- Term life insurance is one of the most affordable ways to protect your family’s financial future — locking in fixed premiums for 10, 20, or 30 years while your dependents rely on your income.

- Your beneficiaries receive a lump-sum death benefit that can replace lost income, pay off a mortgage, cover debt, and handle everyday expenses if you pass away during the term.

- There are four main types of term life insurance — level term, annual renewable, group, and convertible — each suited to different financial situations and timelines.

- Term life is significantly cheaper than whole life insurance, making it the go-to choice for young families, homeowners, and anyone with time-sensitive financial obligations.

- Choosing the right term length and coverage amount is the most important decision you’ll make — and there’s a straightforward formula most financial planners use to get it right.

Ranwell Insurance says term life insurance is the most straightforward way to make sure the people who depend on you are not left financially vulnerable if you die unexpectedly.

If you’re new to life insurance or weighing your options, understanding the fundamentals of term life coverage is the single most important step you can take toward building a solid financial safety net for your family. The concept is simple, but the decisions you make — term length, coverage amount, and policy type — have real long-term consequences.

Term Life Insurance Gives Your Family a Financial Safety Net

“A Guide to Term Life Insurance: Types …” from www.investopedia.com and used with no modifications.

Most people buy life insurance for one reason: to make sure their family doesn’t fall apart financially when they’re gone. Term life insurance does exactly that — efficiently, affordably, and without unnecessary complexity.

What Term Life Insurance Actually Does

Term life insurance is a contract between you and an insurer. You pay a fixed monthly or annual premium for a set period — typically 10, 15, 20, or 30 years. If you die during that period, the insurer pays a lump-sum death benefit to your named beneficiaries. If you outlive the term, the policy simply expires with no payout.

That’s it. No investment component, no cash value, no complexity. This simplicity is exactly what makes term life so cost-effective compared to other types of life insurance. You’re paying purely for protection — and that keeps premiums low.

How the Death Benefit Protects Your Loved Ones

The death benefit is the core of any term life policy. When a policyholder passes away while the policy is active, beneficiaries receive the full death benefit as a tax-free lump sum. They can use it however they need — replacing lost income, covering mortgage payments, paying off outstanding debt, funding a child’s education, or simply keeping the household running.

This financial cushion gives families the time and resources to stabilize without being forced into panic-driven financial decisions during an already devastating time.

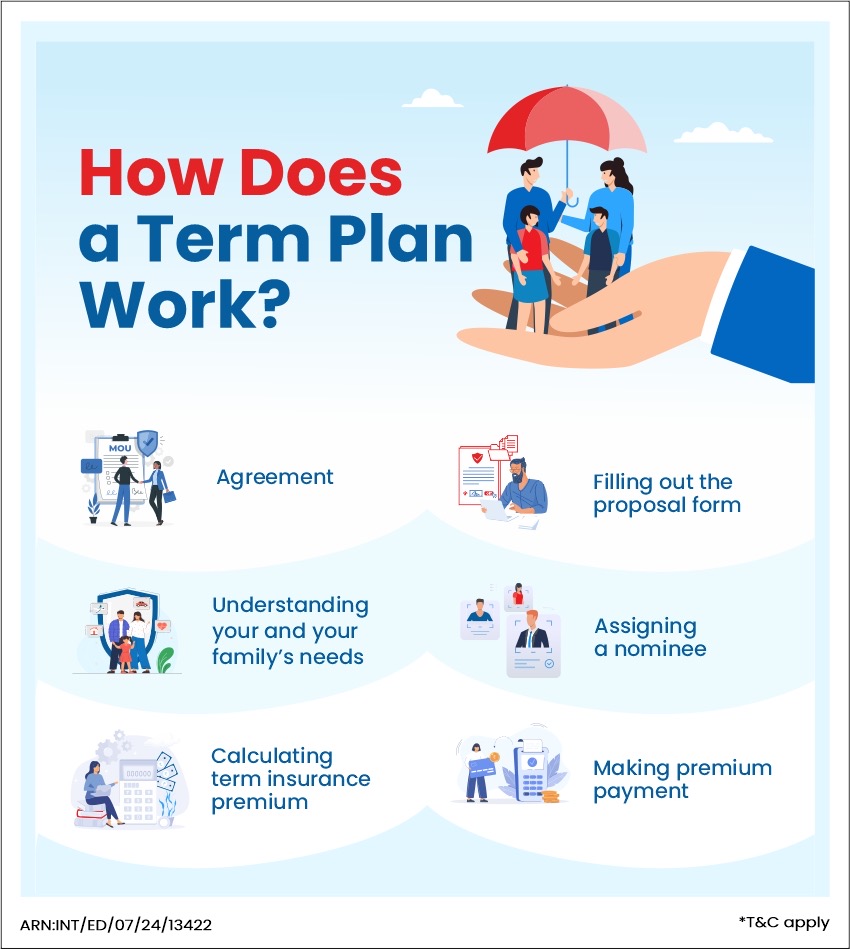

How Term Life Insurance Works

“Steps to get a Term Plan| HDFC Life” from www.hdfclife.com and used with no modifications.

Understanding the mechanics of a term life policy helps you make smarter decisions when choosing coverage. The structure is straightforward, but a few key details — especially around premiums and what happens at the end of your term — are worth knowing before you sign anything.

Coverage Periods: 10, 20, and 30-Year Terms Explained

Term lengths typically come in 10, 15, 20, 25, or 30-year options. A 10-year term works well for someone nearing retirement who only needs coverage for a short window. A 20-year term is one of the most popular choices for parents of young children, covering the years when dependents are most financially vulnerable. A 30-year term is ideal for young adults who want to lock in low rates early and cover a long mortgage or provide extended income replacement.

How Premiums Are Locked In for Your Term

One of the biggest advantages of term life insurance is premium stability. Once your policy is issued, your premium is fixed for the entire term. A healthy 30-year-old who locks in a 20-year level term policy today will pay the same monthly premium at age 49 as they did on day one. This predictability makes budgeting simple and protects you from rising insurance costs as you age.

What Happens When Your Term Ends

When your term expires, coverage ends and no death benefit is paid. At that point, you typically have three options:

- Let the policy lapse — if your financial obligations have significantly reduced and you no longer need coverage.

- Renew the policy annually — most insurers allow this, but premiums will increase each year based on your current age, often substantially.

- Convert to a permanent policy — if your policy includes a conversion rider, you can switch to whole life or universal life insurance without a new medical exam.

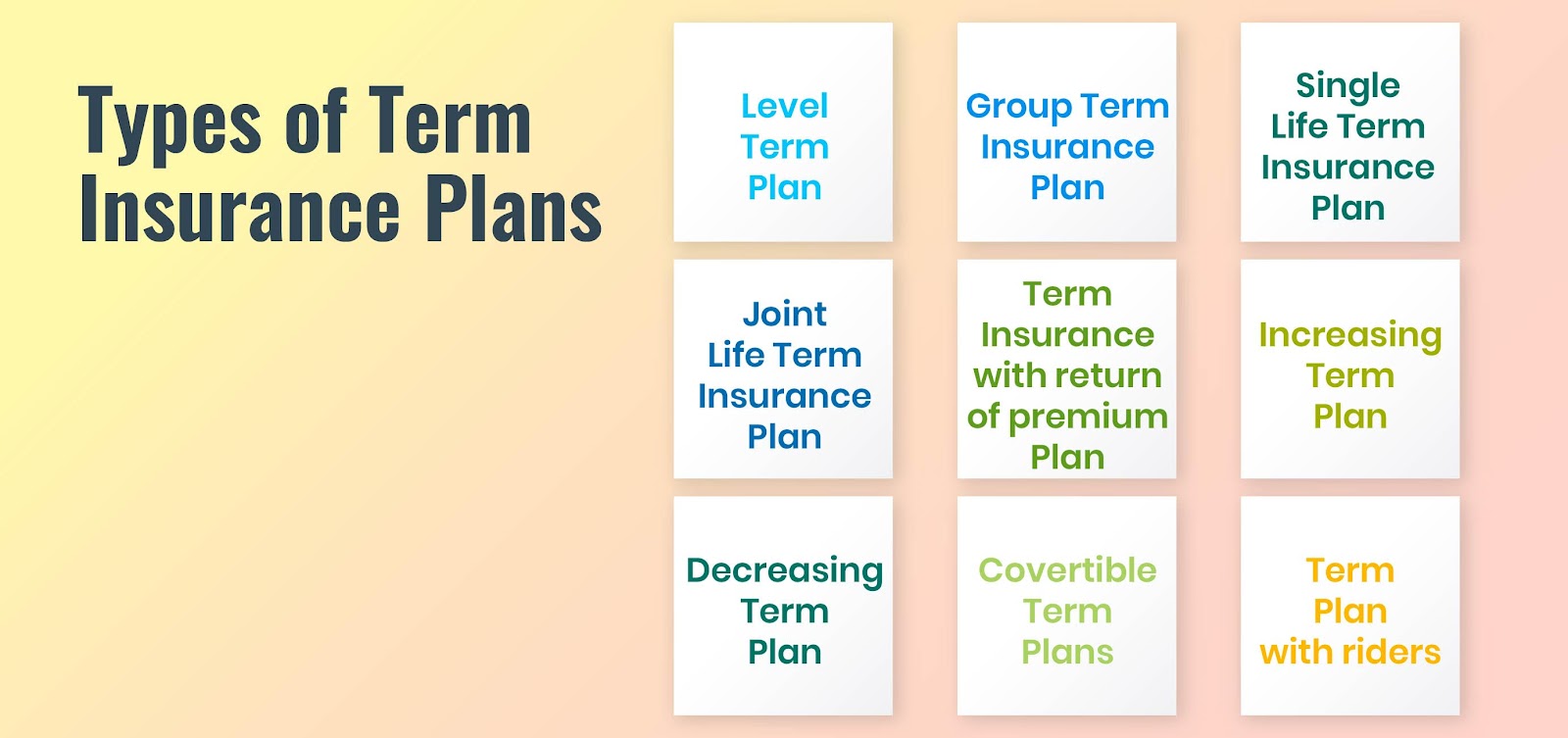

Types of Term Life Insurance

“Type of Term Insurance Plan” from zfunds.in and used with no modifications.

Not all term life policies are built the same. Choosing the right type depends on your financial goals, how long you need coverage, and whether you want the flexibility to change course later.

1. Level Term Life Insurance

This is the most common type. Your premium and death benefit remain constant throughout the entire term. What you pay on day one is what you pay on the last day of the policy. Level term is the best fit for most people because of its simplicity and cost predictability.

2. Annual Renewable Term Life Insurance

Annual renewable term (ART) provides coverage one year at a time, with the option to renew each year without a new medical exam. Premiums start lower than level term but increase every year as you age. This can make ART cost-effective for very short-term needs but expensive over time if you need coverage for more than a few years.

3. Group Term Life Insurance

Group term life insurance is typically offered through an employer as part of a benefits package. Coverage is based on a multiple of your salary — often one to two times your annual income — and premiums are either fully covered by the employer or split between employer and employee. While it’s a convenient and often free benefit, group coverage alone is rarely sufficient for most families, and it disappears the moment you change jobs.

4. Convertible Term Life Insurance

Convertible term life insurance gives you the flexibility to convert your policy into a permanent life insurance policy — such as whole life or universal life — without undergoing a new medical exam. This is a powerful option if your health changes during your term and you’re concerned about qualifying for new coverage later. The conversion rider is often built into the policy at no extra cost, though not every insurer offers it.

- No new medical exam required when converting, regardless of any health changes since the original policy was issued.

- You lock in insurability early, even if a later diagnosis would otherwise make coverage difficult or expensive to obtain.

- Premiums will increase after conversion since permanent policies cost more than term policies by nature.

- Conversion windows are limited — most policies require you to convert before a specific age or before the term ends.

If you’re young and healthy but want a safety net in case things change, buying a convertible term policy is one of the smartest moves you can make. It gives you affordable coverage now with a guaranteed path to permanent protection later. If you’re curious about what happens if you outlive your term life policy, it’s important to explore your options.

Each of these four types serves a specific purpose. For most people shopping for straightforward, affordable protection, level term life insurance hits the sweet spot. But understanding all four options ensures you’re not leaving flexibility or savings on the table.

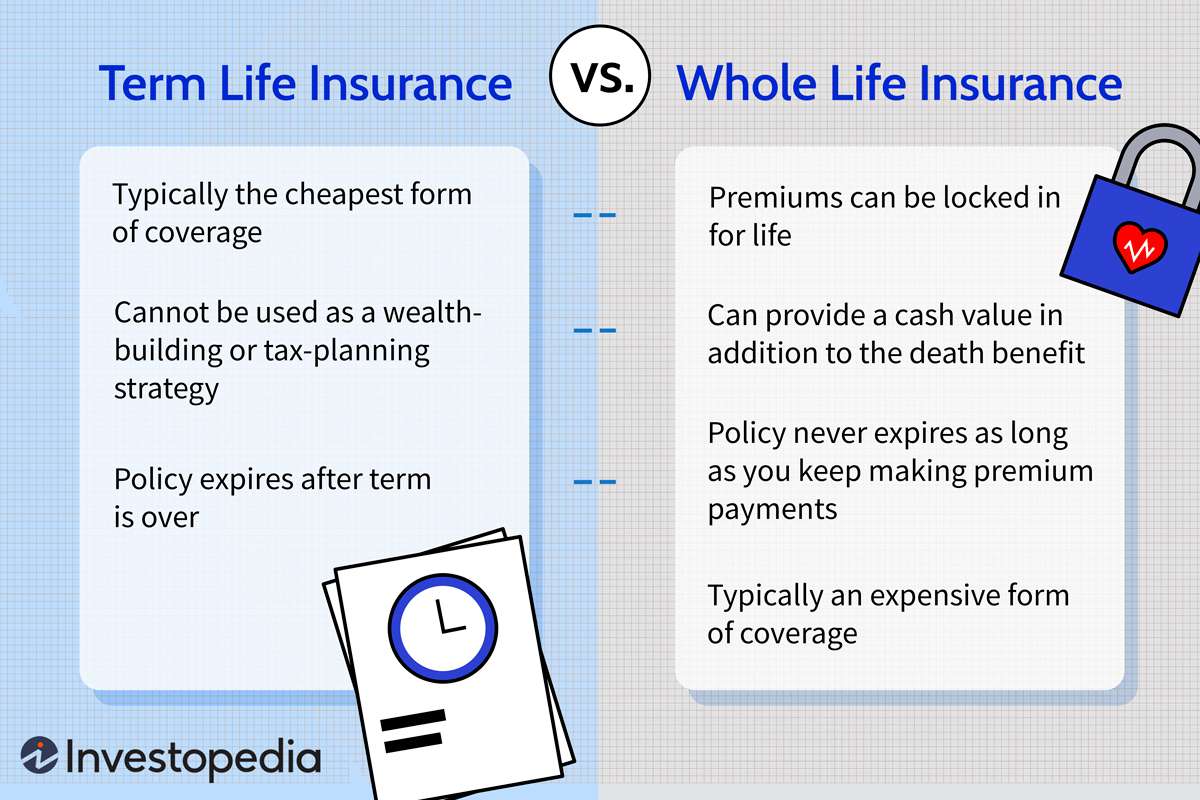

Term Life vs. Whole Life Insurance

“Term vs. Whole Life Insurance: What’s …” from www.investopedia.com and used with no modifications.

The most common question people ask when shopping for life insurance is whether they should buy term or whole life. Both provide a death benefit, but they work very differently — and the right choice comes down to what you actually need coverage for and how long you need it.

Cost Differences Between Term and Whole Life

Term life insurance is dramatically cheaper than whole life insurance for the same death benefit amount. A healthy 35-year-old non-smoking male might pay around $30 to $40 per month for a $500,000 20-year level term policy. The equivalent whole life policy could cost five to fifteen times more per month. That cost difference is significant, especially for young families working within a tight budget.

Cash Value: What Term Life Does Not Offer

The main reason whole life insurance costs more is the cash value component. A portion of every whole life premium goes into a savings-like account that grows over time on a tax-deferred basis. Policyholders can borrow against this cash value or surrender the policy for its accumulated value.

Term life insurance has no cash value whatsoever. If you outlive your term, you receive nothing back. To some people, this feels like wasted money — but that perspective misses the point. You’re not investing; you’re buying pure protection. The premium savings compared to whole life can be invested separately and often generate better long-term returns. For those looking for more information, Ranwell Insurance offers trusted guidance on life insurance options.

Think of it this way: term life is like renting an umbrella during rainy season. You don’t own it forever, but it does exactly what you need it to do when the weather turns bad — at a fraction of the cost of buying one permanently.

- Term life — lower premiums, no cash value, coverage for a set period.

- Whole life — higher premiums, builds cash value, lifetime coverage.

- Best for budget-conscious buyers — term life wins on affordability every time.

- Best for estate planning or lifetime coverage needs — whole life offers permanence that term cannot match.

Which Policy Fits Your Situation

Term life insurance is the right fit if you have time-sensitive financial responsibilities — a mortgage, young children, or income replacement needs that will eventually resolve. Whole life makes more sense for those who want lifelong coverage, have maxed out other tax-advantaged accounts, or need insurance as part of an estate planning strategy. For the vast majority of people, especially those early in their financial journey, term life is the most practical and cost-effective starting point.

Who Should Get Term Life Insurance

“10 Best Term Life Insurance Companies …” from www.insuranceproviders.com and used with no modifications.

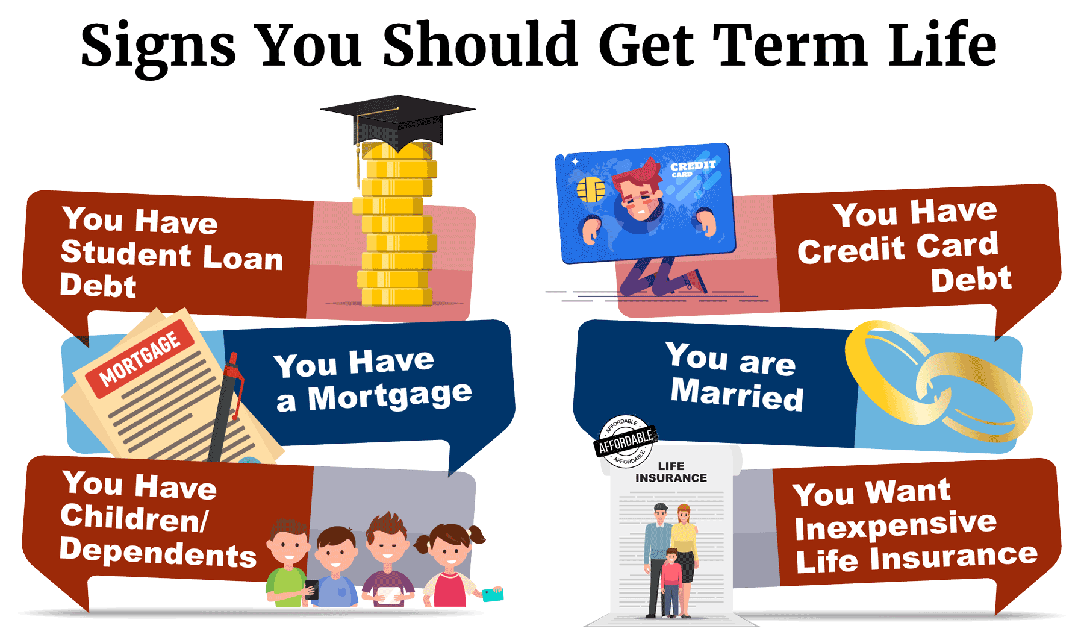

Term life insurance is not one-size-fits-all, but it fits a very wide range of people. If someone depends on your income — or if your death would leave others burdened with your financial obligations — term life coverage is likely the right move.

Young Families With Dependents

Parents with young children have the most to gain from term life insurance. The years between having a child and that child becoming financially independent represent your highest-risk window. If something happens to you during this period, your family loses not just your presence but your income, your contributions to the mortgage, childcare costs, and future education expenses. If you’re looking for life insurance in Georgia, it’s important to find a plan that covers all these potential needs.

A 30-year term policy purchased at age 28 or 30 can cover your family through the most financially vulnerable decades of your life — all while locking in the lowest possible premiums before age-related cost increases kick in.

Example: A 29-year-old mother of two takes out a $750,000 20-year level term policy. Her monthly premium is approximately $35. Over 20 years, she pays roughly $8,400 total. If she passes away in year 12, her family receives $750,000 tax-free — enough to pay off the mortgage, fund two college educations, and replace years of lost income. That is an extraordinary return on a modest monthly commitment.

The earlier you buy, the cheaper your premiums will be. Waiting even five years can meaningfully increase what you pay every month for the same level of coverage.

People With Significant Debt or a Mortgage

If you carry a mortgage, car loan, student debt, or any significant financial obligation that a surviving partner or family member would struggle to handle alone, term life insurance is a direct solution. A policy sized to cover your outstanding debt ensures that a death in the family doesn’t become a financial catastrophe on top of a personal one. Matching your term length to your mortgage payoff timeline is one of the most commonly recommended strategies among financial planners.

How to Choose the Right Term Length and Coverage Amount

“Term Insurance Coverage: How Much Do I …” from www.bandhanlife.com and used with no modifications.

Getting these two numbers right is the most important part of buying term life insurance. Too little coverage leaves your family exposed. Too long a term and you’re paying for protection you no longer need. The goal is to match your policy to your actual financial obligations — nothing more, nothing less.

Matching Your Term to Your Financial Obligations

The simplest rule of thumb: your term should last as long as your most significant financial obligation. If you have a 30-year mortgage, a 30-year term makes sense. If your youngest child is 3 years old and you want coverage until they’re financially independent at 22, a 20-year term gets you there. The goal is to make sure the policy is active during every year that your death would create serious financial hardship for someone else. To understand what happens if you outlive your policy, you can read more here.

How Much Coverage Do You Actually Need

A widely used starting point is the DIME formula — Debt, Income, Mortgage, and Education. Add up your total outstanding debt, multiply your annual income by the number of years your family would need income replacement, add your remaining mortgage balance, and factor in estimated education costs for your children. The sum gives you a solid baseline coverage target. For more insights, you can explore what happens if you outlive your term life policy.

- Debt: Total all non-mortgage debts — car loans, student loans, credit cards.

- Income: Multiply your annual income by the number of years until your youngest child is independent or you reach retirement age.

- Mortgage: Add your remaining mortgage balance.

- Education: Estimate future education costs for each dependent child.

Most financial planners recommend a death benefit of 10 to 12 times your annual income as a general benchmark. So if you earn $70,000 per year, a coverage amount between $700,000 and $840,000 is a reasonable starting range — then adjusted up or down based on your specific debt load and family situation.

Balancing Coverage Amount With Your Budget

More coverage is always better in theory, but only if you can consistently afford the premiums. A policy that lapses because you can’t keep up with payments protects nobody. Start with the coverage amount your budget can comfortably support, and consider laddering multiple smaller policies — for example, a $500,000 20-year term plus a $250,000 10-year term — to front-load coverage during your highest-need years while reducing premiums as obligations decrease over time. If you’re considering life insurance options in the Southeast, Ranwell Insurance offers trusted expertise to help you make informed decisions.

Term Life Insurance Is the Smart First Step Toward Financial Security

“Protect What Matters, Build What Lasts.” from www.cleverinsurance.org and used with no modifications.

Term life insurance does one thing exceptionally well: it puts a financial safety net under the people who depend on you, at a price most families can actually afford. It’s not a wealth-building tool, and it’s not designed to be. It’s designed to make sure that if the worst happens, the people you love have the financial breathing room to recover.

The window where term life matters most is exactly the window where most people are also managing mortgages, raising children, and building careers. That overlap is not a coincidence — it’s precisely why term life exists. The years when coverage is most critical are also the years when locking in low premiums is most achievable.

Whether you’re a 28-year-old with a new baby and a first mortgage, or a 45-year-old still carrying significant debt and dependents at home, term life insurance is almost always the most cost-effective way to close the gap between where your finances are today and where your family would need them to be without you. Start with the right term length, get the coverage amount right using the DIME method, and revisit your policy every few years as your financial picture evolves.

Frequently Asked Questions

Here are answers to the most common questions people ask when researching term life insurance for the first time.

Can You Have More Than One Term Life Insurance Policy?

Yes — and this strategy is more common than most people realize. Holding multiple term life policies simultaneously is completely legal and often financially smart. It allows you to tailor coverage amounts and term lengths to specific financial obligations rather than buying one oversized policy that covers everything at a higher premium.

Example: Policy Laddering Strategy

A 35-year-old with a mortgage, two young children, and $40,000 in student debt might structure coverage like this:

Policy 1: $500,000 — 30-year term — covers mortgage and long-term income replacement

Policy 2: $250,000 — 20-year term — covers child-rearing years and education costs

Policy 3: $100,000 — 10-year term — covers student debt payoff windowAs each shorter policy expires, total coverage decreases in step with decreasing financial obligations — and so does the total premium burden.

Insurers will typically assess your total coverage across all policies relative to your income and financial obligations before approving large amounts. Most insurers cap total coverage at somewhere between 25 and 30 times your annual income, though this varies by carrier and your age at application. If you’re curious about what happens when you outlive your policy, you can learn more about outliving a term life policy.

The laddering approach is particularly powerful for families in their 30s who have significant near-term obligations that will gradually decrease over time. Rather than locking into one massive premium, you front-load coverage when you need it most and let it scale down naturally as debts are paid off and children become independent. For those in the Southeast, Ranwell Insurance offers expertise in tailoring life insurance plans to suit these evolving needs.

Does Term Life Insurance Pay Out for Any Cause of Death?

In most cases, yes. Term life insurance covers death from natural causes, illness, accidents, and most other circumstances as long as the policy is active and premiums are current. The death benefit is paid regardless of whether death results from a heart attack, cancer, a car accident, or any other covered cause.

There are a small number of standard exclusions to be aware of. Suicide within the first two years of the policy (the contestability period) is typically excluded. Death resulting from fraud or material misrepresentation on the application — such as lying about a pre-existing health condition — can also void the policy. Some policies may exclude death during participation in certain high-risk activities, though this varies by insurer. Always read the exclusions section of your specific policy carefully.

Can You Convert Term Life Insurance to a Permanent Policy?

Yes, if your policy includes a conversion rider — and many level term policies do. Converting allows you to switch from term coverage to a permanent policy like whole life or universal life without submitting to a new medical exam. This is particularly valuable if your health has declined during your term and you would otherwise struggle to qualify for new coverage at reasonable rates.

Conversion windows are not unlimited. Most insurers require you to convert before a specified age — often between 65 and 70 — or before the end of your term, whichever comes first. If you think there’s any chance you’ll want permanent coverage later, choosing a term policy with a strong conversion rider from the start is a move worth making, even if you never end up using it. For more information on what happens if you outlive your term life policy, you can read this detailed guide.

What Happens if You Outlive Your Term Life Insurance Policy?

If you outlive your policy, coverage ends and no benefit is paid — this is the expected outcome for most policyholders. At that point you have the option to let it lapse entirely, renew the policy on an annual basis (at significantly higher age-based premiums), or convert to a permanent policy if that option is still available under your contract. If your financial obligations have largely resolved by the time your term ends — your mortgage is paid, your children are independent, your debts are cleared — letting the policy expire is often the right financial decision. For seniors in Georgia, getting life insurance can still be an option to consider.

Is Term Life Insurance Worth It if You Are Single With No Dependents?

For most single people with no dependents and no significant co-signed debt, term life insurance is a lower priority than other financial tools like an emergency fund, disability insurance, or retirement contributions. If nobody relies on your income and your death would not leave anyone financially burdened, the core purpose of term life insurance doesn’t fully apply to your situation right now.

That said, there are two scenarios where buying term life as a single person still makes financial sense. First, if you carry co-signed debt — a student loan with a parent as co-signer, for example — your death leaves that obligation entirely with them. A modest term policy covers that gap cleanly. Second, buying young and healthy locks in the lowest possible premiums for a future policy. A 25-year-old in excellent health will pay a fraction of what a 40-year-old with a health history pays for identical coverage.

If you anticipate having dependents within the next five to ten years — through marriage, children, or aging parents who may come to rely on your support — locking in a policy now while your health and age work in your favor is a financially sound move. The cost of waiting is almost always higher than the cost of starting early.

If you’re ready to explore your options and find a policy that fits your specific financial situation, connecting with a qualified life insurance resource is the most direct path to getting covered with confidence.

Ready to Compare Your Options?

Call (855) 508-5008 to speak directly with Ranwell Insurance about your coverage goals. We compare multiple carriers, explain your options clearly, and help you choose protection that fits your budget and long-term plans — without pressure.

You can also request a personalized quote and see how different coverage amounts and term lengths affect your monthly cost.