Going in with eyes open is the only way to use this tool effectively.

Caps Limit How Much You Can Earn in a Bull Market

The same mechanism that protects your downside also limits your upside. When the market runs hot, your IUL policy won’t keep pace. In years like 2019 and 2021, when the S&P 500 returned over 28% and 26% respectively, an IUL policyholder with a 10% cap captured less than half of those gains.

Over a long bull market cycle, this cap drag can meaningfully reduce the total cash value you accumulate compared to a direct index investment. It’s not a reason to avoid IUL, but it is a reason to be clear about what you’re trading — you’re exchanging uncapped upside for guaranteed downside protection. That trade makes sense for some financial goals and not others.

Participation rates add another layer of complexity. Even if your policy has no stated cap, a participation rate below 100% achieves the same limiting effect. A policy with an 80% participation rate and no cap will credit you 80% of whatever the index returns — so a 20% index year only adds 16% to your cash value. Always evaluate both the cap and the participation rate when comparing IUL policies.

- Cap rate: The maximum interest rate credited in a given period, regardless of index performance above that level

- Participation rate: The percentage of index gains applied to your cash value — e.g., 80% participation on a 15% index return credits you 12%

- Spread/margin: Some policies subtract a percentage from the index return before crediting — a 3% spread on a 10% return credits only 7%

- Crediting period: Most IUL policies use annual point-to-point crediting, meaning only the start and end values of the index period count — intra-year volatility doesn’t help you

Fees and Charges Can Quietly Eat Into Your Cash Value

IUL policies carry multiple layers of fees — including premium load charges, administrative fees, cost of insurance charges, and surrender charges in the early years of the policy. These aren’t always easy to find in the policy illustration, but they can significantly impact how quickly your cash value grows, especially in the first 10 years. Always ask for a full fee breakdown before signing anything, and compare the internal rate of return net of all fees — not the gross crediting rate. For more information on life insurance options, consider exploring different policy types.

Active Management Is Required to Keep the Policy on Track

An IUL policy isn’t something you set up and forget. As the cost of insurance rises with age, the balance between premium, cash value, and death benefit needs regular review. If cash value growth underperforms projections — which can happen during prolonged low-return periods — the policy can become underfunded and eventually lapse. Working with a knowledgeable advisor who reviews your policy annually isn’t optional; it’s essential to making IUL work over the long term.

How to Use IUL as Part of a Broader Wealth Strategy

“The Power of IUL: Achu, Maxwell N …” from www.amazon.com and used with no modifications.

The most effective use of IUL isn’t as a standalone product — it’s as one component of a layered financial strategy. When you already have your emergency fund in place, your employer match captured in your 401(k), and your core investment accounts funded, IUL can serve as a powerful third or fourth layer of your wealth-building plan — adding tax-free growth potential, downside protection, and a permanent death benefit all in one vehicle.

Supplementing Retirement Income With Tax-Free Withdrawals

One of the most strategically powerful uses of IUL is as a tax-free income stream in retirement. Once your cash value has grown sufficiently, you can take policy loans against it — and unlike a 401(k) withdrawal or traditional IRA distribution, those loans are not considered taxable income by the IRS. This means you can create a retirement income stream that doesn’t push you into a higher tax bracket, doesn’t trigger additional taxation on your Social Security benefits, and doesn’t count against Medicare premium thresholds. For high earners planning retirement, that tax positioning alone can be worth tens of thousands of dollars over a 20-year retirement.

The key is proper policy design from the start. An IUL structured specifically for maximum cash value accumulation — rather than maximum death benefit — will have lower insurance costs, which means more of your premium goes to work building the asset you’ll eventually draw from. This is called a minimum non-MEC design, and it’s how advisors structure IUL policies intended for retirement income purposes. Getting this wrong at the policy level means you spend years building a less efficient vehicle, so the structure conversation with your advisor matters enormously before anything is signed.

Estate Planning and Wealth Transfer Goals

The death benefit in an IUL policy passes to your beneficiaries income-tax-free, making it one of the cleanest wealth transfer tools available. For individuals with taxable estates, an IUL policy held inside an irrevocable life insurance trust (ILIT) can keep the death benefit proceeds outside of the taxable estate entirely — protecting generational wealth from estate taxes that can currently reach up to 40%. Even outside of a trust structure, the direct beneficiary designation bypasses probate entirely, meaning your heirs receive the proceeds faster and without the legal fees and delays of the probate process.

IUL Is a Powerful Tool — In the Right Hands

“Indexed Universal Life Insurance” from www.investopedia.com and used with no modifications.

Indexed universal life insurance is not a magic solution, and it’s not right for every person or every financial situation. But for the right profile — high earner, long time horizon, permanent coverage need, and appetite for active financial management — it is one of the most versatile financial instruments available. You get a death benefit that lasts your entire life, cash value that grows without direct market exposure, downside protection through the floor mechanism, and the potential for tax-free income in retirement. That combination is genuinely difficult to replicate with any other single financial product.

The mistakes people make with IUL almost always come down to one of three things: buying it for the wrong reasons, structuring it poorly from the start, or failing to manage it actively over time. Approach it as a long-term financial strategy — not a quick fix or a sales pitch — and the benefits become very real. Ignore the complexity, and the fees and underperformance will quietly erode everything you were trying to build. The tool is powerful. What matters is whether you’re using it with precision.

Frequently Asked Questions

Here are the most common questions people ask when evaluating indexed universal life insurance for the first time.

What is the main difference between IUL and whole life insurance?

The main difference between IUL and whole life insurance comes down to flexibility and how cash value grows. Whole life offers fixed premiums, a guaranteed death benefit, and a guaranteed rate of cash value growth set by the insurer. IUL, by contrast, offers flexible premiums, an adjustable death benefit, and cash value growth tied to a market index rather than a guaranteed fixed rate. If you’re considering life insurance options, it’s important to understand the pros and cons of guaranteed issue life insurance as well.

Whole life is simpler and more predictable — premiums don’t change, growth is guaranteed, and there’s very little active management required. IUL has higher growth potential in favorable market conditions, but that growth is not guaranteed. The floor protects against losses, but caps and participation rates limit the upside, and the overall performance is far less certain than whole life’s guaranteed crediting.

For someone who values certainty above all else, whole life is the better fit. For someone who wants flexibility and is willing to manage the policy actively in exchange for higher growth potential, IUL becomes the stronger option. The right choice depends entirely on your financial goals, risk tolerance, and how involved you’re willing to be in managing a financial product over decades. If you’re considering life insurance options, it’s important to know at what age you should stop buying life insurance to make the best decision for your future.

Can you lose money with an indexed universal life insurance policy?

Your cash value won’t decrease due to market index losses — the 0% floor prevents that. However, you can absolutely lose money in an IUL policy in a different way: if the policy fees, cost of insurance charges, and administrative expenses exceed the interest being credited to your account, your cash value will decline. This is especially common in the early years of the policy when surrender charges are still active, or in later years when the rising cost of insurance outpaces cash value growth. If the policy becomes severely underfunded, it can lapse entirely — meaning you lose your coverage and potentially face a tax bill on any gains that were sheltered inside the policy.

Is IUL a good retirement strategy?

IUL can be an excellent retirement strategy — but only as a complement to, not a replacement for, traditional retirement accounts. The conventional guidance is to first capture any employer 401(k) match, then max out a Roth IRA if eligible, then max out your 401(k) or other qualified accounts. Only after those steps does IUL make sense as an additional retirement vehicle for most people.

Where IUL genuinely shines in retirement planning is for high earners who have already maxed out every other tax-advantaged option. At that point, IUL offers a tax-deferred growth environment with tax-free access in retirement — something neither a traditional brokerage account nor a taxable savings account can match. Used in this context, with a properly structured policy and consistent funding over 20 or more years, IUL can generate a meaningful, tax-efficient income stream in retirement that complements Social Security and qualified plan distributions.

What happens to IUL cash value when you die?

In most standard IUL policies, the accumulated cash value does not pass to your beneficiaries separately — instead, the insurer pays out the death benefit, and the cash value is effectively absorbed into that payout. Your beneficiaries receive the face value of the death benefit, not the death benefit plus the cash value. This is one of the most misunderstood aspects of permanent life insurance. Some policies offer a return of cash value rider that allows both amounts to be paid out, but this option increases the cost of insurance and should be weighed carefully against the added expense.

How much does an IUL policy typically cost?

IUL policy costs vary widely based on your age at issue, health status, the amount of death benefit you select, and how aggressively you fund the cash value component. A healthy 35-year-old might pay anywhere from $500 to $1,500 or more per month for a well-structured IUL policy designed for both meaningful death benefit coverage and significant cash value accumulation. Older applicants or those with health conditions will face higher cost-of-insurance charges, which reduces the efficiency of the policy for cash value building purposes. For more detailed information, you can explore Nerdwallet’s guide on indexed universal life insurance.

It’s also important to understand that not all of your premium represents “cost” in the traditional sense. With IUL, a significant portion of your premium payment goes directly into your cash value account — it’s building an asset, not just paying for protection. The true cost of the policy is the sum of the insurance charges and fees, not the total premium. That said, those internal charges can be substantial and should be scrutinized carefully through a full policy illustration before you commit.

Key IUL Cost Factors at a Glance:

- Age at issue: Younger applicants face lower cost-of-insurance charges, making early policy initiation significantly more efficient for long-term cash value growth

- Health classification: Preferred health ratings reduce insurance costs and leave more premium available for cash value accumulation

- Death benefit amount: Higher face value means higher cost of insurance — minimum non-MEC designs reduce the death benefit to maximize cash value efficiency

- Premium funding level: Overfunding the policy (up to MEC limits) accelerates cash value growth and improves long-term performance

- Policy fees: Administrative charges, premium loads, and surrender charges vary significantly between insurers — always compare net internal rates of return, not just crediting rates

The single most important step before purchasing any IUL policy is requesting a detailed policy illustration that shows projected values under multiple crediting scenarios — typically a guaranteed scenario (0% crediting), a mid-point scenario, and a current assumption scenario. This gives you a realistic range of outcomes and lets you stress-test whether the policy still works for your goals in a low-return environment. Never evaluate an IUL policy based solely on the optimistic illustration — always look at what happens if the index consistently returns modest gains or even nothing at all for extended periods.

If you’re serious about building financial freedom through tax-efficient strategies and permanent protection, connect with a financial professional who specializes in IUL structuring — the difference between a well-designed policy and a poorly structured one can be hundreds of thousands of dollars over the life of the contract.

Looking for life insurance that fits your family’s needs?

Contact Ranwell Insurance today at (855) 508-5008 or request a free personalized quote. We help families compare life insurance options and choose coverage with confidence.

Reviewed by Ranwell Insurance

Licensed Insurance Agency

Georgia License #: GID276-EN

Ranwell Insurance provides educational guidance on life insurance, final expense insurance, mortgage protection, retirement planning, and related coverage options.

Last Reviewed: May 2026

Contact: (855) 508-5008

Disclosure: Insurance products, rates, and eligibility requirements vary by carrier and state. Information is provided for educational purposes only. Please see our Editorial Policy for more information.