Key Takeaways

- Universal life insurance offers Macon residents flexibility to adjust premiums and death benefits as their financial situations change over time.

- The cash value component in universal life policies provides tax-advantaged growth potential while maintaining lifetime coverage.

- Unlike term insurance, universal life provides permanent protection with the added benefit of building equity you can access during your lifetime.

- Macon residents in their 30s-50s often find universal life insurance particularly valuable for long-term financial planning.

- There are several specialized types of universal life policies available in Macon GA, including indexed, variable, and guaranteed options to match different risk tolerances.

The insurance landscape in Macon, Georgia is evolving rapidly, with universal life insurance emerging as a particularly attractive option for residents seeking long-term financial security. This flexibility-focused permanent insurance solution is gaining traction as more Georgians recognize its unique advantages in today’s uncertain economic climate. Local insurance specialists are noting a significant uptick in interest from Macon residents who want coverage that adapts to their changing financial circumstances while building value over time.

Unlike traditional insurance products with rigid structures, universal life insurance offers Macon residents a dynamic approach to protection that grows and changes alongside their lives. This adaptability is especially valuable in a mid-sized city like Macon, where economic opportunities and challenges can shift quickly, requiring financial tools that provide both security and flexibility.

Why Macon GA Residents Are Flocking to Universal Life Insurance

“Universal Life Insurance – Ramsey” from www.ramseysolutions.com and used with no modifications.

Macon’s diverse population—from young professionals establishing careers to established families planning for retirement—increasingly gravitates toward financial products that offer customization. Universal life insurance stands out because it combines lifetime protection with adjustable features that traditional policies simply don’t provide. For Macon residents focused on long-term financial planning, the ability to modify coverage as circumstances change represents a significant advantage over more rigid insurance options.

- Flexibility to increase or decrease premium payments within certain limits

- Ability to adjust death benefit amounts as family needs evolve

- Cash value component that grows tax-deferred over time

- Option to access accumulated cash value through withdrawals or loans

- Potential to maintain coverage for life without fixed payment obligations

The demographic shift in Macon has also contributed to universal life’s popularity. As the city attracts more middle to upper-middle-income residents with complex financial planning needs, traditional term insurance often falls short. These newcomers to Macon frequently seek sophisticated insurance solutions that offer both protection and wealth-building potential—precisely what universal life provides.

The Flexible Premium Advantage

Universal life insurance stands apart from other permanent insurance options through its uniquely flexible premium structure. Macon residents facing income fluctuations—whether from seasonal business cycles, commission-based work, or unexpected expenses—particularly value this adaptability. During prosperous periods, policyholders can make larger premium payments, effectively “overfunding” their policy to build additional cash value. When finances are tight, they can reduce payments temporarily (within policy limits), using accumulated cash value to cover the difference. For more insights, you can explore why universal life insurance is gaining popularity.

This premium flexibility proves especially valuable in Macon’s diverse economic environment. Whether you’re employed in the healthcare sector at Navicent Health, working in manufacturing at one of the area’s industrial facilities, or running your own small business, income variability is a reality that universal life insurance accommodates. Unlike whole life policies that demand consistent premium payments regardless of your financial situation, universal life adjusts to your circumstances.

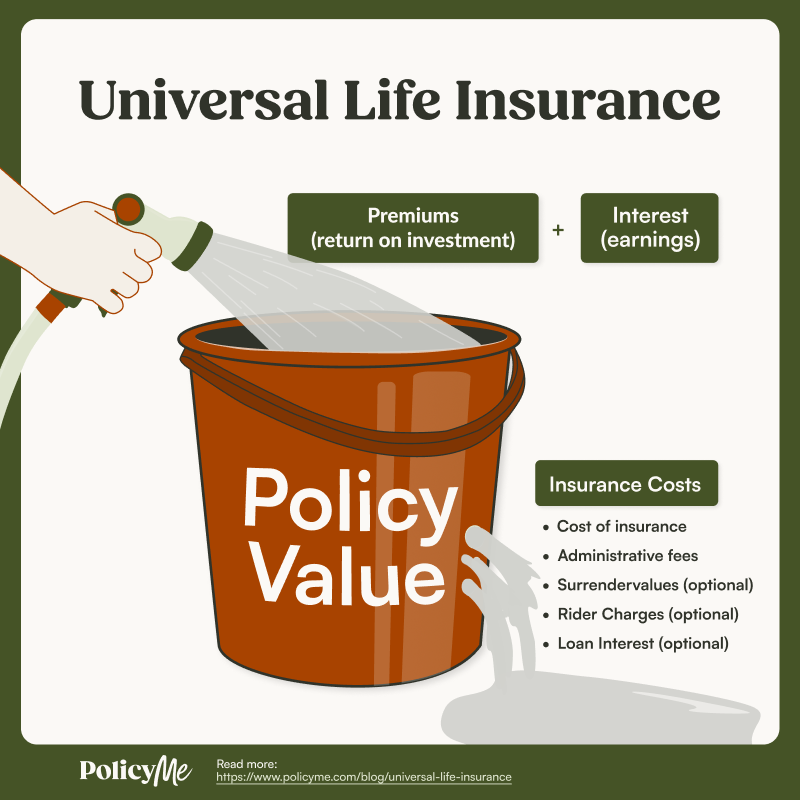

Cash Value Component: Your Money Working for You

Beyond providing a death benefit, universal life insurance functions as a financial asset that builds value throughout your lifetime. The cash value component grows tax-deferred, meaning you won’t pay taxes on its earnings until you withdraw them. For Macon residents focused on long-term wealth accumulation, this tax-advantaged growth represents a significant benefit compared to fully taxable investment accounts. If you’re considering your options, check out the top reasons to get insurance quotes in Macon, GA now.

The cash value grows based on the interest crediting method specified in your policy. Most universal life policies offered in Macon provide a minimum guaranteed interest rate, ensuring your cash value continues to grow even during periods of low market returns. This combination of growth potential and downside protection appeals to conservative Macon investors who want their insurance to double as a safe wealth-building vehicle.

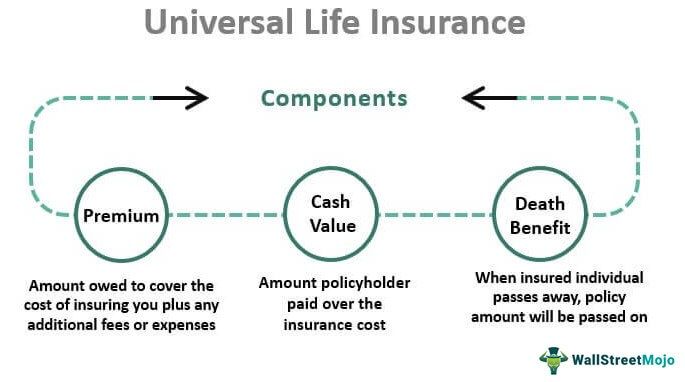

How It Compares to Term and Whole Life Policies

When evaluating insurance options in Macon, understanding how universal life compares to alternatives is crucial. Term life insurance offers temporary coverage—typically 10, 20, or 30 years—with lower initial premiums but no cash value component. Once the term expires, so does your coverage, regardless of how many years you’ve paid into the policy. For Macon residents seeking lasting protection that doesn’t disappear at a predetermined date, universal life provides continuity term policies cannot match.

- Term life: Temporary coverage, lower initial cost, no cash value accumulation

- Whole life: Permanent coverage, fixed premiums, guaranteed cash value growth, less flexibility

- Universal life: Permanent coverage, flexible premiums, adjustable death benefit, cash value growth potential

Whole life insurance, while also permanent, offers significantly less flexibility than universal life policies. Macon policyholders with whole life coverage commit to fixed premiums for life, with limited ability to adjust their payment schedule or death benefit amount. Universal life, by contrast, allows Macon residents to increase coverage when family responsibilities grow (such as after having children) or decrease coverage when obligations diminish (such as after children become financially independent).

5 Key Benefits Driving Universal Life’s Popularity in Macon

“Universal vs. Term Life Insurance …” from www.policyme.com and used with no modifications.

As Macon residents evaluate their long-term financial security options, universal life insurance has emerged as a particularly attractive solution for several compelling reasons. The unique combination of lifetime protection and financial flexibility addresses many of the specific concerns faced by Middle Georgia families. Let’s examine the five primary benefits making universal life insurance increasingly popular among Macon residents.

1. Lifetime Protection Without Fixed Payments

Universal life insurance provides Macon residents with coverage that never expires as long as the policy remains in force. Unlike term insurance that ends after a specific period, universal life can protect your family for your entire lifetime. This permanence gives policyholders peace of mind knowing their loved ones will receive a death benefit regardless of when the policyholder passes away.

What makes this lifetime coverage particularly appealing in Macon is that it doesn’t come with the rigid payment structure of traditional whole life policies. Residents can adjust their premium payments based on their current financial situation, making larger contributions when finances allow and smaller payments during tighter times (within policy limits). This flexibility proves especially valuable in Macon’s diverse economy, where income levels and employment stability can vary significantly across industries. For those interested in exploring further, whole life insurance remains a popular choice for long-term financial planning.

2. Tax-Advantaged Growth Potential

Universal life insurance offers Macon residents significant tax advantages that aren’t available with many other financial products. The cash value component grows tax-deferred, meaning you won’t pay taxes on the earnings as they accumulate. This tax-sheltered growth can substantially increase your policy’s value over time compared to fully taxable investments.

Additionally, policy loans and withdrawals can potentially be taken tax-free under certain circumstances, providing Macon families with tax-efficient access to their money when needed. For high-income residents seeking additional tax-advantaged savings vehicles after maximizing contributions to 401(k)s and IRAs, universal life insurance represents an attractive supplementary option with no contribution limits imposed by the IRS.

3. Access to Cash When You Need It

Universal life insurance provides Macon policyholders with ready access to their accumulated cash value through policy loans or withdrawals. This liquidity feature has proven especially valuable during economic uncertainties, allowing policyholders to tap into their policy’s value to cover unexpected expenses, fund a child’s education, or supplement retirement income without having to sell other investments at inopportune times. For those considering their options, understanding the benefits of whole life insurance can also be beneficial.

The ability to borrow against your policy without credit checks or loan applications represents a significant advantage for Macon residents facing financial emergencies. Policy loans typically offer competitive interest rates compared to personal loans or credit cards, with flexible repayment terms that don’t require monthly payments. While unpaid loans will reduce the death benefit, this tradeoff often proves worthwhile when immediate access to funds becomes necessary. For more information, consider reading about why universal life insurance is gaining popularity.

Many Macon policyholders also appreciate that accessing their cash value through loans doesn’t trigger the tax consequences that might come from liquidating other investments. This tax efficiency makes universal life policies a practical source of funds for major life expenses like home improvements, business opportunities, or educational costs.

4. Ability to Adjust Coverage as Life Changes

Universal life insurance offers Macon residents remarkable flexibility to modify their coverage as their circumstances evolve. Policyholders can increase their death benefit (subject to insurability) when family responsibilities grow—perhaps after having children or taking on care for aging parents. Conversely, coverage can be reduced when financial obligations diminish, such as after paying off a mortgage or when children become financially independent. This adaptability ensures your insurance investment remains aligned with your actual protection needs throughout your lifetime.

5. Estate Planning Benefits for Macon Families

For Macon’s more affluent residents, universal life insurance provides valuable estate planning benefits by creating an immediate source of liquidity to cover estate taxes and settlement costs. The death benefit passes income-tax-free to beneficiaries and can be structured to remain outside the probate process, allowing for a faster and more private transfer of wealth to the next generation. For more information, consider exploring final expense insurance quotes in Macon to better understand your options.

Universal life policies can also be used in conjunction with trusts to create sophisticated estate planning strategies that protect family wealth from excessive taxation. Macon attorneys and financial advisors frequently recommend these policies as cornerstones of comprehensive estate plans, particularly for business owners, real estate investors, and professionals with significant assets to protect and transfer.

Who Should Consider Universal Life Insurance in Macon GA

“Universal Life Insurance in California …” from www.thebfis.com and used with no modifications.

Universal life insurance isn’t the right solution for everyone in Macon, but certain demographics and financial situations make it particularly appropriate. Understanding whether this type of coverage aligns with your specific circumstances can help you make a more informed decision about your insurance portfolio.

Macon residents with complex financial situations or multiple insurance objectives often find universal life policies offer the versatility they need. Rather than purchasing separate products for death benefit protection, retirement supplementation, and estate planning, universal life can potentially address all these needs within a single policy framework.

Ideal Candidates Based on Financial Goals

Universal life insurance typically works best for Macon residents who have already established a solid financial foundation. This includes having an emergency fund, contributing to retirement accounts, and addressing short-term debts. Once these basics are in place, universal life can serve as a complementary financial tool that provides both protection and accumulation benefits.

Business owners represent one of the largest groups of universal life policyholders in Macon. The policy’s cash value can serve as a business asset on the balance sheet, while the death benefit can fund buy-sell agreements or key person replacement costs. Many Macon entrepreneurs also appreciate the policy’s ability to serve as a supplemental retirement funding vehicle when traditional qualified plans like 401(k)s reach contribution limits.

Age Considerations: When to Start Your Policy

While universal life insurance can be purchased at virtually any age, most Macon insurance professionals recommend securing coverage during your 30s, 40s, or early 50s. This timing balances affordable premiums (which increase with age) with the appropriate window for cash value accumulation. Starting a policy during these prime earning years allows sufficient time for meaningful cash value growth while securing coverage when you’re likely to be in good health and qualify for preferred rates.

Common Universal Life Insurance Options in Macon

“Universal Life Insurance – Definition …” from www.wallstreetmojo.com and used with no modifications.

Macon insurance providers offer several variations of universal life insurance, each designed to address specific financial objectives and risk tolerances. Understanding the differences between these policy types can help you select the option that best aligns with your personal financial goals and comfort level with investment risk. For those in Macon, it’s also important to consider the top reasons to get final expense insurance quotes to complement your universal life insurance plan.

Indexed Universal Life: Market-Linked Growth Without Market Risk

Indexed universal life (IUL) policies have become increasingly popular among Macon residents seeking growth potential without direct market exposure. These policies link their cash value growth to the performance of market indexes like the S&P 500, but with built-in protections against market losses. When the index performs well, the cash value grows at a rate determined by the policy’s participation rate and cap. When the index performs poorly, the policy’s floor (typically 0-1%) prevents the cash value from decreasing due to market losses.

For conservative Macon investors who want potential returns higher than traditional fixed universal life but aren’t comfortable with the volatility of variable policies, indexed universal life offers an attractive middle ground. Many local insurance professionals report that IUL policies now represent the fastest-growing segment of the universal life market in Middle Georgia.

- Participation in index gains up to a specified cap (typically 8-14%)

- Protection against market losses through guaranteed floor rates

- No direct investment in the market, meaning less volatility

- Various indexing strategies and crediting methods to choose from

- Potential for higher long-term cash value growth compared to fixed universal life

Many Macon financial advisors recommend indexed universal life for clients who want their insurance policy to serve dual purposes: providing death benefit protection while also offering reasonable growth potential for retirement supplementation or other long-term goals. The policy’s combination of growth opportunity and downside protection makes it particularly suitable for Macon’s growing professional class.

Variable Universal Life: Higher Risk, Higher Reward Potential

Variable universal life (VUL) policies represent the highest-risk, highest-potential-reward option available to Macon residents. These policies allow policyholders to invest their cash value in a variety of subaccounts similar to mutual funds, covering different asset classes including stocks, bonds, and money market instruments. Unlike indexed universal life, VUL policies provide direct market exposure, meaning the cash value can decrease during market downturns but may also experience more substantial growth during bull markets. For more information, check out the top reasons for insurance quotes in Macon, GA.

This direct market participation makes VUL policies appropriate for financially sophisticated Macon residents with higher risk tolerance and longer time horizons. Many local professionals in medicine, law, and technology find VUL policies attractive for their potential to accumulate significant cash value over time. The ability to select and manage subaccount allocations also appeals to those who prefer a more hands-on approach to their investments, including the portion contained within their life insurance.

However, Macon insurance advisors typically recommend VUL policies only for clients who already have a diversified investment portfolio and understand the implications of market volatility. The higher fees associated with these policies can also reduce returns, making them less suitable for those primarily focused on death benefit protection rather than cash value accumulation.

Guaranteed Universal Life: The “Sure Thing” Option

Guaranteed universal life (GUL) policies offer Macon residents the permanent protection of universal life with significantly more certainty and less focus on cash value accumulation. These policies essentially function as “lifetime term insurance,” providing a guaranteed death benefit and premium schedule that won’t change as long as you make the required payments. While GUL policies do technically build cash value, they’re designed to maintain just enough to support the policy rather than serve as a significant accumulation vehicle.

For Macon residents primarily concerned with securing permanent death benefit protection at the lowest possible cost, GUL presents an attractive option. These policies typically cost more than term insurance but significantly less than cash value-focused universal life policies. Many empty-nesters and retirees in Middle Georgia choose GUL for estate planning purposes, ensuring beneficiaries receive a tax-free death benefit without paying for cash value features they don’t need.

The trade-off for this guaranteed protection and lower cost is the minimal cash value accumulation and reduced flexibility compared to other universal life variants. Macon insurance professionals often recommend GUL for clients seeking permanent coverage who have already established other retirement savings vehicles and don’t need their insurance to double as an investment tool. For those interested in understanding more about final expense options, getting final expense insurance quotes in Macon GA can provide additional insights.

Frequently Asked Questions

When considering universal life insurance in Macon, many residents share common questions about how these policies work and whether they’re appropriate for their specific situations. The following addresses the most frequent inquiries received by Macon insurance professionals regarding universal life coverage.

Understanding these fundamentals can help you approach conversations with local insurance agents more confidently and make more informed decisions about your coverage options. Always remember that while general guidelines apply, your personal financial situation may warrant customized recommendations.

How much does universal life insurance typically cost in Macon, GA?

Universal life insurance costs in Macon vary considerably based on several factors, with age and health being the most significant determinants. For a healthy 40-year-old Macon resident, monthly premiums might range from $100-300 for a policy with a $250,000 death benefit, depending on the specific universal life variant and design. Coverage amounts of $500,000 or $1 million would proportionally increase these costs. Indexed and variable policies typically command higher premiums than fixed universal life due to their additional features and growth potential.

Other factors affecting universal life premiums in Macon include gender (women generally pay less than men due to longer life expectancy), smoking status (smokers may pay 2-3 times more), occupation (higher-risk jobs increase rates), and family health history. Many Macon insurance providers offer preferred rates to applicants who demonstrate excellent health metrics including normal blood pressure, healthy BMI, and favorable cholesterol levels. Some companies also consider lifestyle factors like regular exercise patterns when determining premium rates. For those interested in learning more, here are the top reasons you need to get final expense insurance quotes in Macon, GA now.

Can I convert my term life policy to universal life insurance?

Many term life policies sold in Macon include conversion provisions that allow policyholders to convert to permanent coverage, including universal life, without providing new evidence of insurability. This feature proves particularly valuable if your health has declined since purchasing your original term policy. Conversion options typically specify a deadline by which you must exercise this right, often the end of the term period or a specific age (such as 65 or 70). When converting, your premiums will increase to reflect the permanent nature of the coverage, but they’ll be based on your original health classification rather than your current condition.

What happens if I miss premium payments on my universal life policy?

Missing premium payments on a universal life policy in Macon doesn’t necessarily mean your coverage will lapse immediately. When premiums go unpaid, the insurance company typically draws from your policy’s cash value to cover the cost of insurance and administrative expenses. Your coverage remains in force as long as sufficient cash value exists to cover these costs. However, consistent premium underpayment will eventually deplete your cash value, potentially resulting in policy termination if the situation isn’t addressed.

Many Macon insurance providers offer grace periods (typically 30-60 days) during which you can make up missed payments without penalties. Some policies also include provisions for automatic premium loans that borrow against the cash value to pay premiums when payments are missed. Understanding your specific policy’s provisions regarding missed payments is crucial, as these details vary significantly between carriers and policy designs.

How is the cash value in universal life insurance taxed?

For Macon residents, the cash value within a universal life policy grows tax-deferred, meaning no income taxes are due on the earnings as they accumulate. This tax-advantaged growth represents one of the policy’s most significant benefits compared to taxable investments. When accessing cash value through withdrawals, you can typically withdraw up to your “basis” (the total premiums paid) tax-free. Withdrawals exceeding your basis may be subject to income taxation.

Policy loans offer another potentially tax-advantaged way to access cash value. Under current tax law, loans against your policy are not considered taxable income as long as the policy remains in force. However, if the policy lapses or is surrendered with an outstanding loan, the loan amount may become taxable. Macon insurance professionals often recommend consulting with a tax advisor before implementing strategies that involve significant policy loans or withdrawals to ensure compliance with current tax regulations.

Can I borrow against my universal life insurance policy?

Yes, Macon policyholders can borrow against the cash value of their universal life insurance policies once sufficient value has accumulated. These policy loans feature several advantages compared to conventional loans: no credit check is required, loan approval is virtually automatic, repayment schedules are flexible, and interest rates are often lower than those for personal loans or credit cards. The borrowed amount, plus interest, is deducted from the death benefit if not repaid before the insured’s passing.

While policy loans offer convenient access to funds, they should be approached cautiously. Unpaid loan interest can compound over time, potentially eroding your death benefit or even causing policy lapse if the loan plus interest eventually exceeds the cash value. Many Macon insurance advisors recommend establishing a systematic repayment plan when taking policy loans to maintain the long-term integrity of your coverage.

For Macon residents seeking comprehensive information about universal life insurance options tailored to their specific needs, consulting with a qualified insurance professional who understands the local market can provide valuable guidance. These flexible policies offer unique advantages for those seeking lifetime coverage with built-in financial versatility, especially when structured properly to align with your long-term financial objectives. For more insights, explore the top reasons to get final expense insurance quotes in Macon, GA.

Have Questions About Coverage?

If you’re comparing options or trying to understand what makes the most sense for your situation, Ranwell Insurance is available to help clarify your next step.

Call (855) 508-5008 for guidance tailored to your needs, or explore our life insurance calculators to estimate coverage and budget ranges.