- Universal life insurance offers lifelong coverage with flexible premiums and an adjustable death benefit — making it one of the most adaptable policies available.

- The built-in cash value component grows tax-deferred over time, giving you a financial resource you can borrow against during your lifetime.

- Unlike whole life insurance, universal life does not guarantee a fixed return on your cash value, which introduces both opportunity and risk depending on market conditions.

- Policy lapse is a real danger if premiums fall too low and the cash value can’t cover the shortfall — understanding this risk could save your coverage.

- Not everyone benefits equally from universal life insurance — keep reading to find out if your financial situation makes it the right fit.

Universal life insurance is one of the most flexible financial tools you can own — but flexibility without understanding can cost you everything.

For anyone serious about long-term financial security, understanding how this type of policy works is not optional. Protecting your family’s financial future starts with knowing exactly what your policy does and does not guarantee. Universal life insurance sits in a unique space — it combines permanent life insurance coverage with a savings component that can grow over time, all while letting you adjust how much you pay and how much your beneficiaries receive.

Universal Life Insurance Gives You Lifelong Coverage With a Built-In Savings Account

“Universal Life Insurance – Ramsey” from www.ramseysolutions.com and used with no modifications.

Universal life insurance is a type of permanent life insurance, meaning it does not expire after a set term. As long as you meet the minimum premium requirements, your coverage stays active for the rest of your life. What makes it stand out from a basic term policy is the cash value account attached to it — a savings component that builds over time on a tax-deferred basis.

How the Cash Value Component Works

Every premium payment you make gets split into two parts. One portion covers the actual cost of your insurance — what insurers call the cost of insurance (COI). The remainder flows into your cash value account, where it earns interest based on current market rates or a minimum rate set by the insurer. Over time, this account can grow into a meaningful financial asset.

The cash value is not just a number on paper. You can borrow against it, use it to cover premium payments, or surrender the policy entirely and receive the accumulated value. This is what separates universal life insurance from term policies, which offer no such financial return if you outlive the coverage period.

Why Flexibility in Premiums Matters

One of the most practical advantages of universal life insurance is the ability to adjust your premium payments within certain limits. If your income drops one year, you may be able to reduce your payment or skip it entirely — provided your cash value is sufficient to cover the cost of insurance. Conversely, if you come into extra income, you can overfund the policy and accelerate cash value growth.

This flexibility is a genuine differentiator. Most financial products lock you into rigid payment schedules. Universal life gives you room to adapt your policy to your life — not the other way around.

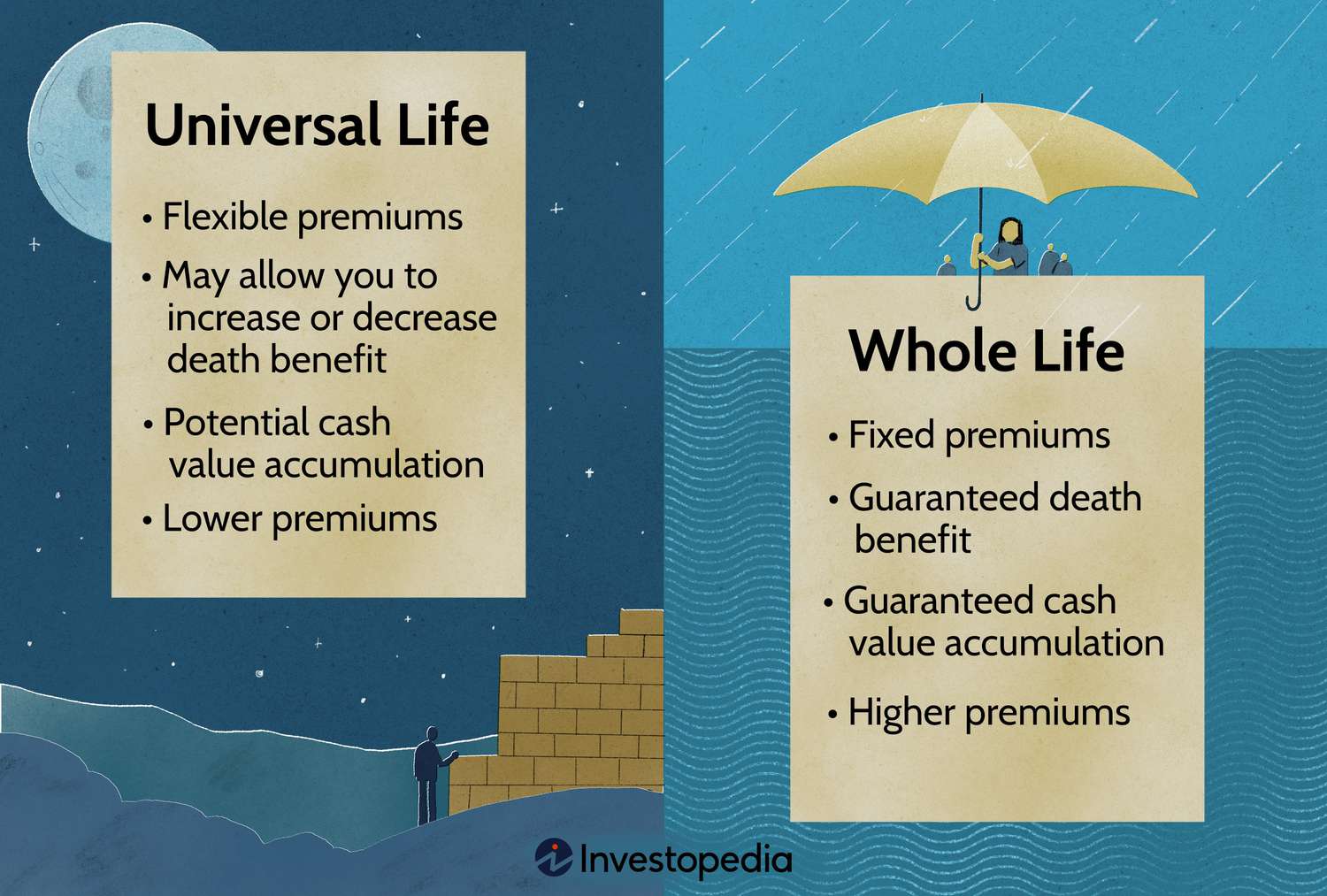

How Universal Life Insurance Differs From Whole Life Insurance

“Universal Life vs. Whole Life Insurance …” from www.investopedia.com and used with no modifications.

Both universal life and whole life insurance are permanent policies, but they operate very differently. Whole life is built on guarantees — fixed premiums, a guaranteed death benefit, and a guaranteed minimum cash value growth rate. Universal life trades some of those guarantees for flexibility, which can work in your favor or against you depending on how the policy is managed.

The core difference comes down to certainty versus adaptability. Whole life is predictable by design. Universal life is adjustable by design. Neither is universally better — it depends entirely on your financial goals and how actively you want to manage your coverage.

Guaranteed vs. Non-Guaranteed Returns

Whole life insurance policies include a guaranteed minimum return on the cash value — your money grows at a set rate no matter what. Universal life insurance does not offer this same guarantee. The cash value earns interest based on rates that can fluctuate, which means your account could grow faster during high-rate environments or slower when rates drop.

Fixed vs. Adjustable Premiums

Feature Whole Life Insurance Universal Life Insurance Premiums Fixed — same payment every period Flexible — can be adjusted within limits Cash Value Growth Guaranteed minimum rate Variable — tied to market or declared rates Death Benefit Fixed amount Adjustable — can increase or decrease Policy Risk Low — insurer bears most risk Higher — policyholder bears more risk Surrender Value Yes, with guaranteed amounts Yes, based on accumulated cash value

Fixed premiums in whole life insurance make budgeting straightforward. You know exactly what you owe every month, every year, for the life of the policy. Universal life insurance removes that certainty in exchange for control. You decide how much to pay — within your insurer’s defined minimum and maximum — which means your policy’s performance depends in part on the decisions you make over time.

Death Benefit Differences

In a whole life policy, the death benefit is set at the time the policy is issued and does not change. Universal life insurance allows you to increase or decrease your death benefit after the policy is in force, subject to insurer approval and, in the case of increases, potentially new underwriting. This gives policyholders the ability to scale coverage as their financial responsibilities grow or shrink over time.

The Core Benefits of Universal Life Insurance

The benefits of universal life insurance are most valuable when the policy is understood and actively managed. Passive ownership — paying premiums and never reviewing the policy — is one of the most common mistakes policyholders make and one of the leading causes of unexpected lapses.

When managed correctly, universal life insurance delivers several advantages that few other financial products can match simultaneously.

Benefit What It Means for You Tax-Deferred Cash Value Growth Your cash value grows without annual tax liability until withdrawal Policy Loans Borrow against cash value without a credit check or tax penalty (if structured correctly) Adjustable Death Benefit Scale your coverage up or down as your life changes Flexible Premiums Adapt payments to match your cash flow without losing coverage Policy Surrender Option Access accumulated cash value if you no longer need coverage

Tax-Deferred Cash Value Growth

The cash value inside a universal life insurance policy grows on a tax-deferred basis, meaning you do not owe income tax on the interest earned each year it stays inside the policy. This is a significant advantage compared to a standard savings account or taxable investment account, where earnings are reported and taxed annually. Over decades, the compounding effect of tax-deferred growth can result in substantially more accumulated value than a comparable taxable account.

It is important to understand that taxes are deferred, not eliminated. If you withdraw more than your basis — the total amount of premiums you have paid in — the excess is taxable as ordinary income. However, structured correctly, a universal life policy can be an efficient vehicle for building long-term, accessible wealth alongside your death benefit coverage.

Ability to Borrow Against Your Policy

Once your cash value has accumulated, you can borrow against it without going through a credit check or approval process. Policy loans from a universal life insurance policy are not considered taxable income as long as the policy remains in force. This makes them a uniquely accessible source of funds during financial hardship, major purchases, or investment opportunities — without triggering a tax event.

The critical detail here is that unpaid loans accrue interest and reduce your death benefit if they remain outstanding at the time of your death. If a loan — combined with accrued interest — causes your cash value to drop to zero, the policy could lapse, and any outstanding loan balance may then become taxable. Borrowing against your policy is a powerful tool, but it requires careful management.

Adjustable Death Benefits

Life changes, and your death benefit should be able to change with it. Universal life insurance allows you to request a decrease in your death benefit at virtually any time, which can lower your cost of insurance and free up more of your premium to build cash value. Increasing your death benefit is also possible, though it typically requires evidence of insurability — meaning the insurer may ask for updated health information before approving the change. For seniors in Georgia, understanding life insurance options to cover medical debt can be crucial.

Policy Surrender Options

If you reach a point where you no longer need life insurance coverage, you can surrender your universal life policy and receive the accumulated cash value — minus any surrender charges that may apply, particularly in the early years of the policy. This is called the cash surrender value, and it represents a financial return that term life insurance simply cannot offer.

Surrender charges are an important cost to understand before you sign. Many universal life policies carry surrender periods of 10 to 15 years during which accessing the full cash value will result in a fee. These charges typically decrease over time and eventually disappear, but exiting a policy early can significantly reduce what you receive. For more information on life insurance options, consider reading about Ranwell Insurance.

The Risks You Need to Know Before You Sign

“Indexed Universal Life Insurance” from www.investopedia.com and used with no modifications.

Universal life insurance is not a set-it-and-forget-it product. The same flexibility that makes it appealing also introduces risks that whole life insurance does not carry. Understanding these risks upfront is what separates policyholders who get lasting value from those who end up with a lapsed policy and nothing to show for years of premium payments.

The three primary risk areas are return uncertainty, premium shortfalls, and policy lapse. Each one is manageable — but only if you know they exist and actively monitor your policy over time.

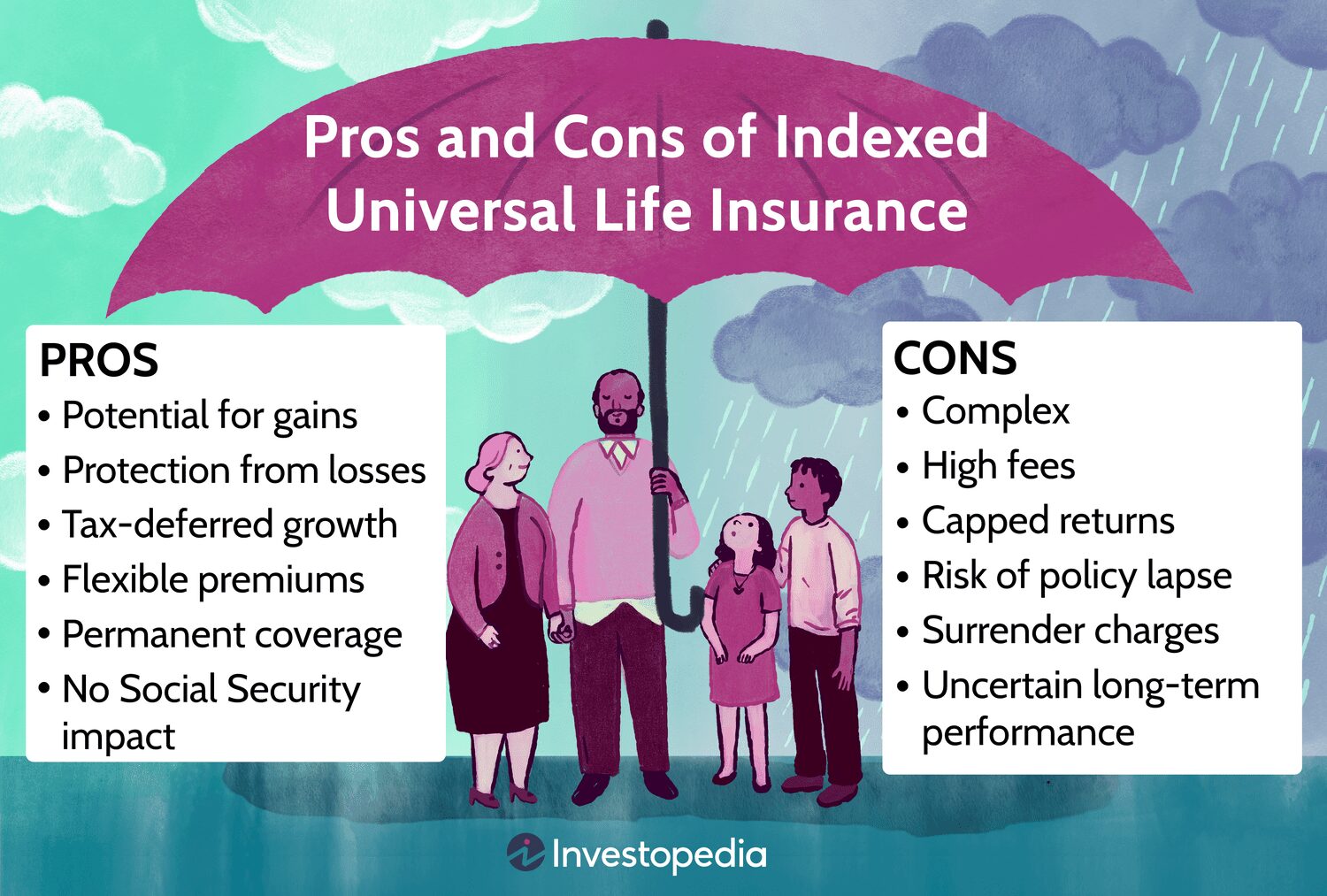

No Guaranteed Return on Investment

The cash value in a universal life insurance policy earns interest based on rates that are not fixed. Traditional universal life policies credit interest based on a declared rate set by the insurer, which can fluctuate with market conditions. While most policies include a minimum guaranteed interest rate — often around 2% — that floor may not be enough to keep the policy performing as originally illustrated if rates stay low for extended periods.

This stands in direct contrast to whole life insurance, where the growth rate on cash value is guaranteed regardless of external conditions. With universal life, the policyholder absorbs more of the performance risk. If you purchase a policy based on an illustration showing 5% annual growth and actual credited rates average 2.5%, your cash value will be significantly lower than projected — potentially leaving your policy underfunded.

Indexed universal life (IUL) and variable universal life (VUL) policies introduce additional complexity. IUL policies link cash value growth to a stock market index like the S&P 500, with caps on gains and floors on losses. VUL policies invest directly in sub-accounts similar to mutual funds, with full exposure to market upside and downside. Both offer higher growth potential than traditional universal life, but they come with correspondingly higher risk profiles.

Policy Lapse Risks When Premiums Fall Short

One of the most misunderstood aspects of universal life insurance is how a policy can lapse even after years of premium payments. Because premiums are flexible, policyholders sometimes reduce or skip payments assuming the cash value will cover the difference. If the cash value is insufficient to cover the monthly cost of insurance — which increases as the insured gets older — the policy will eventually lapse, terminating coverage entirely.

Some policies include a no-lapse guarantee rider that prevents the policy from lapsing for a defined period as long as a minimum premium is paid, regardless of cash value performance. This rider adds a layer of protection but typically comes at an additional cost. Without it, policyholders need to regularly review in-force illustrations — updated projections of how the policy will perform based on current assumptions — to ensure the policy remains on track.

How State and Federal Regulations Protect You

Universal life insurance policies are regulated at the state level, with each state setting its own requirements for how insurers must notify policyholders about potential lapses, grace periods, and changes to policy terms. Most states require insurers to provide advance written notice before a policy lapses, giving you a window to make a corrective payment and keep your coverage active.

At the federal level, the tax treatment of life insurance — including the tax-deferred growth of cash value and the income-tax-free nature of death benefits — is governed by the Internal Revenue Code. Specifically, policies must meet the definition of life insurance under IRC Section 7702, which sets limits on how much cash value a policy can accumulate relative to the death benefit. Policies that exceed these limits lose their tax-advantaged status and are reclassified as modified endowment contracts (MECs), which changes how loans and withdrawals are taxed.

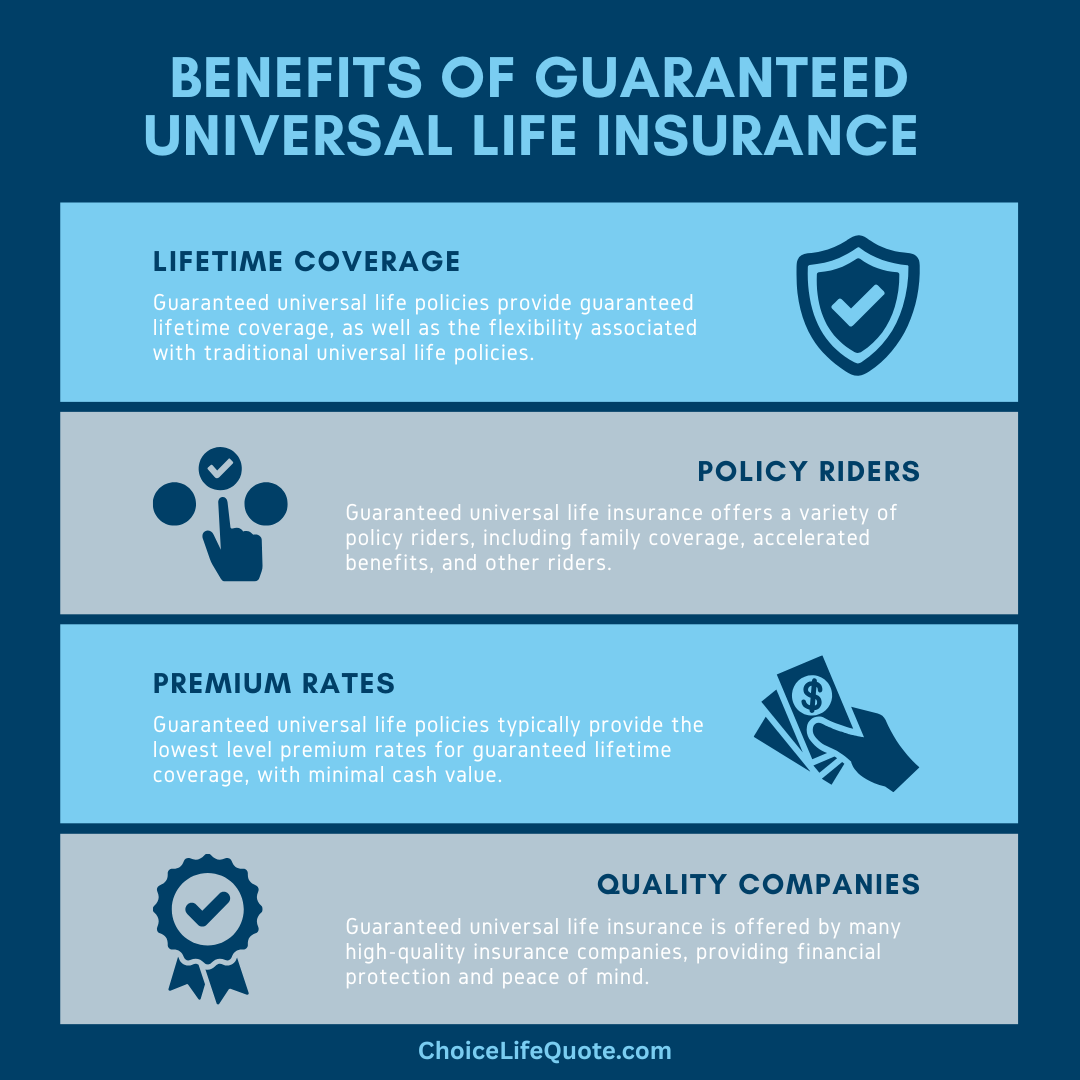

Who Benefits Most From Universal Life Insurance

“Guaranteed Universal Life | Affordable …” from choicelifequote.com and used with no modifications.

Universal life insurance is not the right fit for everyone, but for certain financial profiles, it is genuinely difficult to beat. The people who get the most value from this type of policy tend to share a few common characteristics — they have long-term financial goals, they want permanent coverage, and they are comfortable actively managing a financial product rather than setting it and walking away.

The following profiles benefit most from universal life insurance:

- High-income earners who have maxed out contributions to tax-advantaged accounts like 401(k)s and IRAs and are looking for additional tax-deferred growth vehicles

- Business owners who need flexible coverage that can adapt as their business and personal financial situations evolve

- Parents of dependents with special needs who require guaranteed lifelong financial support beyond the policyholder’s working years

- Estate planning candidates who want to pass wealth to heirs efficiently while minimizing estate tax exposure

- Individuals with variable income — such as freelancers or commission-based earners — who need premium flexibility to match inconsistent cash flow

Conversely, someone in their 20s who simply needs income replacement coverage for a 20-year mortgage is almost always better served by a term life policy. Universal life insurance earns its value over long time horizons. The longer you hold the policy and allow the cash value to compound, the more the built-in advantages work in your favor.

Is Universal Life Insurance Right for You

The honest answer is that universal life insurance is a powerful tool in the right hands and a liability in the wrong ones. If you are looking for predictable, guaranteed coverage with no management required, whole life insurance or a term policy will likely serve you better. If you want permanent coverage with the ability to build tax-deferred savings and the flexibility to adjust your policy as your life changes, universal life deserves serious consideration.

Before committing, ask your insurer or financial advisor for a detailed in-force illustration that shows how the policy performs under both optimistic and conservative interest rate assumptions. The difference between a 2% and a 5% credited rate over 30 years can be dramatic — and understanding that range before you sign gives you a realistic picture of what you are actually buying.

Frequently Asked Questions

Below are the most common questions people ask when evaluating universal life insurance, answered clearly and directly.

What happens if I stop paying premiums on my universal life insurance policy?

If you stop paying premiums, your policy does not immediately terminate. The insurer will draw from your cash value account to cover the monthly cost of insurance. As long as the cash value remains sufficient to cover these charges, your coverage stays active.

The problem arises when the cash value is depleted. Once the account cannot cover the cost of insurance, the policy enters a grace period — typically 30 to 61 days depending on your state — during which you can make a payment to keep the policy in force. If no payment is made within that window, the policy lapses and your coverage ends.

Some policies include a no-lapse guarantee rider that prevents termination for a specified period as long as a minimum defined premium is maintained. If your policy includes this rider, review it carefully to understand exactly what payment is required to keep the guarantee active.

Can I increase my death benefit after my policy is issued?

Yes, most universal life insurance policies allow you to request an increase in your death benefit after the policy is issued. However, this is not automatic. Increasing the death benefit typically requires you to submit evidence of insurability — meaning the insurer will evaluate your current health status, and approval is not guaranteed. For more information on life insurance options, you can explore what happens if you outlive your term life policy.

Decreasing your death benefit is generally simpler and does not require medical underwriting. Lowering the death benefit reduces your cost of insurance, which means more of your premium goes toward building cash value. This can be a useful strategy for policyholders who want to shift the policy’s focus from protection to accumulation as they age and their dependents become financially independent.

How is the cash value in universal life insurance taxed?

The cash value inside a universal life insurance policy grows on a tax-deferred basis. You do not owe income tax on the interest credited to your account each year it remains inside the policy. This allows the account to compound more efficiently than a comparable taxable savings vehicle.

Withdrawals are taxed on a first-in, first-out (FIFO) basis for standard universal life policies — meaning your contributions (basis) come out first, tax-free, before any taxable gains are distributed. Policy loans are not considered taxable income as long as the policy remains in force and is not classified as a modified endowment contract (MEC). If the policy lapses or is surrendered with an outstanding loan balance, the gain portion may become immediately taxable as ordinary income.

What is the difference between universal life insurance and term life insurance?

Term life insurance provides coverage for a specific period — commonly 10, 20, or 30 years — and pays a death benefit only if the insured dies during that term. It has no cash value component, no flexibility in the death benefit, and no investment element. Premiums are fixed for the duration of the term and are generally significantly lower than universal life premiums for the same death benefit amount.

Universal life insurance, by contrast, is permanent. It covers you for your entire life as long as the policy remains funded. It builds cash value over time, offers flexible premiums, and allows you to adjust your death benefit. It is a fundamentally different financial instrument — not just a longer version of term coverage.

- Term life insurance: Lower cost, fixed coverage period, no cash value, straightforward structure

- Universal life insurance: Higher cost, permanent coverage, cash value accumulation, flexible premiums and death benefit

- Best use for term: Income replacement during working years, mortgage coverage, temporary dependent protection

- Best use for universal life: Estate planning, long-term wealth accumulation, permanent coverage needs, supplemental retirement income strategy

Can I lose my universal life insurance policy if the cash value runs out?

Yes. This is one of the most critical risks associated with universal life insurance and one that catches many policyholders off guard. If your cash value is depleted — whether due to low credited interest rates, excessive loans, insufficient premium payments, or rising cost of insurance charges — and you do not make a corrective payment, your policy will lapse.

A lapsed policy means your coverage ends entirely. If you are older and in poor health at the time of lapse, obtaining new coverage may be impossible or prohibitively expensive. This is why regular policy reviews — ideally annually with your insurer or financial advisor — are not optional. They are essential to making sure your policy stays on track.

The best protection against this scenario is to request updated in-force illustrations regularly, avoid over-borrowing against your cash value, and maintain premium payments at a level that keeps the policy funded even under conservative interest rate assumptions. Understanding the mechanics of your specific policy is the most effective safeguard you have against an unexpected lapse. If you’re considering life insurance options, Ranwell Insurance can provide guidance tailored to your needs.

Looking for life insurance that fits your family’s needs?

Contact Ranwell Insurance today at (855) 508-5008 or request a free personalized quote. We help families compare life insurance options and choose coverage with confidence.

Reviewed by Ranwell Insurance

Licensed Insurance Agency

Georgia License #: GID276-EN

Ranwell Insurance provides educational guidance on life insurance, final expense insurance, mortgage protection, retirement planning, and related coverage options.

Last Reviewed: April 2026

Contact: (855) 508-5008

Disclosure: Insurance products, rates, and eligibility requirements vary by carrier and state. Information is provided for educational purposes only. Please see our Editorial Policy for more information.