- Whole life insurance covers you for your entire life — unlike term life, it never expires as long as you keep paying your premiums.

- A portion of every premium builds cash value you can borrow against or withdraw while you’re still alive.

- The death benefit is guaranteed, giving your family financial certainty no matter when you pass.

- Whole life offers tax advantages most policyholders don’t fully realize — including tax-deferred cash value growth and tax-free loans.

- The higher premium cost is real — but understanding exactly what you’re getting in return changes how you evaluate it entirely.

Most people buy life insurance from Ranwell Insurance thinking about death — but whole life insurance is just as much about how you live.

When you hold a whole life policy, you’re not just buying a payout for your family someday. You’re building a financial asset that grows quietly in the background, available to you during your lifetime and guaranteed for your beneficiaries after. For anyone planning long-term financial security, that combination is hard to match. Understanding how permanent coverage works is one of the most important steps toward building a financial plan that actually holds up over time.

Whole Life Insurance Covers You for Life — Here’s What That Really Means

“How Whole Life Insurance Works” from www.investopedia.com and used with no modifications.

Term life insurance is straightforward — you’re covered for 10, 20, or 30 years. If you outlive the policy, the coverage ends and the premiums you paid are gone. Whole life works completely differently. Your coverage doesn’t have an expiration date. As long as you pay your premiums, the policy stays active until you die — whether that’s at 65 or 95.

That permanence matters more than most people realize. It removes the guesswork. You don’t have to worry about re-qualifying for coverage later in life when health conditions might make that impossible. The policy you lock in today is the coverage your family keeps. For those wondering, can a 70-year-old get life insurance in Georgia?

How Whole Life Insurance Works

Every whole life insurance policy is built on two core components: a death benefit and a cash value account. When you pay your premium each month, that payment is split — part covers the cost of your insurance, and part goes into the cash value savings portion. Over time, that savings component grows at a guaranteed rate, building real financial value inside your policy.

How Premiums Are Set and Why They Stay Fixed

One of the most practical features of whole life insurance is that your premiums are locked in at the time you buy the policy. They don’t increase as you age, and they don’t change if your health declines. Insurers calculate your premium based on your age and health at the time of purchase, then hold that rate for the life of the policy. The earlier you buy, the lower that fixed rate will be — making age at purchase one of the most important financial decisions tied to this type of coverage.

How Cash Value Builds Over Time

The cash value in a whole life policy grows on a tax-deferred basis, meaning you don’t owe taxes on the growth each year. The insurer guarantees a minimum growth rate, so your cash value increases predictably regardless of market conditions. This is a key difference from investment-linked policies — your cash value won’t drop because the stock market had a bad year.

After enough time, some policyholders find their cash value has grown large enough that the policy essentially sustains itself. In some cases, accumulated dividends (paid by participating whole life policies) can be used to cover premium payments entirely.

How the Death Benefit Is Paid Out

When the insured person passes away, the insurance company pays the death benefit — a lump sum — directly to the named beneficiaries. This payment is generally income tax-free under current IRS rules. The amount is the face value of the policy, which was agreed upon when the policy was purchased and guaranteed not to decrease.

It’s worth noting one common point of confusion: in most standard whole life policies, the cash value is not added on top of the death benefit. The insurer typically pays out the face value of the policy, and the accumulated cash value is absorbed by the insurer. Some policies, called whole life with paid-up additions, are structured differently — but standard policies work this way by default.

The Real Benefits of Whole Life Insurance

“Benefits of Whole Life Insurance” from www.westernsouthern.com and used with no modifications.

Whole life insurance gets a mixed reputation, mostly because people compare its premium cost to term life without accounting for what it actually delivers. When you look at the full picture, the benefits go well beyond a simple death payout.

Lifetime Coverage With No Expiration Date

There’s no scenario where you outlive a whole life policy and lose your coverage. This is significant for anyone with long-term financial dependents, estate planning goals, or a lifelong commitment to leaving something behind. Unlike term policies that force you to re-evaluate coverage every decade or two, whole life is a decision you make once and maintain.

Cash Value You Can Actually Use While You’re Alive

The cash value that builds in your policy isn’t locked away until death. You can borrow against it at relatively low interest rates, use it as collateral, or make a direct withdrawal. People use this feature to cover emergencies, fund a child’s education, supplement retirement income, or bridge financial gaps without going through a bank. The flexibility is real and meaningful — especially later in life when traditional lending can become harder to access.

Tax Advantages Most People Overlook

Whole life insurance comes with a tax profile that most financial products can’t match. The cash value grows tax-deferred year over year. Policy loans are not considered taxable income. And the death benefit paid to your beneficiaries is typically received income tax-free. For high-income earners or anyone looking to reduce taxable estate value, these features can make whole life a legitimate part of a broader tax strategy — not just an insurance product. For more insights, consider exploring Ranwell Insurance’s expertise in life insurance.

A Guaranteed Death Benefit Your Family Can Count On

The death benefit in a whole life policy isn’t a projection or an estimate — it’s a contractual guarantee. The amount your beneficiaries will receive is set when the policy is issued and cannot be reduced as long as premiums are paid. For families building long-term financial plans, that certainty is foundational. It means your spouse, children, or other dependents aren’t left guessing about what they’ll receive or when.

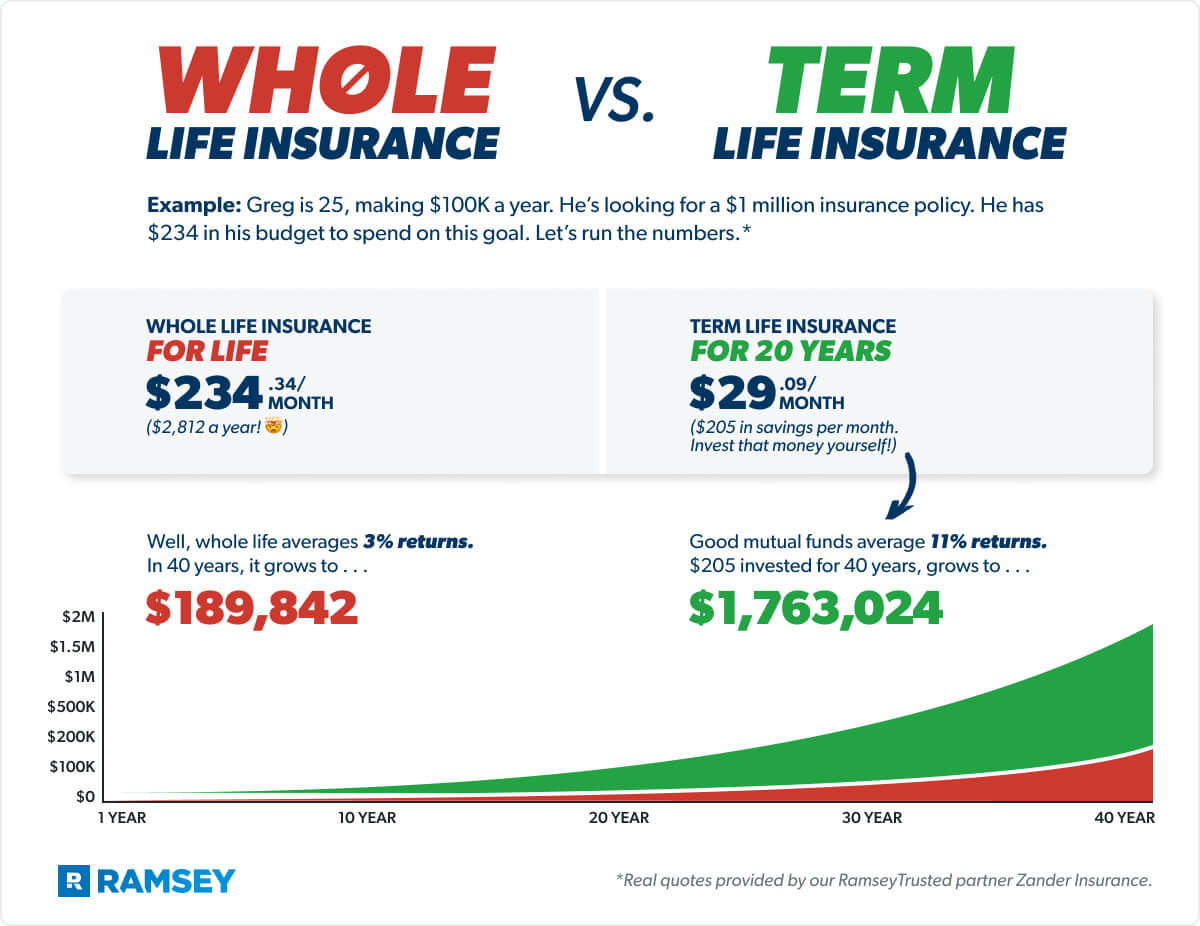

Whole Life Insurance vs. Term Life Insurance

“Term vs. Whole Life Insurance: What’s …” from www.ramseysolutions.com and used with no modifications.

Choosing between whole life and term life insurance is one of the most common — and most misunderstood — decisions in personal finance. Both provide a death benefit, but they’re built for different purposes and different types of buyers. For those wondering about life insurance options at different ages, you might find it helpful to learn about life insurance for seniors.

Term life is simple: you pick a coverage period, pay a lower premium, and your beneficiaries collect if you die within that window. If you live past the term, the policy ends with no payout and no savings component. It’s pure protection, nothing more.

Whole life, on the other hand, combines lifetime protection with a savings vehicle that builds real value over time. You pay more each month, but you’re getting coverage that never expires and a cash value account that grows in the background. The two products aren’t really competing — they serve different financial goals.

Cost Differences Between Whole and Term Life

The premium gap between whole life and term life is significant and worth addressing directly. For the same death benefit amount, whole life premiums can run anywhere from five to fifteen times higher than a comparable term policy. That’s not a small difference — and it’s the primary reason many financial advisors default to recommending term life for younger buyers on tight budgets.

However, the cost comparison only tells part of the story. Term premiums are, effectively, spent — when the term ends, that money is gone. Whole life premiums build cash value, contribute to a guaranteed death benefit, and can eventually fund the policy itself through accumulated dividends. Viewed over a 30- or 40-year horizon, the math looks very different than a simple monthly premium comparison.

A 35-year-old in good health might pay around $200 to $300 per month for a $500,000 whole life policy, compared to roughly $25 to $40 per month for a 20-year term policy with the same benefit. The price difference is real — but so is the difference in what each product delivers over a lifetime.

Which One Makes More Sense for Your Family

Term life makes the most sense when your primary goal is maximum coverage at minimum cost — ideal for young families with a mortgage, income replacement needs, and a limited budget. Whole life fits better when you have long-term estate planning goals, want a guaranteed financial asset that builds over time, or need coverage that will still be in force decades from now regardless of future health changes. For some households, holding both simultaneously is the most practical approach.

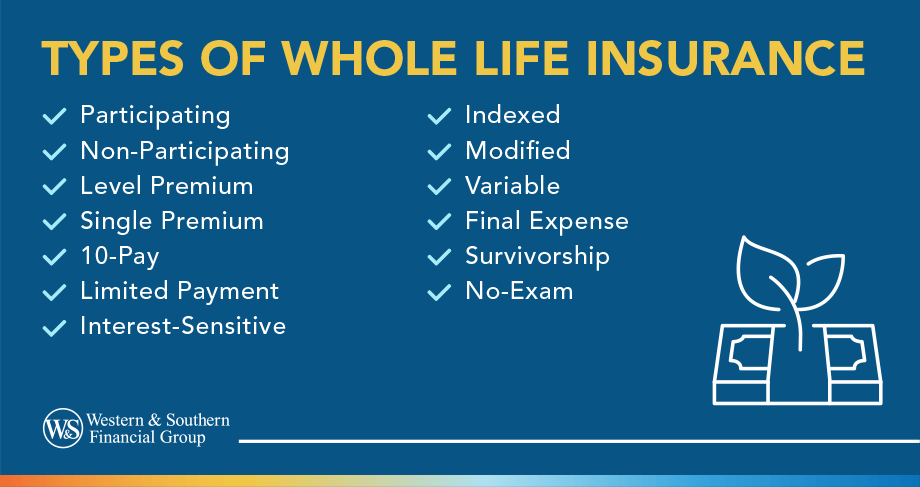

Types of Whole Life Insurance Policies

“What Are the Types of Whole Life Insurance?” from www.westernsouthern.com and used with no modifications.

Whole life insurance isn’t a single product — it comes in several structures, each designed to fit different financial situations and payment preferences. The core benefits remain consistent across types, but how and when you pay can vary significantly.

- Standard Whole Life — level premiums paid throughout your lifetime with guaranteed cash value growth

- Modified Whole Life — lower premiums in the early years that increase after a set period, typically 5 to 10 years

- Limited Payment Whole Life — higher premiums paid over a shorter period (10, 20, or 30 years) after which the policy is fully paid up

- Single Premium Whole Life — the entire policy is funded with one large upfront payment, immediately creating substantial cash value

- Participating Whole Life — issued by mutual insurance companies, these policies may pay annual dividends that can be reinvested into the policy

Each structure has a specific use case. A high-income earner looking to move a lump sum into a tax-advantaged vehicle might lean toward single premium whole life. Someone earlier in their career who expects income to grow might find modified whole life a practical entry point.

The right type depends entirely on your cash flow, financial goals, and how long you plan to hold the policy. Working with a licensed insurance professional helps match the right structure to your actual situation rather than defaulting to a one-size-fits-all recommendation.

Standard Whole Life

Standard whole life is the most common form of the policy. You pay the same premium every month for your entire life, and in return you receive lifetime coverage, guaranteed cash value accumulation, and a fixed death benefit. It’s straightforward, predictable, and the easiest version to budget around.

For most people entering the whole life market for the first time, standard whole life is the baseline product worth understanding before exploring more specialized structures. It’s the benchmark everything else is measured against.

Modified Whole Life

Modified whole life is designed for buyers who want permanent coverage now but can’t comfortably afford standard premiums right away. Premiums start lower — sometimes close to term rates — for an initial period of five to ten years, then step up to a higher fixed rate for the remainder of the policy. The tradeoff is that cash value builds more slowly in the early years, and the total lifetime cost is often higher than a standard policy.

Limited Payment Whole Life

With limited payment whole life, you compress your premium payments into a defined window — commonly 10, 20, or 30 years — after which the policy is considered paid up and coverage continues for life with no further payments required. Premiums during the payment period are higher than standard whole life, but the appeal is significant: at a certain point, your coverage becomes completely free of ongoing cost. This structure is especially popular among people who want to eliminate insurance expenses during retirement, such as seniors looking to cover medical debt.

Drawbacks Worth Knowing Before You Commit

“Whole Life Insurance Definitive Guide …” from abramsinc.com and used with no modifications.

Whole life insurance is a powerful financial tool — but it’s not the right fit for everyone, and going in without understanding the limitations is a mistake that can be costly to reverse.

Higher Premiums Compared to Term Life

The most common reason people walk away from whole life insurance is the premium. Compared to term life, the monthly cost is substantially higher — and that gap is real. A healthy 40-year-old might pay $50 per month for a 20-year term policy with a $500,000 death benefit, while the equivalent whole life policy could run $400 to $500 per month or more depending on the insurer and policy structure.

That number can feel hard to justify, especially when you’re balancing a mortgage, retirement contributions, and everyday expenses. But the comparison needs to be made honestly. Term premiums buy pure protection — when the term ends, nothing remains. Whole life premiums build a financial asset. The cash value in your policy is real money, accessible during your lifetime, growing on a tax-deferred basis every year you hold the policy.

The question isn’t really whether whole life costs more than term — it does, by a significant margin. The real question is whether the lifetime coverage, guaranteed death benefit, and growing cash value justify that premium for your specific financial situation. For many people, especially those with estate planning goals or lifelong dependents, the answer is yes.

- Whole life premiums are fixed — they won’t increase as you age or if your health changes

- Every premium payment builds equity in the form of cash value you can access

- The death benefit is guaranteed regardless of when you die, not just within a set window

- Dividends from participating policies can eventually offset or eliminate your premium payments entirely

- Buying younger locks in a lower fixed rate for the lifetime of the policy — delaying costs more long-term

Slower Cash Value Growth Than Other Investment Options

Whole life insurance is not an investment product — and treating it like one leads to unfair comparisons. The cash value in a whole life policy grows at a conservative, guaranteed rate. It won’t keep pace with a well-performing stock portfolio over a 30-year bull market. For pure wealth accumulation, options like index funds or a maxed-out 401(k) will typically outperform the cash value growth rate in a whole life policy.

That said, the cash value in a whole life policy offers something no market-linked investment can: a guarantee. The balance doesn’t drop when markets fall. It grows at a predictable rate, sheltered from volatility, accessible when needed. For someone using whole life as one piece of a larger financial plan — not as their only savings vehicle — that stability has genuine value, particularly as a buffer during retirement or economic downturns.

Whole Life Insurance Is a Long-Term Decision — Make It With Confidence

“Whole Life Insurance: Benefits, Cost …” from www.riskquoter.com and used with no modifications.

Whole life insurance rewards patience and punishes short-term thinking. If you cancel a policy in the first few years, the surrender value is low and the financial benefit disappears. But held over decades, it becomes a dependable, multi-purpose financial asset — providing a guaranteed death benefit, a growing tax-advantaged savings component, and lifetime coverage that never expires. The decision to buy should be made with a clear-eyed view of your long-term financial goals, your budget, and your family’s needs — not based on premium cost alone. If you’re evaluating whether whole life fits your plan, speaking with a licensed advisor who can model the long-term numbers for your specific situation is the most valuable step you can take.

Frequently Asked Questions

Whole life insurance raises a lot of questions — and the details matter. The following answers address the most common points of confusion so you can make an informed decision without guesswork.

Can I withdraw money from my whole life insurance policy?

Yes — you can access your cash value through two main methods: a policy loan or a direct withdrawal. Policy loans let you borrow against the cash value without a credit check or approval process, and the loan is not considered taxable income. You repay it on your own schedule, though unpaid loan balances plus interest will reduce the death benefit paid to your beneficiaries. For more information, you can read about whole life insurance on Investopedia.

Direct withdrawals are also possible, but come with more nuance. Withdrawals up to the amount you’ve paid in premiums (your cost basis) are generally tax-free. Any amount above that cost basis is considered a gain and becomes taxable as ordinary income. Withdrawing too much can also risk triggering the policy to lapse, so it’s worth consulting your insurer or a financial advisor before making large withdrawals.

Does whole life insurance ever expire?

No. Whole life insurance does not expire as long as you continue paying your premiums. This is the defining feature that separates it from term life insurance. Some policies include a maturity date — typically age 100 or 121 depending on the policy — at which point the cash value equals the death benefit and the insurer may pay out the face value directly to the policyholder. In practical terms for most policyholders, the coverage is permanent.

Is whole life insurance worth the higher cost?

It depends entirely on what you need the policy to do. For someone whose primary goal is replacing income for a set number of years at the lowest possible cost, term life is the more efficient choice. But for someone who wants lifelong coverage, a guaranteed death benefit for estate planning purposes, a tax-advantaged savings component, or protection against future insurability issues — whole life delivers value that term simply can’t replicate. For more information, you might consider at what age you should stop buying life insurance.

The people who get the most out of whole life insurance are typically those who buy it early (locking in lower fixed premiums), hold it for decades, and use the cash value strategically over time. Those who struggle with the value proposition are often those who bought it expecting investment-level returns or who cancel the policy within the first five to ten years before the cash value has meaningfully accumulated.

Whole life also makes strong financial sense for high-net-worth individuals looking to reduce taxable estate size, business owners using it for key-person coverage or buy-sell agreements, and parents of children with special needs who require guaranteed lifetime financial support.

One useful way to evaluate whether whole life is worth it: add up the total premiums you’d pay over 20 to 30 years, then compare that to the guaranteed cash value and death benefit at that same point in time. The numbers often look very different from a simple monthly premium comparison.

Feature Whole Life Insurance Term Life Insurance Coverage Duration Lifetime (permanent) Fixed term (10, 20, 30 years) Premium Cost Higher, fixed for life Lower, fixed for term Cash Value Yes — grows tax-deferred No Death Benefit Guaranteed, does not expire Only paid if death occurs in term Policy Loans Available against cash value Not available Tax Advantages Tax-deferred growth, tax-free loans, tax-free death benefit Tax-free death benefit only Best For Lifelong protection, estate planning, cash value building Temporary income replacement, budget-conscious buyers

What happens to the cash value when I die?

In most standard whole life insurance policies, the cash value does not pass to your beneficiaries separately — it is absorbed back into the insurance company, and your beneficiaries receive the policy’s face value (the death benefit) as a lump sum. This is one of the most important and frequently misunderstood aspects of how whole life insurance works. If maximizing the transfer of cash value at death is a priority, certain policy riders or policy structures — such as paid-up additions riders — can be used to increase the death benefit over time as cash value grows, but these need to be built into the policy from the start.

Can I convert a term life policy to whole life insurance?

Many term life insurance policies include a conversion privilege — a feature that allows you to convert some or all of your term coverage into a permanent whole life policy without needing to pass a new medical exam. This is an important feature because it protects your insurability. If your health changes during your term, you can still lock in permanent coverage based on your original health classification at the time of the term policy purchase.

Conversion options vary by insurer and policy. Some allow conversion at any point during the term; others restrict it to a specific conversion window, often the first 10 years of the policy. The premium for the new whole life policy will be based on your current age at the time of conversion, not your age when you originally bought the term policy — so converting earlier generally results in a lower permanent premium.

If you currently hold a term policy and are considering a longer-term coverage strategy, reviewing your conversion options before your conversion window closes is one of the smartest and most overlooked moves in personal financial planning. It’s a no-exam path to permanent coverage that most policyholders don’t even realize they already have access to.

Ready to Compare Your Options?

Call (855) 508-5008 to speak directly with Ranwell Insurance about your coverage goals. We compare multiple carriers, explain your options clearly, and help you choose protection that fits your budget and long-term plans — without pressure.

You can also request a personalized quote and see how different coverage amounts and term lengths affect your monthly cost.