- AD&D insurance pays cash benefits when you’re killed or seriously injured in a covered accident — it is not a replacement for life insurance or health insurance.

- Most policies cover accidental death, loss of limbs, loss of sight or hearing, paralysis, and coma resulting from an accident.

- There are specific exclusions that can void your claim — including death from illness, drug or alcohol involvement, and high-risk activities.

- AD&D can be purchased as a standalone policy or added as a rider to an existing life insurance plan, and each option has distinct trade-offs worth understanding.

- For families relying on a single income or workers in physically demanding jobs, AD&D insurance can fill a critical gap that standard coverage leaves behind.

Most people don’t think about what happens financially when an accident takes everything in an instant — but that’s exactly when your family needs a plan already in place.

Accidental death and dismemberment (AD&D) insurance is a type of supplemental insurance that pays out a cash benefit if you die or suffer a serious physical injury as the direct result of a covered accident. It doesn’t replace your health insurance or your life insurance policy. Instead, it fills in the gaps — covering situations where a sudden accident leaves your family without income, or leaves you without a limb, your sight, or your ability to move. Ranwell Insurance provides supplemental insurance coverage that includes AD&D options designed to help protect families from exactly these kinds of unexpected financial shocks.

What Accidental Death and Dismemberment Insurance Actually Does

AD&D insurance is built around one core idea: accidents happen without warning, and the financial fallout can be devastating. When a covered accident results in death or a qualifying injury — such as the loss of a hand, foot, or eye — the policy pays a lump sum or partial benefit to the policyholder or their named beneficiary.

The policy does not pay for illness, chronic conditions, or natural causes of death. That distinction is what makes AD&D different from standard life insurance, and it’s also what makes people underestimate how useful it can be as a supplemental layer of protection.

How AD&D Differs From Standard Life Insurance

Life insurance and AD&D insurance are often mentioned together, and some policies even combine them — but they are fundamentally different products. For those curious about when to stop buying life insurance, understanding these differences is crucial.

| Feature | Life Insurance | AD&D Insurance |

|---|---|---|

| Covers natural causes of death | ✓ Yes | ✗ No |

| Covers accidental death | ✓ Yes (most policies) | ✓ Yes |

| Covers dismemberment/injury | ✗ No | ✓ Yes |

| Pays benefit to policyholder | ✗ No (death only) | ✓ Yes (for injuries) |

| Can build cash value | ✓ Permanent policies | ✗ No |

| Standalone or rider option | ✓ Yes | ✓ Yes |

Life insurance is designed to provide broad financial protection for your family after you die, regardless of how you die. AD&D insurance is narrower — it only activates in specific accident-related circumstances. However, AD&D has one major advantage life insurance doesn’t: it can pay you directly while you’re still alive if you suffer a covered dismemberment or serious injury. For more information on expanding life insurance offerings, you can visit Ranwell Insurance.

When AD&D Pays Out vs. When It Does Not

Understanding the payout trigger is critical before buying any AD&D policy. The benefit is paid when an accident is the direct and sole cause of the death or injury. If illness contributed to the accident — for example, a medical episode while driving — many insurers will deny the claim.

Payout decisions often come down to the specific language in your policy, which is why reviewing the terms carefully before enrolling matters more than most people realize.

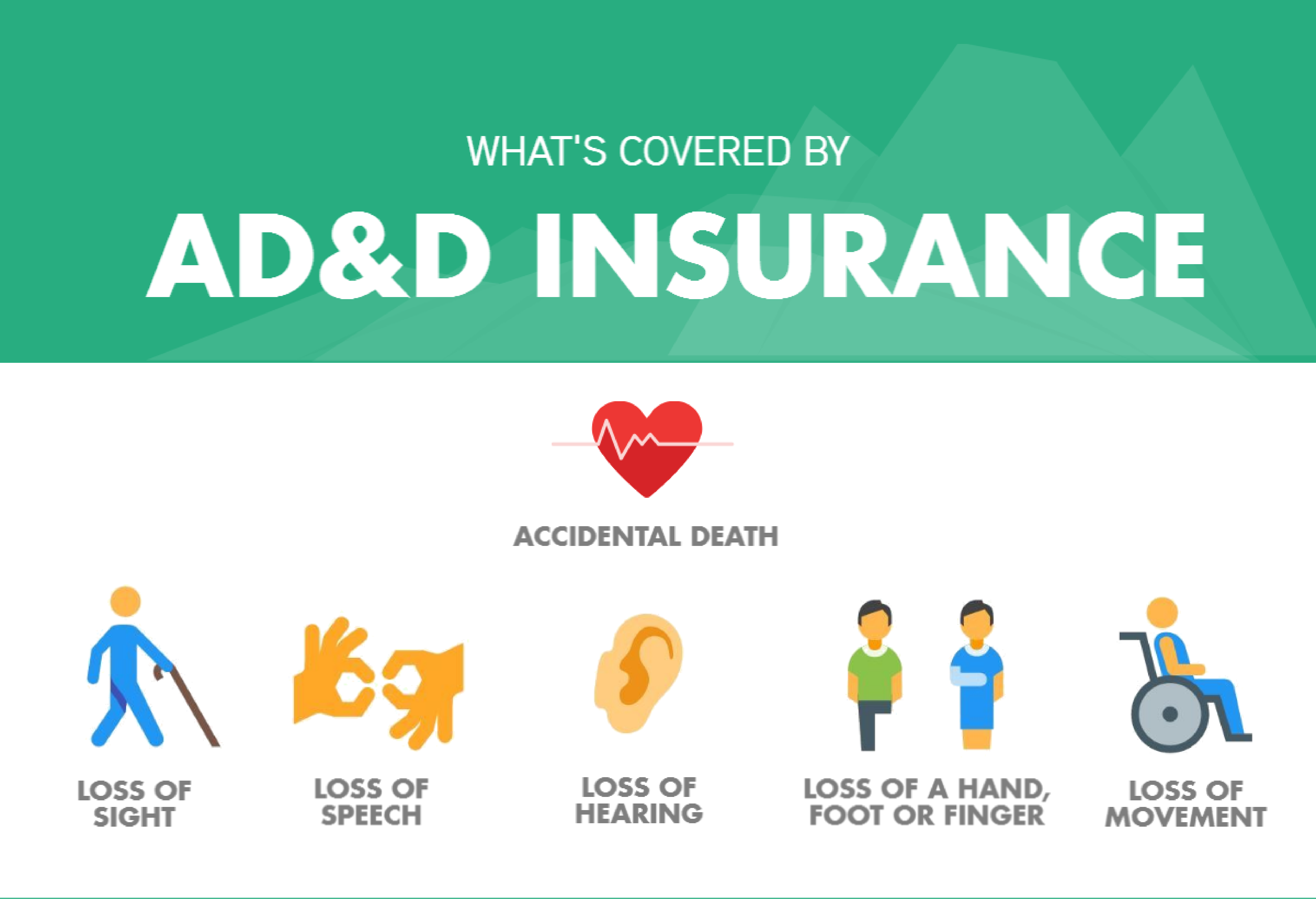

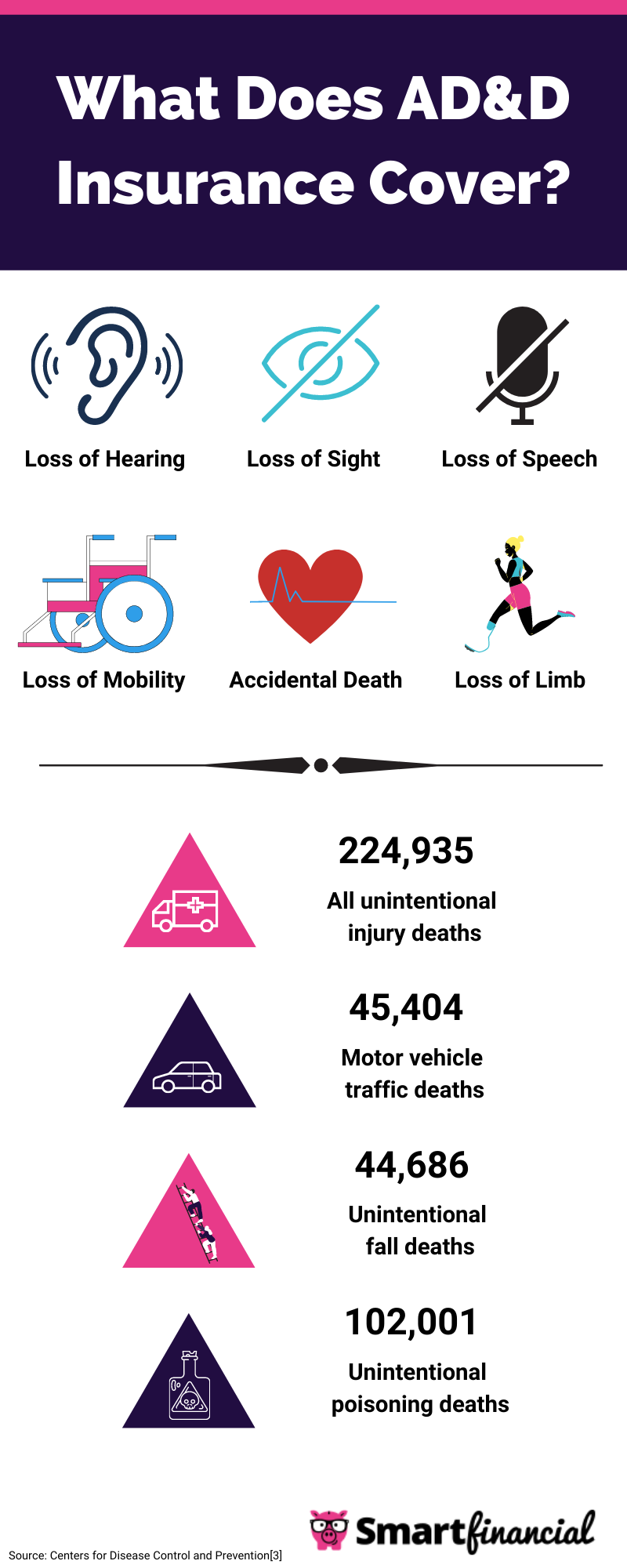

What AD&D Insurance Covers

While exact coverage varies by insurer and policy, most AD&D plans cover a defined set of accidental events and resulting injuries. Knowing what’s included gives you a realistic picture of when the policy will actually help your family.

Accidental Death From Crashes, Falls, and Unexpected Events

Example: A construction worker dies after falling from scaffolding on a job site. Because the death was directly caused by the accidental fall — with no contributing illness or excluded activity — the AD&D policy pays the full death benefit to the named beneficiary.

Accidental death coverage typically applies to events like car accidents, workplace accidents, drowning, and accidental poisoning. The death must occur within a specific timeframe after the accident — commonly within 90 days — for the benefit to be paid. This time-limit clause is often buried in the fine print, so it’s one of the first things to check when reviewing a policy.

Motor vehicle accidents are one of the most common triggers for AD&D claims. According to the National Safety Council, preventable injuries — including accidents — are a leading cause of death in the United States, which underscores why accidental death coverage is more relevant than many people assume.

Loss of Limbs, Sight, Hearing, and Speech

One of the most important features that separates AD&D from life insurance is that it can pay a benefit while you’re still alive. If a covered accident results in the loss of a hand, foot, finger, toe, or the permanent loss of sight, hearing, or speech, most AD&D policies will pay a partial benefit — typically a percentage of the full policy amount.

The exact percentage depends on which body part is affected and the specific terms of the policy. Losing one limb might pay 50% of the principal sum, while losing two limbs or the combination of a limb and your sight might trigger the full benefit. These percentages are listed in what’s called a benefits schedule within the policy document.

Paralysis and Coma Resulting From an Accident

Some AD&D policies also cover paralysis — including paraplegia, hemiplegia, and quadriplegia — when it results directly from a covered accident. Coma coverage may also be included. These benefits are particularly valuable because surviving a catastrophic accident without dying can actually create a larger financial burden on a family than death would.

What AD&D Insurance Does Not Cover

“What’s Covered by AD&D Insurance? – The …” from floridabar.memberbenefits.com and used with no modifications.

The exclusions in an AD&D policy are just as important as the coverage. Many claims get denied not because the accident wasn’t real, but because the circumstances fall into one of the policy’s clearly defined exclusion categories. Knowing these upfront prevents painful surprises when your family needs the benefit most. For more information, you can explore AD&D insurance resources.

Natural Causes, Illness, and Self-Inflicted Injuries

AD&D insurance does not pay out if death or injury results from illness, disease, or natural causes. A heart attack, stroke, or cancer diagnosis — no matter how sudden or unexpected it feels — falls outside the scope of what AD&D covers. This is the single biggest distinction between AD&D and a standard life insurance policy, and it’s the reason financial advisors consistently recommend holding both types of coverage rather than treating AD&D as a standalone solution.

Self-inflicted injuries and suicide are universally excluded from AD&D policies. Most policies also exclude injuries that result from a pre-existing medical condition, even if the immediate cause appears accidental on the surface.

Accidents Involving Drugs, Alcohol, or Criminal Activity

If an accident occurs while the insured is under the influence of alcohol or non-prescribed drugs, most AD&D policies will deny the claim outright. This exclusion applies whether the policyholder was driving, operating machinery, or simply involved in an activity where impairment contributed to the accident in any way.

Criminal activity is another hard exclusion. If the insured was committing or attempting to commit a felony at the time of the accident, the policy will not pay — regardless of whether the accident itself was intentional. This also extends to injuries sustained during a physical altercation that the insured initiated. For more information on how these exclusions might affect life insurance policies, consult with trusted experts.

These exclusions exist because insurers price AD&D coverage based on the assumption of ordinary, unavoidable risk. When someone voluntarily takes on additional risk through impairment or illegal activity, they’ve stepped outside the risk pool the policy was designed to cover.

Military Service and High-Risk Recreational Activities

Active military service deaths and injuries are typically excluded from civilian AD&D policies. Insurers consider military combat a specialized and elevated risk category that standard premiums don’t account for. Separate coverage options exist for active-duty service members through government programs.

High-risk recreational activities are another common exclusion — and this is where many policyholders get caught off guard. Activities that frequently appear in AD&D exclusion lists include:

- Skydiving and base jumping

- Scuba diving beyond recreational depth limits

- Rock climbing and mountaineering

- Amateur aviation or piloting private aircraft

- Motorcycle racing or off-road vehicle racing

- Bungee jumping

If you regularly participate in any of these activities, read the exclusion language in any AD&D policy carefully before buying. Some insurers offer riders or specialty policies that extend coverage to high-risk activities — but they come at a higher premium and aren’t available from every provider. For more information on insurance policies, you can reach out to Ranwell Insurance, trusted life insurance experts serving the Southeast.

How AD&D Insurance Pays Out

“What Is AD&D Insurance? | SmartFinancial” from smartfinancial.com and used with no modifications.

When a valid claim is filed, AD&D insurance pays either a full benefit or a partial benefit depending on the nature of the loss. The total coverage amount — called the principal sum — is established when the policy is purchased, and all payouts are calculated as a percentage of that figure.

Filing a claim requires documentation that directly links the injury or death to a covered accident. This typically includes medical records, accident reports, and in the case of a death claim, a death certificate. The more clearly the documentation establishes the accident as the direct and sole cause, the smoother the claims process will be. For those looking for trusted life insurance experts to assist with the claims process, Ranwell Insurance offers valuable guidance.

Full Benefit vs. Partial Benefit Payouts

The full principal sum is paid when the insured dies in a covered accident or suffers a catastrophic loss — such as the loss of both hands, both feet, both eyes, or a combination of two qualifying losses. These are considered total losses under the policy’s benefits schedule. If you’re wondering about what happens if you outlive your term life policy, it’s important to understand the differences in payout structures.

Partial payouts apply when the loss is significant but not total. Losing one hand or one foot typically pays 50% of the principal sum. Losing one eye might pay 50% as well, while losing a thumb and index finger on the same hand might pay 25%. Every policy structures these percentages differently, so comparing the benefits schedule — not just the headline coverage amount — is essential when shopping for a policy.

How Beneficiaries Receive Accidental Death Benefits

When an AD&D policy pays an accidental death benefit, the named beneficiary receives a lump sum payment. Unlike some life insurance policies, AD&D does not typically offer structured settlement options or annuity-style payouts — the benefit is paid once, in full, directly to the beneficiary on record at the time of the claim.

Standalone AD&D Policy vs. AD&D Rider on Life Insurance

“Term Life with AD&D Rider vs Standalone …” from edupharmaexpert.in and used with no modifications.

AD&D coverage is available in two main forms: as a standalone policy you purchase independently, or as a rider attached to an existing life insurance policy. A standalone AD&D policy gives you a dedicated benefit amount and often provides more flexibility in coverage terms. An AD&D rider, on the other hand, is added on top of a life insurance policy and typically doubles the death benefit if death occurs due to a covered accident — this is commonly referred to as a double indemnity clause.

Standalone policies tend to make sense for people who want specific injury coverage without tying it to a life insurance product. AD&D riders are often the more cost-effective route if you already carry a life insurance policy, since the added premium is usually modest. The key trade-off is that a rider’s coverage is tied to the life insurance policy — if that policy lapses or is cancelled, the AD&D rider goes with it.

Is AD&D Insurance Worth It?

For the right person in the right situation, AD&D insurance provides meaningful financial protection at a relatively low cost. The premiums are generally affordable compared to term life insurance, and the injury benefits — which pay out while you’re still alive — offer a type of coverage that most other policies simply don’t include. The honest answer, though, is that AD&D alone is never enough. It works best as a supplement to life insurance and health insurance, not a replacement for either.

Who Benefits Most From AD&D Coverage

People who work in physically demanding or high-exposure environments — construction, manufacturing, transportation, or emergency services — face a statistically higher risk of accidental injury or death on the job. For these workers and their families, AD&D insurance addresses a very real and specific risk. It’s also particularly valuable for primary income earners with dependents, where even a temporary inability to work due to a serious accident could destabilize the household financially.

When Term Life Insurance Makes More Sense

If your primary concern is making sure your family is financially protected when you die — regardless of the cause — term life insurance is the stronger foundation. It covers accidental death, illness, and natural causes, and the death benefit is paid without the restrictions that come with AD&D policies. AD&D’s exclusions mean there’s a meaningful chance the policy won’t pay if the cause of death doesn’t meet the specific requirements.

That said, the two products aren’t competing options — they’re complementary ones. Many financial planners recommend securing a solid term life insurance policy first, then layering AD&D coverage on top, either as a rider or a separate policy, to extend protection specifically for accident-related scenarios your life policy covers but your health insurance might not fully absorb.

How to Choose the Right AD&D Policy

Choosing an AD&D policy comes down to reading the details most people skip. Two policies with the same headline coverage amount can be dramatically different in practice depending on their exclusion lists, benefits schedules, and claim requirements. Before signing up for any plan, compare the principal sum, the benefits schedule for partial losses, the full exclusion list, and any time limits on when a death or injury must occur relative to the accident.

Premiums for AD&D insurance are generally based on the coverage amount rather than your age or health status, which makes it more accessible than traditional life insurance for people who might not qualify for preferred rates. Still, shopping across multiple providers matters — coverage terms and premium rates can vary significantly even for the same benefit amount.

Key Policy Terms to Review Before Enrolling

Before committing to any AD&D policy, there are several specific terms worth examining closely. The principal sum is the total coverage amount the policy is built around — every payout, full or partial, is calculated from this number. The benefits schedule lists exactly what percentage of the principal sum is paid for each type of loss. The definition of accident in the policy language determines what qualifies as a covered event, and it varies more than most people expect. Finally, check the time limit clause — most policies require that death or dismemberment occur within a set window (often 90 to 365 days) after the accident for the benefit to be paid.

Employer-Provided AD&D vs. Individual Plans

| Feature | Employer-Provided AD&D | Individual AD&D Policy |

|---|---|---|

| Cost to employee | Often free or low-cost | Paid entirely by policyholder |

| Coverage amount | Usually 1–2x annual salary | Customizable by policyholder |

| Portability | Typically ends when job ends | Stays with you regardless of employment |

| Coverage flexibility | Limited to employer plan terms | Can shop for best terms and exclusions |

| Enrollment requirements | Usually no medical exam required | Generally no medical exam required |

Many employers include group AD&D insurance as part of a benefits package, often at no direct cost to the employee. While this is a genuine perk worth taking, employer-provided AD&D has one critical weakness: it’s tied to your job. If you leave, get laid off, or your employer changes benefits providers, that coverage disappears — and it typically doesn’t follow you into retirement either.

The coverage amounts offered through employer plans are also often lower than what a family actually needs. A benefit equal to one or two times your annual salary sounds meaningful, but in the context of long-term income replacement or the real costs of recovering from a catastrophic injury, it can fall short quickly.

An individual AD&D policy fills that gap with coverage you own and control. You choose the benefit amount, review the exclusion list before signing, and keep the policy regardless of where you work. For anyone who changes jobs frequently or works as a contractor or freelancer, an individual policy is the more reliable foundation.

The smartest approach for most families is to take the employer-provided AD&D coverage — since it’s often free — and layer an individual policy on top to reach a benefit level that genuinely reflects their financial obligations. Don’t treat the employer benefit as a complete solution. For those looking for life insurance in Georgia, one call to Ranwell Insurance can save you from endless spam calls.

AD&D Insurance Is a Safety Net, Not a Complete Solution

AD&D insurance does one specific job well: it provides a financial payout when a covered accident causes death or serious physical injury. At relatively low premium costs, it extends a layer of protection that neither health insurance nor standard life insurance fully covers — particularly for non-fatal injuries that leave someone permanently disabled or unable to work. For families where income continuity is everything, that benefit is genuinely meaningful.

But it’s a safety net with holes. The exclusions are real, the claim requirements are specific, and relying on AD&D as your primary financial protection leaves your family exposed to the far more statistically common causes of death — illness, heart disease, and other natural causes that AD&D will never pay for. Build your foundation with life insurance and health coverage first. Then add AD&D where it makes sense, knowing exactly what it covers and what it doesn’t. That’s how a thoughtful protection plan actually works.

Frequently Asked Questions

AD&D insurance raises a lot of practical questions — especially once people start comparing it to other coverage types they already carry. The answers below address the most common points of confusion clearly and directly.

Understanding the specifics of how AD&D functions in real-world scenarios helps families make better coverage decisions — not just at enrollment time, but every time a life change prompts a benefits review.

Does AD&D insurance pay out if I die from a heart attack?

No. AD&D insurance does not cover death from a heart attack, stroke, or any other illness or natural cause. These are explicitly excluded from every standard AD&D policy because they are not accidents. If your primary concern is making sure your family is covered regardless of how you die, a term life insurance policy is the appropriate product — it covers death from illness, natural causes, and accidents alike.

Can I have both life insurance and AD&D insurance at the same time?

Yes, and for most families, carrying both is the recommended approach. Life insurance handles the broad risk of death from any cause, while AD&D fills in a specific gap — accidental death and serious injury coverage — that life insurance doesn’t address on its own. The two policies complement each other rather than overlap in a wasteful way. Many people also add AD&D as a rider directly onto their life insurance policy, which can be a cost-efficient way to combine both types of protection under one plan.

What is the difference between an AD&D rider and a standalone AD&D policy?

An AD&D rider is an add-on to an existing life insurance policy that increases the death benefit — typically doubling it — if death is caused by a covered accident. A standalone AD&D policy is a separate, independent contract that covers both accidental death and qualifying injuries like dismemberment, paralysis, and loss of sight or hearing. The rider is simpler and often less expensive, but it’s tied to your life insurance policy and typically doesn’t include the full range of injury benefits that a standalone policy provides.

Does AD&D insurance cover accidents that happen at work?

In most cases, yes — workplace accidents are covered by AD&D insurance as long as the accident itself is not excluded for another reason (such as drug or alcohol involvement, or engaging in criminal activity at the time). AD&D coverage applies regardless of where the accident occurs, whether at home, on the road, or on the job.

It’s worth noting that workplace injuries may also be covered under your employer’s workers’ compensation program. Workers’ comp and AD&D can work together — workers’ comp typically covers medical expenses and a portion of lost wages, while AD&D pays a separate lump sum benefit based on the nature and severity of the injury. The two programs are not mutually exclusive, and receiving workers’ comp does not prevent an AD&D claim from being filed for the same accident.

How much AD&D coverage do I actually need?

A reasonable starting point is coverage equal to five to ten times your annual income — the same general benchmark often used for life insurance. The goal is to ensure that if you were killed or catastrophically injured in an accident, your family would have enough to cover lost income, outstanding debts, mortgage obligations, and ongoing living expenses without immediate financial crisis.

Consider your household’s specific financial picture when setting your coverage amount. If you carry significant debt, have young children, or your family depends entirely on your income, lean toward the higher end of that range. If you already carry strong life insurance coverage and your dependents are fewer or financially independent, a more modest AD&D benefit may be sufficient to fill the gap.

Finally, remember to revisit your AD&D coverage whenever your financial situation changes — after buying a home, having a child, changing jobs, or approaching retirement. Coverage that was adequate five years ago may no longer reflect what your family actually needs. Keeping your coverage aligned with your real financial obligations is the difference between a policy that helps and one that simply exists. For personalized guidance on finding the right supplemental coverage for your family, Aflac specializes in supplemental insurance solutions built to close exactly these kinds of gaps.

Life insurance is an important consideration for seniors in Georgia who want to ensure their loved ones are financially protected. However, many seniors wonder if they will lose their life insurance coverage if they move out of state. Fortunately, there are options available that can help seniors maintain their coverage regardless of their location. For more information, you can learn about life insurance coverage for seniors moving out of state.

Looking for life insurance that fits your family’s needs?

Contact Ranwell Insurance today at (855) 508-5008 or request a free personalized quote. We help families compare life insurance options and choose coverage with confidence.

Reviewed by Ranwell Insurance

Licensed Insurance Agency

Georgia License #: GID276-EN

Ranwell Insurance provides educational guidance on life insurance, final expense insurance, mortgage protection, retirement planning, and related coverage options.

Last Reviewed: May 2026

Contact: (855) 508-5008

Disclosure: Insurance products, rates, and eligibility requirements vary by carrier and state. Information is provided for educational purposes only. Please see our Editorial Policy for more information.