Article At A Glance

-

Mortgage protection life insurance pays off your remaining mortgage balance if you die during the policy term — keeping your family in their home.

-

Unlike standard term life insurance, the death benefit on most mortgage protection policies decreases over time as your loan balance drops, but your premiums stay the same.

-

Most mortgage protection policies skip the medical exam — which sounds great, but it’s one of the key reasons it often costs more than comparable term life coverage.

-

Healthy homeowners may find that a standard term life insurance policy offers better value and more flexibility for their family’s financial needs.

-

There’s a specific type of homeowner for whom mortgage protection life insurance genuinely makes sense — and it might surprise you.

Your Mortgage Is Likely Your Biggest Debt — Here’s How to Protect It

“Is Mortgage Protection Life Insurance …” from www.pinnaclequote.com and used with no modifications.

For most families, the mortgage is the single largest financial obligation they’ll ever carry — and mortgage protection life insurance is designed to make sure that debt doesn’t outlive you.

Housing payments make up the largest share of living costs in the United States. If the primary earner in a household dies unexpectedly, that monthly mortgage payment doesn’t pause for grief. Mortgage protection life insurance steps in to cover that balance, giving surviving family members something invaluable: the ability to stay in their home without financial panic. Understanding your coverage options early is one of the most important financial decisions a homeowner can make.

But this type of policy isn’t automatically the right choice for every homeowner. Whether it’s a smart buy or an overpriced product depends almost entirely on your health, your financial situation, and what you actually need life insurance to do for your family.

What Is Mortgage Protection Life Insurance?

“What Is Mortgage Protection Insurance …” from www.bankrate.com and used with no modifications.

Mortgage protection life insurance is a type of term life insurance policy designed with one specific job: pay off your mortgage if you die before it’s paid off. The coverage amount is tied directly to your outstanding mortgage balance, and the policy term is generally set to match the length of your home loan — typically 15 or 30 years. For those interested in exploring more about life insurance options, Ranwell Insurance offers insights as trusted life insurance experts serving the Southeast.

It’s a form of credit life insurance, meaning the benefit is structured around a specific debt rather than providing a general payout to your beneficiaries. In most cases, the death benefit goes directly toward paying off the mortgage, not into your family’s hands to use as they see fit.

How It Differs From Standard Term Life Insurance

Standard term life insurance pays a fixed death benefit to your named beneficiaries, who can use the money for anything — mortgage payments, living expenses, college tuition, or any other financial need. Mortgage protection life insurance, by contrast, is narrowly focused. The payout is typically sent directly to the lender, not your family, meaning your loved ones don’t get to decide how the money is used. For those considering their options, what happens if you outlive your term life policy is an important question to explore.

There’s another critical difference: the death benefit amount. With a standard term policy, your $300,000 coverage stays at $300,000 for the life of the policy. With most mortgage protection policies, the benefit shrinks over time as your loan balance decreases — while your premium stays flat. That’s a significant distinction in value.

How It Differs From Private Mortgage Insurance (PMI)

These two products are frequently confused, but they serve completely different purposes. Private mortgage insurance (PMI) protects the lender — not you — if you default on your loan. It’s typically required on conventional loans when your down payment is less than 20%. Mortgage protection life insurance, on the other hand, is entirely optional and protects your family by paying off the mortgage if you die.

How the Death Benefit Works

When you take out a mortgage protection policy, the initial death benefit is set equal to your current mortgage balance. As you make monthly payments and your loan balance decreases, the death benefit decreases in parallel. If you pass away 10 years into a 30-year mortgage, the policy pays off whatever balance remains at that point — not the original loan amount. For more information on term life policies, check out this article.

This decreasing benefit structure is one of the most important features to understand before purchasing. You’re paying consistent premiums throughout the policy for a benefit that provides less and less coverage as time goes on.

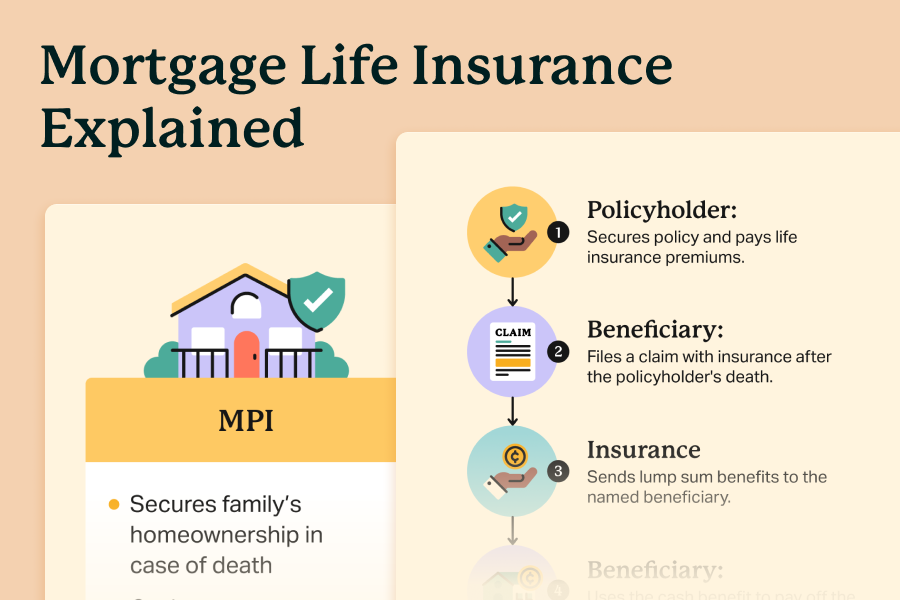

How Mortgage Protection Life Insurance Works

“Mortgage Life Insurance Explained …” from choicemutual.com and used with no modifications.

The mechanics of a mortgage protection policy are straightforward, but the details matter a great deal when you’re comparing it to other life insurance options.

Decreasing Death Benefit Over Time

Example: You take out a $350,000 mortgage on a 30-year term and purchase a matching mortgage protection policy. In year one, your death benefit is $350,000. By year 15, your remaining loan balance might be around $220,000 — so that’s all the policy would pay out. Meanwhile, your monthly premium has remained the same since day one. You’re paying the same amount for significantly less protection.

This structure is the core trade-off of mortgage protection insurance. The policy does exactly what it promises — it covers your outstanding mortgage balance — but it does so in a way that delivers diminishing value over time relative to what you’re paying in premiums.

Fixed Premiums Throughout the Policy Term

One feature that mortgage protection insurance shares with standard term life is fixed premiums. You lock in your rate at the time of purchase, and that amount stays consistent for the entire policy term. Your premium is calculated based on factors like your age, the loan amount, and the policy term length — and in many cases, your health plays a smaller role than it would with a traditional policy.

The fixed premium is often marketed as a benefit, and it genuinely is one — particularly for buyers who expect their income to be stable. Knowing exactly what you’ll pay each month makes budgeting straightforward.

No Medical Exam Required in Most Cases

Most mortgage protection life insurance policies are issued on a guaranteed acceptance or simplified issue basis, meaning there’s either no medical exam at all or just a basic health questionnaire. This is a significant advantage for homeowners who have pre-existing conditions or health histories that would result in a declined application or very high premiums on a standard term life policy.

However, this accessibility comes at a cost. Because the insurer is taking on more risk by not fully evaluating your health, they price that risk into the premium. Healthy individuals who qualify for standard term life will almost always find better value outside of a mortgage protection policy.

Policy Riders You Can Add

Some mortgage protection policies allow you to customize coverage with optional riders. These add-ons can expand what the policy covers beyond just death, making it a more versatile financial tool depending on your situation.

-

Disability rider: Covers your mortgage payments if you become disabled and can no longer work

-

Critical illness rider: Pays out a lump sum if you’re diagnosed with a covered condition like cancer, stroke, or heart attack

-

Unemployment rider: Temporarily covers mortgage payments if you lose your job involuntarily

-

Return of premium rider: Refunds your premiums if you outlive the policy term — though this significantly increases your monthly cost

Not every insurer offers all of these riders, and adding them will increase your premium. But for homeowners who want broader protection than a standard mortgage protection policy provides, they’re worth asking about when comparing quotes.

How Much Does Mortgage Protection Life Insurance Cost?

“Mortgage Life Insurance Cost …” from www.policyme.com and used with no modifications.

Mortgage protection life insurance is generally more expensive per dollar of coverage than a comparable term life insurance policy. The no-medical-exam feature that makes it accessible is the same feature that drives the price up — insurers price for the unknown risk they’re accepting by skipping health underwriting.

Key Factors That Affect Your Premium

Several variables determine what you’ll pay for mortgage protection coverage. Understanding these can help you anticipate costs before you start shopping.

-

Age: The older you are at the time of purchase, the higher your premium

-

Loan amount: A larger mortgage balance means a higher initial death benefit, which increases cost

-

Policy term: A 30-year term will cost more than a 15-year term for the same loan amount

-

Gender: Women statistically live longer, so they typically pay lower premiums

-

Health (when applicable): If the insurer does ask health questions, any disclosed conditions can affect your rate

-

Riders selected: Each add-on increases your monthly premium

How It Compares in Cost to Term Life Insurance

For healthy applicants, the cost difference between mortgage protection insurance and standard term life is notable. A term life policy requires full medical underwriting, which actually works in your favor if you’re in good health — insurers reward low-risk applicants with significantly lower premiums. A healthy 35-year-old could potentially secure a $300,000 term life policy at a fraction of what a mortgage protection policy for the same amount would cost.

The other cost consideration is value over time. With a term life policy, your $300,000 death benefit stays at $300,000 for the entire term. Your family could use that payout to cover the mortgage and still have funds left for other expenses. With mortgage protection insurance, the death benefit shrinks as your loan balance decreases, but your premium doesn’t. Over a 30-year term, that gap in value becomes increasingly difficult to justify for most healthy homeowners.

Pros and Cons of Mortgage Protection Life Insurance

“paying off a mortgage” from www.healio.com and used with no modifications.

Like any financial product, mortgage protection life insurance has genuine strengths and real drawbacks. Neither side of the equation should be ignored when you’re deciding whether this policy fits your situation.

The honest answer is that this product works well for a narrow group of homeowners and works poorly for many others. Here’s a clear breakdown of both sides.

The Case For Getting It

-

Guaranteed or simplified acceptance: If health issues prevent you from qualifying for standard life insurance, this may be your best available option

-

Focused protection: If your sole priority is ensuring the mortgage gets paid and your family keeps the home, the policy does exactly that

-

Predictable premiums: Fixed monthly costs make budgeting straightforward with no surprises

-

Fast approval: Without a medical exam requirement, policies can often be issued quickly after application

-

Peace of mind for new homeowners: When you’ve just taken on a large mortgage and have limited savings or assets, having that specific debt covered can provide meaningful reassurance

The Case Against Getting It

-

Decreasing benefit, flat premium: You pay the same amount every month while receiving progressively less coverage — a poor value proposition over time

-

Lender receives the payout, not your family: Your beneficiaries have no flexibility in how the death benefit is used

-

More expensive than term life for healthy applicants: If you qualify for standard underwriting, you can almost always get better coverage for less money

-

Limited flexibility: The coverage is tied entirely to your mortgage — it doesn’t help with any other financial needs your family may have after you’re gone

Who Should Consider Mortgage Protection Life Insurance?

“Mortgage Protection Insurance: Who …” from www.ramseysolutions.com and used with no modifications.

This isn’t a product that fits everyone — but for certain homeowners, it can genuinely be the most practical option available.

The right candidate for mortgage protection life insurance typically has one or more characteristics that make standard life insurance difficult to obtain or financially out of reach. It fills a specific gap rather than serving as a general financial planning tool.

Before purchasing, it’s worth getting quotes for both mortgage protection insurance and a standard term life policy side by side. For many homeowners, that comparison alone will clarify which product makes more sense.

Homeowners With Health Issues That Block Standard Coverage

If you’ve been declined for traditional life insurance due to a pre-existing condition, a serious diagnosis, or a complicated health history, mortgage protection life insurance may be one of the few options available to you. The guaranteed or simplified acceptance underwriting process means that your health history has limited impact on your eligibility. For someone in this position, having a policy that at minimum protects the family home is far better than having no coverage at all. The higher cost is a real trade-off, but for homeowners with limited alternatives, it can be a worthwhile one. For more information on life insurance options, you can explore Ranwell Insurance’s offerings.

Early-Stage Mortgage Holders With Limited Assets

If you’ve recently closed on your first home and your savings are thin, mortgage protection life insurance offers a targeted safety net during the most financially vulnerable stage of homeownership. In the early years of a mortgage, your loan balance is at its highest — and your equity is at its lowest. If you haven’t yet built up savings, investments, or other assets your family could fall back on, having a policy that directly covers that large outstanding balance can make real financial sense.

This window of vulnerability typically narrows over time. As you build equity, grow your savings, and potentially upgrade to a standard term life policy, the need for mortgage-specific coverage diminishes. But in those early years — especially with dependents relying on your income — the focused protection of a mortgage protection policy can serve as a practical bridge.

Term Life Insurance Is Often the Better Choice — Here’s Why

“Term Life – Free Quote – Coverage As …” from www.njlifeandhealth.com and used with no modifications.

For most healthy homeowners, a standard term life insurance policy delivers more value, more flexibility, and a lower cost per dollar of coverage than mortgage protection life insurance. The death benefit stays fixed for the entire term, your family receives the payout directly and can use it however they need, and the premium reflects your actual health risk rather than a blanket rate designed for the highest-risk applicants.

Consider what your family actually needs if you’re gone — not just a paid-off house, but money to cover living expenses, childcare, outstanding debts, and daily costs that don’t stop just because the mortgage does. A $400,000 term life payout gives your family the financial breathing room to make real decisions. A mortgage protection policy pays the lender and leaves your family to figure out the rest on their own.

The math is straightforward for healthy applicants. Full medical underwriting rewards low-risk individuals with significantly lower premiums. The trade-off of submitting to a medical exam is almost always worth it when the result is better coverage at a lower monthly cost. Unless a health condition blocks you from standard underwriting, term life insurance is the stronger financial move for most homeowners.

The Right Coverage Protects More Than Your Home

Mortgage protection life insurance does one thing well — it ensures your mortgage gets paid if you die. For the right homeowner in the right circumstances, that focused protection has genuine value. But life insurance, at its core, is about protecting the financial future of the people who depend on you — and that need is almost always bigger than a single debt. Choosing the right policy means thinking beyond the mortgage and asking what your family would actually need to maintain their lives, their stability, and their options. If you’re in good health, a standard term life policy gives you all of that and more, for less money.

Frequently Asked Questions

Is mortgage protection life insurance the same as PMI?

No, they are entirely different products. Private mortgage insurance (PMI) protects the lender if you default on your loan and is typically required when your down payment is less than 20% on a conventional mortgage. Mortgage protection life insurance is optional, protects your family, and pays off your mortgage balance if you die during the policy term. One serves the bank’s interests; the other serves your family’s.

Can my lender require me to get mortgage protection life insurance?

No. Unlike PMI, mortgage protection life insurance is entirely optional. No lender can legally require you to purchase it as a condition of your home loan. You may receive marketing materials from lenders or insurers shortly after closing on your home, but purchasing a policy is always your choice. If you’re considering life insurance options, you might want to explore how a 70-year-old can get life insurance in Georgia.

If you ever feel pressured by a lender to buy a specific insurance product as a loan condition, that’s worth questioning carefully — and potentially reporting to your state’s insurance commissioner or consumer financial protection authority.

What happens to the death benefit if I pay off my mortgage early?

If you pay off your mortgage before the policy term ends, the coverage typically becomes unnecessary — but the policy itself doesn’t automatically cancel. You would need to contact your insurer to cancel the policy, and in most cases, you won’t receive a refund of premiums already paid unless you purchased a return of premium rider.

This is one of the lesser-discussed downsides of tying insurance directly to a specific debt. If your financial situation improves and you pay off your home loan ahead of schedule, you may end up paying premiums on a policy that no longer serves a practical purpose. Always review your coverage whenever your mortgage situation changes significantly.

Can I get mortgage protection life insurance if I have a pre-existing condition?

Yes — and this is actually one of the strongest use cases for mortgage protection life insurance. Because most policies are issued on a guaranteed acceptance or simplified issue basis, your health history has minimal impact on your eligibility. You can typically qualify regardless of pre-existing conditions that might disqualify you from standard term life insurance.

The trade-off is cost. Insurers price guaranteed acceptance policies to account for the higher risk they’re taking on by skipping full medical underwriting. If you have a serious health condition, expect to pay a higher premium than a healthy applicant would — but for many people in this situation, having some coverage in place is far more important than optimizing for the lowest possible rate.

How long can I wait after closing to apply for mortgage protection life insurance?

There’s no hard deadline for applying after closing. You can purchase a mortgage protection policy at any point during your loan term — whether that’s the week you close or several years into repayment. However, waiting has a real cost: premiums increase with age, so the longer you wait, the more you’ll pay for the same coverage.

Many homeowners receive unsolicited mortgage protection offers in the weeks immediately following closing, as lender information becomes part of public record. While the timing might feel aggressive, it does coincide with the period when coverage arguably matters most — when your loan balance is at its highest and your home equity is at its lowest. For more information, you can read about mortgage protection insurance.

If you’re considering this type of coverage, the smartest move is to compare quotes for both mortgage protection insurance and a standard term life policy at the same time. That side-by-side comparison will give you the clearest picture of which option delivers the better value for your specific health profile and financial situation.

Looking for life insurance that fits your family’s needs?

Contact Ranwell Insurance today at (855) 508-5008 or request a free personalized quote. We help families compare life insurance options and choose coverage with confidence.