- Variable life insurance combines lifelong coverage with an investment component — your cash value grows (or shrinks) based on how your chosen subaccounts perform in the market.

- Premium payments are split three ways: a portion covers the death benefit, a portion goes to the insurer, and the rest is invested in subaccounts similar to mutual funds.

- Cash value growth is tax-deferred, and the death benefit paid to your beneficiaries is generally free from federal income tax.

- This policy costs more than term life insurance — but for the right person, the investment flexibility and lifelong protection can make it worth every dollar.

- Keep reading to find out if variable life insurance fits your risk tolerance, financial goals, and long-term wealth strategy — including a side-by-side comparison with variable universal life insurance.

Variable life insurance is one of those policies that can either be a powerful financial tool or a costly mistake — and which one it becomes depends entirely on how well you understand it before signing.

Ranwell Insurance has been helping people navigate permanent life insurance decisions for decades, and variable life consistently ranks among the most misunderstood products in the market. That’s not because it’s bad — it’s because it demands more from the policyholder than a standard whole or term policy ever would.

Variable Life Insurance Offers Growth Potential — With Strings Attached

“Variable Universal Life Insurance …” from www.jrcinsurancegroup.com and used with no modifications.

Variable life insurance sits in a unique category. It’s permanent, meaning it doesn’t expire after 10, 20, or 30 years like term coverage. But unlike whole life insurance, where the insurer controls how your cash value grows at a modest guaranteed rate, variable life hands that control — and the risk — directly to you.

What Variable Life Insurance Actually Is

Variable life insurance is a type of permanent life insurance policy that includes both a death benefit and a cash value component that you can invest in a range of subaccount options. Those subaccounts function similarly to mutual funds, and they can include equity portfolios, bond portfolios, and money market options. The value of your policy’s cash component — and in some cases the death benefit itself — can rise or fall depending on how those investments perform. If you’re wondering at what age you should stop buying life insurance, it’s important to consider how your needs may change over time.

What makes it “variable” is exactly that: the performance isn’t fixed or guaranteed. You’re taking on investment risk in exchange for higher growth potential. That’s the trade-off at the core of every variable life policy.

How Cash Value Works in a Variable Policy

When you pay your premium, that money doesn’t go into one pool. It gets divided, with one portion covering the cost of your death benefit protection, another covering insurer fees and administrative costs, and the remainder flowing into your chosen subaccounts. Over time, if those subaccounts perform well, your cash value grows — and it does so on a tax-deferred basis, meaning you won’t owe taxes on gains until you withdraw them. For more information on life insurance options, you can explore Ranwell Insurance’s offerings.

Some policies also include a fixed account option alongside the variable subaccounts. The fixed account offers a set interest rate determined by the insurer — lower growth potential, but no market exposure. This gives policyholders a way to balance risk within the same policy. For those considering life insurance options, Ranwell Insurance offers a variety of plans to suit different needs.

If you borrow against your cash value, those loan proceeds are generally not considered taxable income. That’s a meaningful advantage for policyholders who want to access funds without triggering a tax event — something a standard brokerage account can’t offer.

Here’s a quick look at how the cash value component compares across permanent life insurance types:

| Policy Type | Cash Value Growth | Investment Control | Risk Level |

|---|---|---|---|

| Whole Life | Fixed, guaranteed rate | None | Low |

| Universal Life | Tied to interest rates | Minimal | Low to Medium |

| Variable Life | Tied to subaccount performance | High | Medium to High |

| Variable Universal Life | Tied to subaccount performance | High | Medium to High |

Why This Policy Costs More Than Term Coverage

Variable life insurance carries higher premiums than term policies with the same death benefit — and higher fees overall. You’re paying for permanent coverage, investment access, and the administrative structure that supports subaccount management. For policyholders who use those features strategically, the higher cost is justifiable. For those who don’t, it can become an expensive policy that underperforms simpler alternatives.

How Variable Life Insurance Builds Cash Value

Understanding how your money actually moves inside a variable life policy is key to making it work for you. The mechanics are straightforward once you break them down. For more insights, you can explore how Ranwell Insurance serves as a trusted life insurance expert in the Southeast.

How Premium Payments Get Split Into Three Buckets

Every time you make a premium payment, the insurer divides it into three distinct portions. The first covers the pure cost of insurance — the death benefit. The second covers the insurer’s operational expenses and any policy fees. The third, and the portion that most policyholders care about, is directed into the subaccounts you’ve selected.

How much lands in each bucket depends on your policy’s structure, your age, the size of your death benefit, and the fees built into the contract. Early in the policy’s life, more of your premium tends to go toward insurance costs. Over time — assuming consistent payments — the investment portion begins to accumulate meaningfully.

What Are Subaccounts and How Do They Work

Subaccounts are the investment vehicles inside your variable life policy. They work similarly to mutual funds — each one holds a diversified portfolio of assets such as stocks, bonds, or money market instruments. You choose which subaccounts to allocate your cash value to, and you can typically shift allocations over time as your risk tolerance or goals change.

Most variable life policies offer a range of subaccounts across different asset classes and risk profiles. A policyholder comfortable with higher risk might allocate heavily toward equity-based subaccounts. Someone approaching retirement might shift toward bond or money market subaccounts to preserve value.

Tax-Deferred Growth on Cash Value

One of the most practical advantages of variable life insurance is the tax treatment of your cash value growth. Any gains inside your policy accumulate on a tax-deferred basis — you don’t owe taxes on investment growth each year the way you would with a standard taxable brokerage account. This allows your cash value to compound more efficiently over time, since no portion is being carved out annually for taxes.

Variable Life Insurance vs. Variable Universal Life Insurance

“Variable Universal Life Insurance …” from www.investopedia.com and used with no modifications.

These two policies are closely related, but they’re not the same — and the differences matter depending on how much flexibility you want over your premiums and death benefit structure.

Variable life insurance has a fixed premium structure. You pay a set amount on a set schedule, and in return you receive a guaranteed minimum death benefit. Variable universal life insurance, by contrast, gives you the ability to adjust both your premium payments and your death benefit over time. That added flexibility comes with added complexity, and it places more responsibility on the policyholder to actively manage the policy to keep it in force.

Fixed vs. Flexible Premium Payments

With a standard variable life policy, your premium is locked in. That predictability can actually be an advantage — it removes the temptation to underfund the policy during market downturns, which is a common mistake with variable universal life policies that can lead to lapse. Variable universal life lets you pay more when you have extra cash and less when finances are tight, but underpaying when markets are down can erode your cash value faster than you might expect.

Death Benefit Differences Between the Two

Variable life insurance provides a guaranteed minimum death benefit that won’t drop below a set floor, regardless of how your subaccounts perform. Variable universal life insurance may offer the potential for a higher death benefit if your investments perform well, but without that same guaranteed floor in all cases. For policyholders who want the investment upside but need certainty around the death benefit their family will receive, standard variable life insurance offers more protection on that specific point.

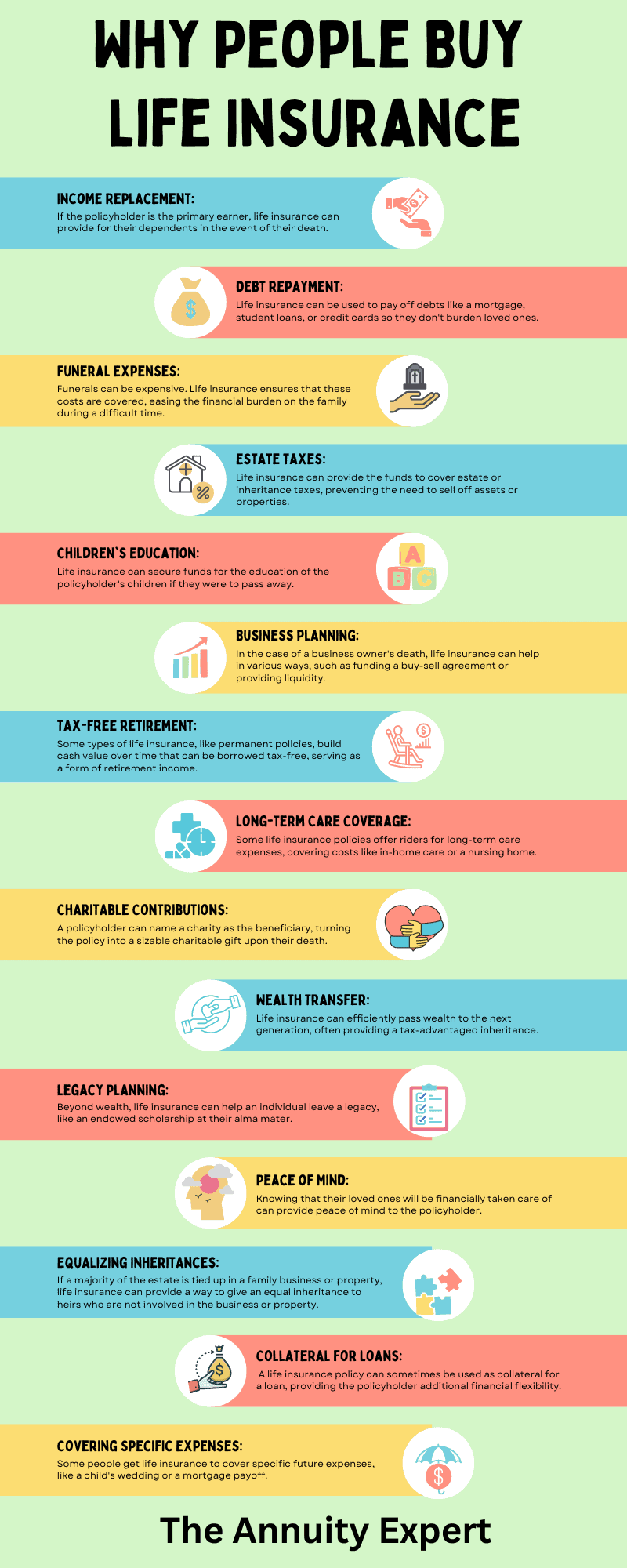

Benefits of Variable Life Insurance

“Variable Life Insurance: How It Works …” from www.westernsouthern.com and used with no modifications.

For the right policyholder, variable life insurance offers a combination of advantages that no other single financial product can fully replicate. The key is knowing which benefits are most relevant to your situation.

Lifelong Coverage With No Expiry Date

Unlike term life insurance, which covers you for a defined period and then expires, variable life insurance is permanent. As long as your premiums are paid and your policy remains in force, your beneficiaries will receive the death benefit whenever you pass — whether that’s in 10 years or 40. That certainty has real value, especially for those with long-term dependents, estate planning needs, or business succession arrangements.

Greater Control Over Investment Choices

Variable life insurance gives you direct input into how your cash value is invested — a level of control that whole life and universal life policies simply don’t offer. Instead of accepting whatever return the insurer credits to your account, you choose your own subaccount allocations based on your financial goals and risk tolerance.

This matters because investment performance compounds over decades. A cash value growing at a higher rate inside a tax-deferred account can accumulate significantly more than one tied to a modest guaranteed interest rate — provided the markets cooperate and the policyholder makes informed allocation decisions.

Most variable life policies offer a broad menu of subaccount options across different asset classes:

- Equity subaccounts — invested in stock portfolios, offering higher growth potential with more volatility

- Bond subaccounts — invested in fixed-income securities, offering more stability with lower return potential

- Money market subaccounts — the most conservative option, prioritizing capital preservation

- Fixed account options — a set interest rate determined by the insurer, separate from market performance

- Balanced or blended subaccounts — a mix of equities and bonds for moderate risk and return

Death Benefit Is Generally Tax-Free for Beneficiaries

When your beneficiaries receive the death benefit from a variable life insurance policy, that payout is generally not subject to federal income tax. This is one of the most significant advantages of life insurance as a financial instrument — the full benefit passes to your family without being reduced by a tax bill at what is already a difficult time.

Combined with the tax-deferred growth on cash value and the ability to take policy loans without triggering a taxable event, variable life insurance offers a layered set of tax advantages that make it attractive as part of a broader wealth strategy — not just as pure protection.

Policy Riders That Add Extra Protection

Many variable life insurance policies can be enhanced with optional riders — add-ons that expand your coverage or add features beyond the base policy. Common riders include accelerated death benefit provisions, which allow you to access a portion of the death benefit early if you’re diagnosed with a terminal illness, and no-lapse guarantee riders, which protect the policy from lapsing even if the cash value drops to zero due to poor market performance.

Other riders may allow for additional purchase of coverage without new medical underwriting, or provide a waiver of premium benefit if you become disabled and can no longer make payments. Each rider comes with an added cost, but for many policyholders, the protection they provide is well worth factoring into the overall policy design.

The Real Risks You Need to Know

“The Benefits of Life Insurance & Why to …” from www.newyorklife.com and used with no modifications.

Variable life insurance is not the right fit for everyone, and glossing over its risks would be doing you a disservice. The same features that make it attractive — investment control, growth potential — also introduce real financial exposure that other permanent policies don’t carry.

The most significant risk is straightforward: your subaccounts can lose value. If the market drops sharply, your cash value drops with it. Unlike whole life insurance where the cash value grows at a guaranteed rate, variable life offers no such floor on investment performance. A sustained market downturn can meaningfully reduce your cash value, and in extreme cases, it can threaten the policy’s ability to stay in force if the cash value falls too low to cover ongoing insurance costs.

Market Losses Can Reduce Your Cash Value

When the market falls, your subaccounts fall with it — and there’s no guaranteed floor to catch your cash value the way there is with whole life insurance. A prolonged downturn can strip away years of accumulated growth, and if the cash value drops low enough to no longer cover the cost of insurance, your policy could lapse entirely. This isn’t a hypothetical edge case. It’s a real outcome that has happened to policyholders who didn’t monitor their allocations or who over-weighted equity subaccounts without a plan for volatility.

Higher Fees and Policy Complexity

Variable life insurance comes with a layered fee structure that can quietly eat into your returns if you’re not paying attention. Beyond the standard cost of insurance, you’re typically looking at mortality and expense risk charges, administrative fees, and the underlying expense ratios of each subaccount — which mirror the fees you’d pay inside a mutual fund. Some subaccounts carry expense ratios well above 1%, and when stacked with policy-level charges, the total cost drag on your cash value can be substantial. This is one of the core reasons why variable life insurance works best for policyholders who actively engage with their policy rather than set it and forget it.

Who Should Consider Variable Life Insurance

“Variable Life Insurance: Quotes …” from www.annuityexpertadvice.com and used with no modifications.

Variable life insurance makes the most sense for a specific type of person. If you have a long investment horizon, a genuine comfort with market risk, a need for permanent life insurance coverage, and a desire to grow wealth inside a tax-advantaged structure, variable life is worth serious consideration. It tends to be a strong fit for high-income earners who have maxed out contributions to traditional retirement accounts like 401(k)s and IRAs and are looking for additional tax-deferred growth vehicles. It also works well for those with estate planning goals who need a guaranteed death benefit alongside long-term wealth accumulation.

On the other hand, if you’re primarily looking for affordable protection, a straightforward term policy will almost always be the better choice. And if you want permanent coverage with cash value but don’t want to manage investment risk, whole life or standard universal life insurance will serve you better. Variable life insurance rewards those who understand it and engage with it — and it can underperform for those who don’t.

Frequently Asked Questions

Here are the most common questions people ask about variable life insurance benefits, answered directly and without the jargon.

What Investment Options Are Available in Variable Life Insurance?

Variable life insurance policies typically offer a menu of subaccounts that span multiple asset classes. The specific options vary by insurer, but most policies include equity-based subaccounts invested in domestic and international stock portfolios, fixed-income subaccounts invested in government or corporate bond portfolios, and money market subaccounts focused on capital preservation.

Many policies also include a fixed account option that sits outside the variable subaccounts entirely. The fixed account credits a set interest rate determined by the insurer, offering a stable, lower-risk option for a portion of your cash value. This is particularly useful for policyholders who want to reduce market exposure as they get older or as their financial goals shift.

The ability to reallocate between subaccounts over time — typically at no direct cost and sometimes with restrictions on frequency — gives policyholders meaningful control over how aggressively or conservatively their cash value is managed throughout the life of the policy. For more insights on managing life insurance policies, consider reading about Ranwell Insurance, trusted life insurance experts serving the Southeast.

Can You Borrow Against a Variable Life Insurance Policy?

Yes. Once your policy has accumulated sufficient cash value, you can borrow against it. Policy loans from a variable life insurance policy are generally not considered taxable income at the time you receive them, which makes them a useful tool for accessing funds without triggering a tax event — unlike withdrawing from a brokerage account or taking an early distribution from a retirement account.

However, unpaid policy loans accrue interest and reduce your death benefit if not repaid. If the loan balance grows large enough relative to your cash value — especially during a market downturn that has already reduced the account — it can put the policy at risk of lapsing. Any outstanding loan balance at the time of lapse could then be treated as taxable income. Borrowing against your policy is a legitimate strategy, but it requires careful management.

What Happens to Cash Value if the Market Drops?

If the market drops, the value of your subaccounts drops with it, and your cash value decreases accordingly. Variable life insurance does not guarantee a minimum return on the investment component of your policy. A significant or prolonged market decline can substantially reduce your cash value, and if it falls below the amount needed to cover ongoing insurance costs, your policy could lapse unless you make additional premium payments. This is why monitoring your policy’s performance and maintaining an appropriate subaccount allocation for your risk tolerance is essential — not optional.

Is Variable Life Insurance a Good Investment?

Variable life insurance is not a pure investment — it’s a life insurance policy with an investment component, and that distinction matters. The fees embedded in a variable life policy are higher than what you’d pay investing directly in mutual funds through a brokerage account. However, the tax-deferred growth on cash value and the tax-free death benefit create advantages that a standard investment account doesn’t offer. To understand more about how this type of insurance works, you can read this detailed guide on variable life insurance.

For high-income earners who have already maximized contributions to tax-advantaged retirement accounts, variable life insurance can serve as an additional layer of tax-efficient growth with the added benefit of permanent life insurance coverage. For someone who simply wants to invest, lower-cost vehicles will almost always outperform on a net-return basis. The value of variable life insurance lies in what it does as a combined insurance and financial planning tool — not as a standalone investment.

How Does a No-Lapse Guarantee Work in Variable Life Insurance?

A no-lapse guarantee is an optional rider available on some variable life insurance policies that prevents the policy from lapsing even if the cash value drops to zero — provided certain premium payment conditions are met. Without this rider, a policy can lapse if poor market performance depletes the cash value to the point where it can no longer cover the cost of insurance.

With the no-lapse guarantee in place, the insurer contractually agrees to keep the policy in force for a specified period — sometimes the life of the insured — as long as the required minimum premium is paid on time. This offers a meaningful safety net for policyholders who are concerned about market volatility threatening their coverage.

The rider does come at an additional cost, and the terms vary significantly between insurers. Some no-lapse guarantees are ironclad for life; others apply only for a defined period such as 20 years. Reading the fine print on this rider before purchasing is important, particularly understanding what happens to the guarantee if you miss a payment or take a policy loan.

For those who want the investment flexibility of variable life insurance but need certainty that their death benefit will be there for their family regardless of market conditions, the no-lapse guarantee rider is one of the most practical protections available. Western & Southern Financial Group offers personalized guidance to help you evaluate whether this and other policy features align with your long-term financial goals. Additionally, for those exploring options in the Southeast, Ranwell Insurance provides trusted life insurance expertise.

Looking for life insurance that fits your family’s needs?

Contact Ranwell Insurance today at (855) 508-5008 or request a free personalized quote. We help families compare life insurance options and choose coverage with confidence.

Reviewed by Ranwell Insurance

Licensed Insurance Agency

Georgia License #: GID276-EN

Ranwell Insurance provides educational guidance on life insurance, final expense insurance, mortgage protection, retirement planning, and related coverage options.

Last Reviewed: April 2026

Contact: (855) 508-5008

Disclosure: Insurance products, rates, and eligibility requirements vary by carrier and state. Information is provided for educational purposes only. Please see our Editorial Policy for more information.