- No medical exam life insurance lets you skip the doctor’s office — no blood draws, no physicals, no waiting weeks for results.

- There are multiple types of no-exam policies, and choosing the wrong one could mean paying significantly more than you need to.

- You can still get competitive rates without a full medical exam, especially if you apply while you’re younger and healthier.

- Insurers still assess your health — they just do it differently, using data sources you may not expect.

- Ranwell insurance offers no-exam life insurance options worth comparing before you commit to any policy.

Getting life insurance from Ranwell Insurance doesn’t have to mean scheduling a doctor’s appointment, rolling up your sleeve for a blood draw, and waiting weeks to find out if you’re approved.

No medical exam life insurance is exactly what it sounds like — a life insurance policy you can get without undergoing a physical examination. For many families, this is the difference between actually getting coverage and putting it off indefinitely. The process is faster, less invasive, and increasingly competitive in terms of pricing. Aflac offers no medical exam life insurance options designed to help families get protected without the traditional hurdles.

That said, “no exam” doesn’t mean “no questions asked.” Understanding how these policies actually work — and what insurers are doing instead of a physical — is the key to finding a policy that genuinely fits your family’s needs without overpaying.

Skip the Doctor’s Office and Still Get Covered

“Hattiesburg Clinic” from www.hattiesburgclinic.com and used with no modifications.

Traditional life insurance has long required a paramedical exam — a process where a nurse or technician visits your home or a clinic to collect blood, urine, height, weight, and blood pressure data. The insurer uses this information to calculate your risk level and set your premium. It’s thorough, but it’s also slow, sometimes taking four to eight weeks from application to approval.

No medical exam life insurance cuts that process down dramatically. Many policies can be approved in days — or even minutes. This speed is one of the biggest draws for busy parents, people who have delayed getting coverage, or anyone who simply doesn’t want to deal with the traditional process.

What No Medical Exam Life Insurance Actually Means

At its core, no medical exam life insurance means the insurer will not require you to complete a physical exam as part of the application process. However, this does not mean the insurer skips assessing your health altogether — they just gather that information differently.

Instead of a paramedical exam, insurers may rely on:

- A health questionnaire completed during the application

- Access to your prescription drug history (Rx database)

- Motor vehicle records

- The MIB (Medical Information Bureau) database

- Previous life insurance applications you’ve submitted

- In some cases, electronic health records

The insurer builds a picture of your health risk using these data sources rather than a physical exam. Depending on your age and the coverage amount you’re applying for, this process can be surprisingly comprehensive — even without a single needle.

How It Differs From Traditional Life Insurance

The clearest difference is the absence of a physical exam, but the implications go beyond convenience. Traditional fully underwritten life insurance typically offers the widest range of coverage amounts and often the most competitive premiums for people in excellent health — because the insurer has the most complete picture of your risk.

No medical exam policies trade some of that precision for speed and accessibility. Here’s how the two approaches compare at a glance:

| Feature | Traditional Life Insurance | No Medical Exam Life Insurance |

|---|---|---|

| Medical Exam Required | Yes | No |

| Approval Time | 4–8 weeks | Minutes to a few days |

| Coverage Limits | Up to millions | Typically up to $500,000–$1M+ |

| Premiums | Often lower for healthy applicants | Can be slightly higher |

| Health Questions | Yes | Yes (varies by type) |

| Best For | Those wanting lowest cost possible | Those prioritizing speed and convenience |

For many families, the slightly higher premium of a no-exam policy is a worthwhile trade-off for the speed and simplicity of the process — especially when it means actually getting covered instead of delaying.

How No Medical Exam Life Insurance Works

“Medical Exam Life Insurance Policies” from www.provalife.com and used with no modifications.

Once you decide to apply for a no medical exam policy, the process moves quickly. Most applications are completed entirely online or over the phone, and the information you provide drives the entire underwriting decision.

What Replaces the Medical Exam

Insurers have gotten remarkably sophisticated at assessing risk without ever meeting you in person. The combination of prescription drug history, the MIB database, and motor vehicle records gives underwriters a surprisingly detailed snapshot of your health and lifestyle. Some carriers have also begun using algorithmic underwriting — where your application data is run through a predictive model that estimates your health risk based on thousands of data points.

This is why honesty on your application matters more than most people realize. Insurers aren’t just taking your word for it — they’re cross-referencing your answers against multiple data sources. A discrepancy between what you report and what shows up in your prescription history, for example, can result in a denied claim for your family down the road — even if the policy was issued. For more information, you might consider reading about how Ranwell Insurance can assist with life insurance needs.

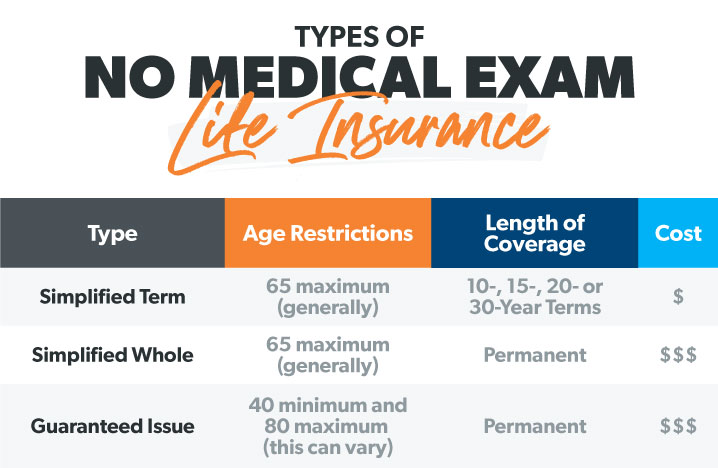

Types of No Medical Exam Life Insurance

“Life Insurance With No Medical Exam …” from www.ramseysolutions.com and used with no modifications.

Not all no-exam policies are built the same way. There are three main types, and each one works differently in terms of how much the insurer learns about your health, how quickly you get approved, and how much you’ll pay.

Accelerated Underwriting

Accelerated underwriting is the closest thing to traditional life insurance without the exam. You’ll answer a detailed health questionnaire, and the insurer uses data sources to verify your responses and assess risk. If everything checks out, you can get approved in days — sometimes hours — with coverage amounts that can reach $1 million or more and premiums that are competitive with fully underwritten policies. For those interested in life insurance options in Georgia, Ranwell Insurance offers insights on securing coverage efficiently.

The catch? Eligibility often depends on your age and health profile. Most carriers cap accelerated underwriting eligibility at age 60 or younger, and if your data raises any flags, they may require a full exam after all. But for healthy applicants who simply want to avoid the inconvenience of a paramedical exam, this is often the best option on the market.

Simplified Issue Life Insurance

Simplified issue policies skip the exam entirely and replace it with a short health questionnaire — typically between 5 and 15 questions. There’s no database cross-referencing at the same depth as accelerated underwriting, which makes this type faster and more accessible for people with some health concerns.

Coverage limits are generally lower — often capped between $100,000 and $500,000 depending on the carrier — and premiums are typically higher than what you’d pay with accelerated underwriting or full underwriting. That said, simplified issue is a strong option for:

- People who have been declined for traditional life insurance

- Older applicants who may not qualify for accelerated underwriting

- Those with manageable pre-existing conditions like controlled high blood pressure

- Anyone who wants coverage quickly without navigating a complex application

Guaranteed Issue Life Insurance

Guaranteed issue is exactly what the name suggests — approval is guaranteed, regardless of your health history. There are no health questions, no database checks, and no possibility of being declined based on medical history. This makes it the most accessible type of no-exam life insurance, but it comes with significant trade-offs. For instance, if you’re wondering if a 70-year-old can get life insurance, guaranteed issue might be an option to consider.

Coverage amounts are typically capped between $5,000 and $25,000, making it primarily suited for final expense coverage — funeral costs, outstanding debts, or small end-of-life expenses. Premiums are considerably higher per dollar of coverage than any other life insurance type. Most guaranteed issue policies also include a graded death benefit, meaning if you pass away within the first two to three years of the policy, your beneficiaries may only receive a refund of premiums paid rather than the full death benefit.

Important: Guaranteed issue life insurance is not ideal as a primary income replacement policy. It’s best used as a supplemental layer of coverage for final expenses, particularly for seniors between ages 50 and 85 who may not qualify for other types of coverage.

Who Should Consider No Medical Exam Life Insurance

“Do I Need No-Medical Life Insurance …” from www.policyadvisor.com and used with no modifications.

The appeal of no-exam coverage is broad, but it’s particularly well-suited for specific situations. If any of the following scenarios apply to you, a no-exam policy may be worth prioritizing over a traditional fully underwritten policy.

People who need coverage fast are one of the most common use cases. Life events — a new baby, a new mortgage, a business partnership — can create an immediate need for life insurance that a six-week underwriting process simply can’t accommodate. A simplified issue or accelerated underwriting policy can close that gap quickly.

Those with a fear of needles or medical anxiety represent a larger portion of the uninsured population than most people realize. If the prospect of a paramedical exam has been your reason for delaying coverage, a no-exam policy removes that barrier entirely — and getting some coverage in place is always better than waiting for the “perfect” policy.

Older adults who want straightforward coverage without medical complications often find that simplified issue or guaranteed issue policies give them access to protection they might otherwise struggle to obtain. And healthy applicants in their 30s and 40s who simply want a faster, more convenient process can often get excellent rates through accelerated underwriting without sacrificing meaningful coverage.

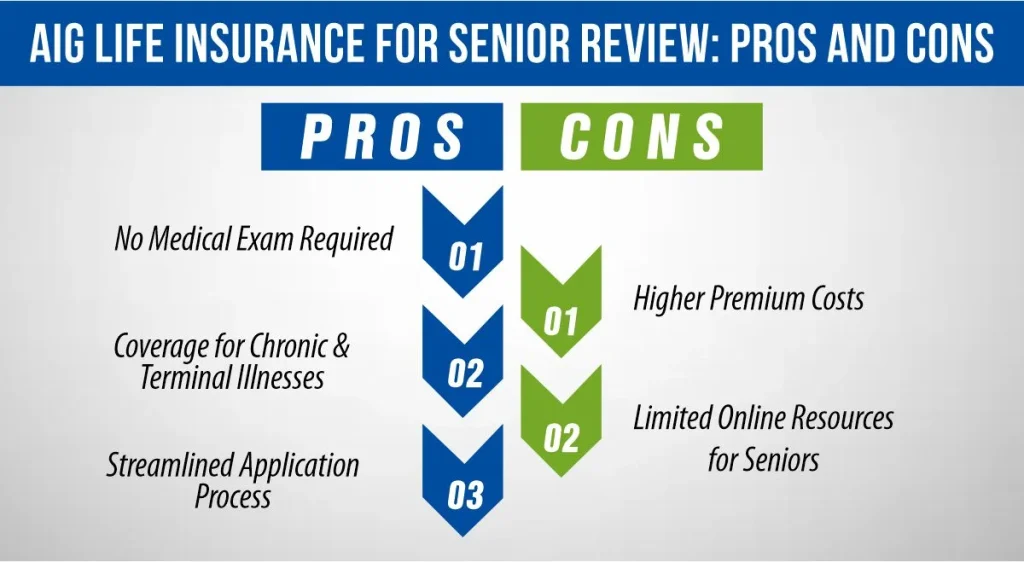

Pros and Cons of No Medical Exam Life Insurance

“AIG Life Insurance for Senior Review …” from mlifeinsurance.com and used with no modifications.

Like any financial product, no medical exam life insurance comes with genuine advantages and real limitations. Knowing both sides helps you make a decision that actually serves your family — not just one that feels convenient in the moment.

The Advantages

Speed and accessibility are the two biggest selling points. The application process can take as little as 15 minutes, and approval can come through the same day. For families who have been putting off life insurance because the traditional process felt overwhelming, this is often the nudge they need to finally get covered. If you’re in the Southeast, Ranwell Insurance can help you find the right policy quickly and efficiently.

No-exam policies also tend to be more inclusive. People with manageable health conditions that might complicate a full underwriting process — controlled diabetes, a history of anxiety, or a past cancer diagnosis that’s now in remission — often have better luck with simplified issue policies than they would navigating the full paramedical exam route.

Other notable advantages include:

- No scheduling or coordinating a paramedical exam appointment

- No fasting or preparing for blood draws

- Fully digital application process with most carriers

- Faster peace of mind for your family

- Competitive pricing through accelerated underwriting for healthy applicants

The Limitations

The most significant limitation is cost relative to coverage. Because the insurer has less health data to work with, they take on more risk — and they price that into your premium. For a healthy 35-year-old, the difference in premium between a fully underwritten policy and a simplified issue policy for the same coverage amount can be notable over the life of the policy.

Coverage caps are another factor. While accelerated underwriting has pushed these limits higher — some carriers now offer up to $1 million or more without an exam — simplified issue and guaranteed issue policies often top out at amounts that may not be sufficient to replace income or cover a mortgage for young families with significant financial obligations.

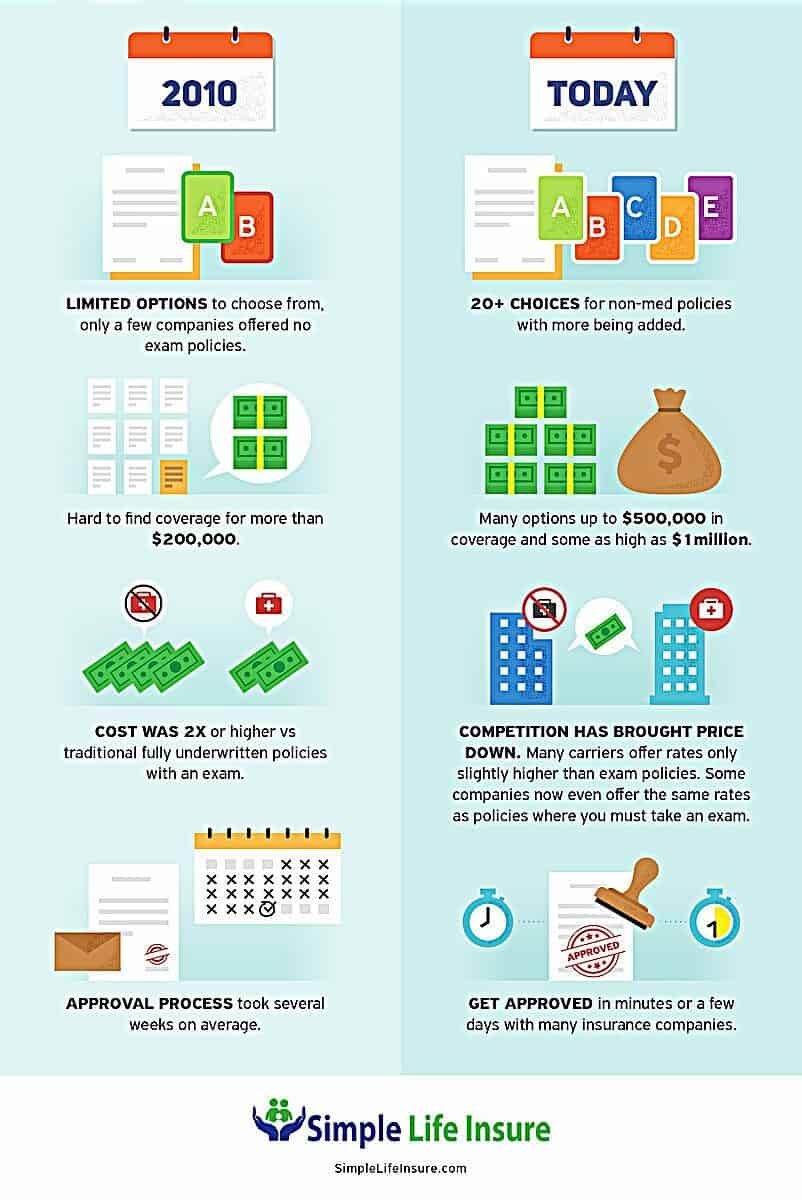

How Much Does No Medical Exam Life Insurance Cost

“Best No-Exam Life Insurance Companies …” from simplelifeinsure.com and used with no modifications.

Pricing varies significantly based on the type of policy, your age, the coverage amount, and the carrier. As a general benchmark, a healthy 35-year-old non-smoker might pay between $25 and $40 per month for a $500,000 20-year term life policy through accelerated underwriting — rates that are competitive with many fully underwritten policies.

Simplified issue policies for the same applicant and coverage amount might run 10% to 40% higher, depending on the carrier and the specific health questions answered. Guaranteed issue policies are priced at a premium relative to their low coverage amounts, often costing more per $1,000 of coverage than any other life insurance type.

The key variables that affect your premium include:

- Age: Younger applicants consistently pay less, and eligibility for accelerated underwriting typically decreases after age 60

- Gender: Women statistically live longer and generally pay lower premiums

- Coverage amount: Higher face values mean higher premiums

- Policy type: Term is less expensive than whole life regardless of exam status

- Tobacco use: Smokers pay significantly more across all policy types

- Policy term length: A 30-year term costs more than a 10-year term for the same coverage amount

How to Choose the Right No Medical Exam Policy

“Life Insurance With No Medical Exam …” from www.ramseysolutions.com and used with no modifications.

Start by identifying why you need coverage and how much your family would realistically need if you were gone. A common starting point is 10 to 12 times your annual income, though your specific mortgage balance, number of dependents, and existing savings will shape that number significantly.

From there, work through the type of policy that fits your situation. If you’re healthy and under 60, accelerated underwriting should be your first stop — you’ll get the best rates without the exam. If you have some health history that might complicate things, simplified issue gives you a cleaner path to coverage. Guaranteed issue should be reserved for situations where other options genuinely aren’t available.

When comparing carriers, look beyond the premium. For instance, it’s important to understand how no exam life insurance works before committing.

- Financial strength rating — Look for carriers rated A or better by AM Best

- Graded benefit period — Understand exactly when your full death benefit kicks in

- Conversion options — Can you convert a term policy to permanent coverage later without an exam?

- Riders available — Accelerated death benefit, waiver of premium, and child riders add meaningful value

- Coverage caps — Make sure the maximum available coverage actually meets your family’s needs

Frequently Asked Questions

Can I get no medical exam life insurance with pre-existing conditions?

Yes, in many cases. Simplified issue policies are specifically designed to accommodate applicants with health history that might complicate full underwriting. Conditions like controlled high blood pressure, type 2 diabetes, and past mental health treatment don’t automatically disqualify you. Guaranteed issue policies accept all applicants regardless of health history, though coverage amounts are limited.

Is no medical exam life insurance worth it?

No medical exam life insurance is worth it when the alternative is having no coverage at all. For healthy applicants using accelerated underwriting, it can be just as cost-effective as a traditional policy with far less hassle. For those who need coverage quickly or have health concerns, the slightly higher cost is often a reasonable trade-off for the accessibility and speed it provides. For more information on life insurance options, Ranwell Insurance offers expert guidance tailored to your needs.

How quickly can I get approved?

Approval timelines vary by policy type. Accelerated underwriting and simplified issue policies can result in same-day or next-day approval in many cases. Guaranteed issue policies are typically approved immediately upon application completion, since no health assessment is required.

What is the maximum coverage I can get without a medical exam?

Coverage limits depend on the carrier and the type of policy. Accelerated underwriting policies from major carriers can go up to $1 million or more. Simplified issue policies typically cap between $100,000 and $500,000. Guaranteed issue policies generally max out between $5,000 and $25,000.

The Bottom Line

No medical exam life insurance has matured significantly — what was once a niche, expensive alternative to traditional coverage has become a legitimate, accessible option for millions of families. The right policy depends on your health profile, how much coverage you need, and how quickly you need it in place, but in almost every case, having some coverage is better than delaying for the perfect policy that never gets purchased.

Ready to Compare Your Options?

Call (855) 508-5008 to speak directly with Ranwell Insurance about your coverage goals. We compare multiple carriers, explain your options clearly, and help you choose protection that fits your budget and long-term plans — without pressure.

You can also request a personalized quote and see how different coverage amounts and term lengths affect your monthly cost.