Key Takeaways

- Georgia’s free look period gives you 10 days to review and cancel a new life insurance policy with a full refund

- This consumer protection is mandatory in Georgia and all 50 states, ensuring you’re not locked into a policy you don’t understand

- During this period, you can thoroughly review your policy’s terms, coverage amounts, and premium obligations without financial risk

- Your free look period begins when you physically receive your policy documents, not when you apply or make your first payment

- Canceling during the free look period leaves no negative mark on your insurance record, unlike cancellations after this window closes

Georgia’s Free Look Period Gives You Time to Review Your Life Insurance

“Life Insurance Policies …” from www.youtube.com and used with no modifications.

When you purchase life insurance from a trusted agent like Ranwell Insurance in Georgia, you’re making a significant financial decision that could impact your family for decades. That’s why Georgia law provides a safety net known as the “free look period.” This protection gives you valuable time to review your new policy without commitment, ensuring you’re completely comfortable with your coverage before it becomes binding.

The free look period serves as a cooling-off period that allows you to thoroughly examine the details of your life insurance contract after receiving it. If you find the policy doesn’t meet your needs or expectations for any reason whatsoever, you can cancel it during this window and receive a complete refund of any premiums paid. This consumer protection feature applies to all types of life insurance policies sold in Georgia, including term life, whole life, universal life, and variable life insurance.

Many Georgians don’t realize this protection exists until after they’ve purchased a policy, and some insurance agents may not emphasize this right during the sales process. Understanding how the free look period works can give you confidence when shopping for life insurance, knowing you have time to make an informed decision without financial penalty.

What Is a Free Look Period?

The free look period is a state-mandated timeframe during which a new life insurance policyholder can cancel their policy and receive a full premium refund with no questions asked. Think of it as a risk-free trial period for your life insurance coverage. This provision is required by Georgia insurance regulations and exists to protect consumers from high-pressure sales tactics or buyer’s remorse after purchasing a complex financial product.

What makes the free look period particularly valuable is that you don’t need to provide a specific reason for cancellation. Whether you found a better rate elsewhere, discovered terms you weren’t comfortable with, or simply changed your mind, you have the absolute right to cancel during this period without penalty. This stands in stark contrast to cancellations after the free look period ends, which may result in surrender charges or only partial refunds depending on the policy type.

Insurance companies are required by law to explain this provision clearly in your policy documents. You’ll typically find this information on the policy’s cover page or within the first few pages of your contract. The language will specify exactly how many days you have to review the policy and the procedure for cancellation if you choose to exercise this right. For more details, you can read about the free look period in life insurance policies.

10-30 Day Window to Cancel Without Penalty

In Georgia, the minimum free look period mandated by state law is 10 days. This means Georgia residents have at least 10 full days to review their new life insurance policy and decide whether to keep it or cancel for a full refund. The clock starts ticking from the day you physically receive your policy documents, not from the date of application or when you make your first premium payment. For more details, you can read about what is the free look period in life insurance policies.

While Georgia requires a minimum 10-day window, many insurance companies voluntarily extend this period to 20 or even 30 days as a customer service benefit. Some insurers offer standardized free look periods across all states where they operate, meaning you might receive more than the Georgia minimum. If you’re comparing policies from different companies, the length of the free look period is worth considering as part of your decision process.

Full Premium Refund Guarantee

The full premium refund guarantee is one of the most important aspects of Georgia’s free look provision. If you decide to cancel your policy during this window, the insurance company must refund 100% of any premiums you’ve paid, with no deductions or fees. For standard term life insurance policies, this is straightforward—you’ll receive exactly what you paid. For more complex products like variable life insurance policies, Georgia regulations specify that you’ll receive either the premium paid or the current account value, depending on which is stated in your contract.

Insurance companies in Georgia must process your refund promptly after receiving your cancellation request. Most insurers will issue the refund within 7-10 business days, using the same payment method you used for the premium. If you paid by check or bank transfer, you’ll typically receive a check in the mail for the full amount. Some companies may require you to return the original policy documents before processing your refund, so be prepared to mail these back if requested.

It’s important to note that this full refund guarantee is specifically tied to the free look period. Once this window expires, cancellation terms become much less favorable, often resulting in little to no refund depending on your policy type and how long you’ve held it. This stark difference underscores why taking full advantage of your free look period is so crucial for Georgia insurance buyers.

Why Free Look Periods Exist in Life Insurance

“Axis Max Life Insurance” from www.axismaxlife.com and used with no modifications.

Free look periods were introduced as a consumer protection measure after regulators identified patterns of misleading sales practices in the insurance industry. Prior to these protections, some consumers found themselves locked into complex, long-term financial products they didn’t fully understand. Georgia, like other states, implemented these provisions to ensure consumers have adequate time to review their purchase without pressure.

Life insurance policies are complex legal contracts with terms that can span decades. Even educated consumers may find it difficult to fully grasp all provisions during the application process. The free look period acknowledges this complexity by giving you time to review the actual policy document, perhaps with the help of a financial advisor or attorney, before making a final commitment.

Another important purpose of the free look period is to balance the information asymmetry that naturally exists between insurance companies and consumers. Insurance providers have teams of actuaries, lawyers, and product specialists who create these policies, while most consumers purchase life insurance only a few times in their lives. This mandated review period helps level the playing field by giving you time to become more informed about exactly what you’ve purchased. If you’re considering your options, you might wonder which is the better option and why: term or whole life insurance.

What You Should Review During Your Free Look Period

Your free look period provides a critical opportunity to thoroughly examine your policy, and there are several key elements you should scrutinize carefully. Start with the death benefit amount and make sure it matches what you applied for and what you need to protect your loved ones. Double-check that all beneficiary information is accurate, including names and relationships, as errors here could cause significant problems for your family later.

Review the premium schedule in detail, confirming both the initial amount and how it might change over time. Some policies, particularly universal life and whole life insurance, may have premiums that increase significantly in later years. Make sure you understand exactly what you’ll be paying both now and in the future, and verify that these amounts align with what your agent discussed during the sales process.

Policy exclusions and limitations deserve special attention during your review. Look for any clauses that might limit or void coverage under certain circumstances. Common exclusions in Georgia policies might include death by suicide within the first two years of coverage, death while participating in certain high-risk activities, or limitations related to pre-existing conditions that weren’t disclosed on your application. Understanding these exclusions now can prevent devastating surprises for your beneficiaries later.

Documents to Review During Your Free Look Period

• Policy declaration page (coverage amounts and basic terms)

• Premium schedule (current and future payment obligations)

• Beneficiary designations (names and percentage allocations)

• Exclusions and limitations (circumstances where coverage might not apply)

• Rider details (additional coverages you may have purchased)

• Cash value growth projections (for permanent policies only)

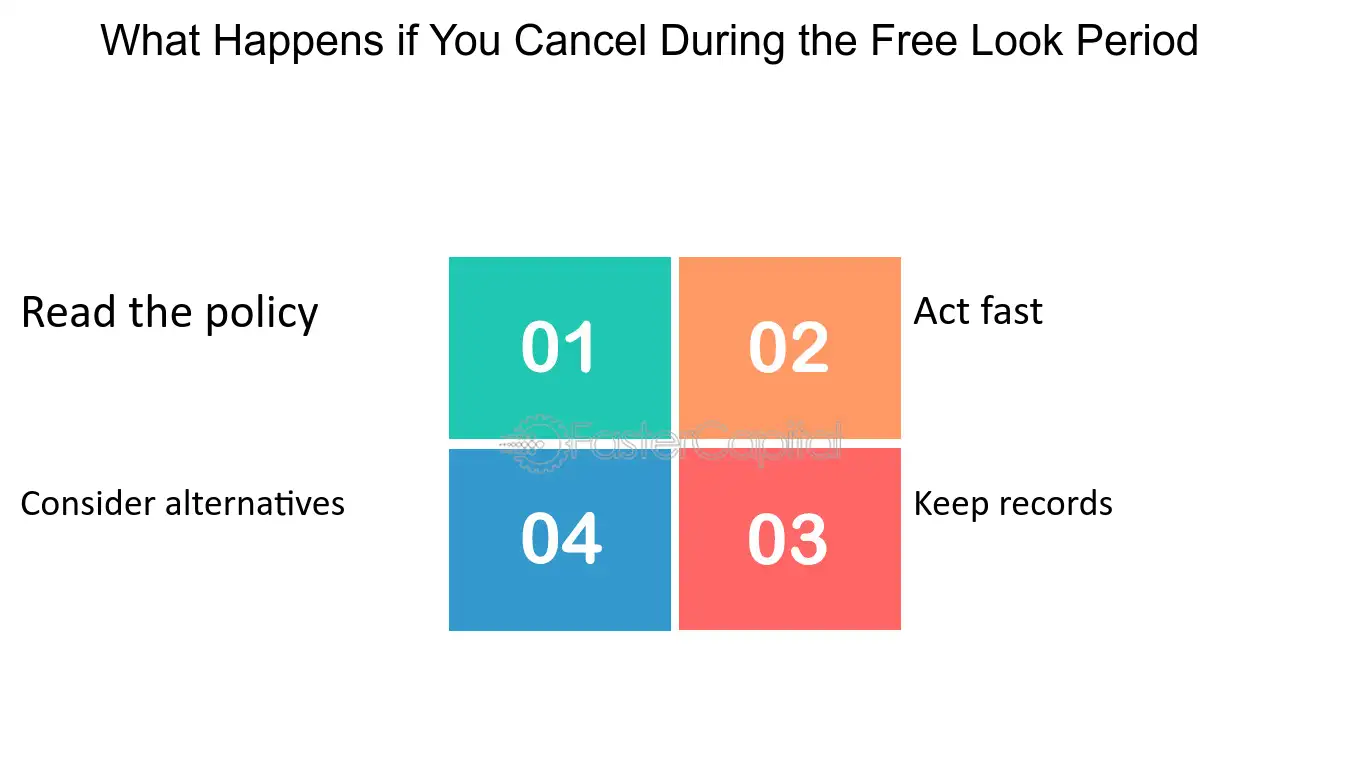

How to Cancel Your Policy During the Free Look Period

If you decide to cancel your policy during Georgia’s free look period, the process is straightforward but must be done correctly to ensure your rights are protected. First, notify your insurance company in writing of your decision to cancel. While some insurers may accept cancellation requests by phone, sending a written notice provides documentation of your request within the required timeframe. Your cancellation letter should include your full name, policy number, the date you received the policy, and a clear statement that you wish to cancel under the free look provision.

Common Reasons People Cancel During Free Look

“Cancel During The Free Look Period …” from fastercapital.com and used with no modifications.

Understanding why others cancel their policies during the free look period can help you determine if you should consider doing the same. The most common reason Georgians exercise this right is discovering they can get similar or better coverage at a lower price from another insurer. If you continue shopping after submitting an application, you might find more competitive rates that better fit your budget, making cancellation a financially sound decision.

Another frequent reason for cancellation is realizing the policy doesn’t provide the specific benefits or coverage you thought it would. For instance, you might discover limitations on payouts for certain causes of death or find that the cash value accumulation in a permanent policy works differently than you understood. These misunderstandings often stem from complex policy language or insufficient explanation during the sales process.

Personal financial changes can also prompt cancellations during the free look period. If your financial situation changes unexpectedly between application and policy delivery—such as a job loss or major expense—you might need to reconsider the affordability of the premiums. Using the free look period in this situation allows you to step back without financial penalty while you reassess your budget and coverage needs.

- Finding lower premiums with another insurance carrier

- Discovering policy exclusions or limitations not initially understood

- Experiencing unexpected financial changes affecting affordability

- Realizing the coverage amount is insufficient or excessive

- Identifying errors in how the policy was set up (wrong beneficiaries, riders, etc.)

What Happens After Your Free Look Period Ends

Once your free look period expires in Georgia, your policy becomes fully in force, and the cancellation terms change significantly. After this window closes, canceling your policy typically means surrendering it according to the contract terms, which rarely includes a full premium refund. For term life policies, you’ll generally forfeit any premiums paid. For permanent policies with cash value, you may receive the surrender value, which is often substantially less than what you’ve paid in premiums during the early years.

The post-free look cancellation process also becomes more complex. While you can still cancel your policy at any time, you’ll need to follow specific procedures outlined in your contract, which may include submitting specific forms and waiting for approval. Some policies may also include surrender charges that further reduce any potential refund, especially if you cancel within the first several years of coverage. For more information on why life insurance is important, read our article on financial security in Georgia.

However, even after your free look period ends, you still have certain options if you’re unhappy with your policy. You might be able to modify your coverage, convert a term policy to permanent insurance, or reduce your death benefit to lower your premiums instead of canceling outright. These alternatives may provide better financial outcomes than cancellation while still addressing your concerns about the original policy terms.

Frequently Asked Questions

Can I extend my free look period in Georgia?

Generally, the free look period in Georgia cannot be extended beyond the statutory minimum of 10 days or whatever longer period your insurer provides. This timeframe is fixed by state regulation and insurance company policy, and exceptions are rarely granted. If you need more time to review your policy, your best approach is to start your review immediately upon receiving your documents and prioritize the most important elements.

In certain limited circumstances, such as if you were hospitalized during the free look period or experienced another serious hardship that prevented policy review, some insurers may consider a discretionary extension. This is not guaranteed by law, however, and would be entirely at the company’s discretion. If you find yourself approaching the end of your free look period and still have concerns, contact your insurance agent or the company’s customer service department immediately to discuss your situation. For more insights on why life insurance is important, you can read about financial security in Georgia.

- Begin reviewing your policy immediately upon receipt

- Focus on coverage amounts, premiums, and exclusions first

- Contact your insurer before the period expires if you need clarification

- Document all communications if you’re requesting special consideration

If you’re concerned about the length of your free look period when shopping for life insurance in Georgia, ask potential insurers about their specific timeframes before applying. Some companies voluntarily offer extended periods of 20 or 30 days, which could give you the additional time you need for a thorough review.

Will canceling during the free look period affect my credit score?

Canceling your life insurance policy during the free look period will not affect your credit score in any way. Insurance companies do not report free look cancellations to credit bureaus, and exercising this consumer protection right has no impact on your credit history. You can cancel with complete confidence that your credit standing will remain unchanged. If you’re unsure about whether to maintain your policy, you might consider reading more about why life insurance is important.

Furthermore, canceling during this period won’t create any negative record in the insurance industry databases that companies use to evaluate applicants. Unlike cancellations for non-payment or misrepresentation, which might be reported to the Medical Information Bureau (MIB) or similar industry databases, free look cancellations are considered a normal consumer right and don’t generate any adverse reports. This means your ability to obtain insurance coverage in the future won’t be compromised in any way by using your free look rights.

What happens if I’ve already made a claim during the free look period?

In the extremely unlikely event that you need to file a claim during the free look period (such as if the insured person passes away shortly after the policy is issued), the situation becomes more complex. Once a claim has been filed or benefits paid, you generally cannot exercise your free look cancellation rights for that policy. The contract would be considered “in force” and executed upon claim filing, effectively ending the free look provision. This is why the free look period is intended primarily as a review period before any claims activity occurs.

Are there any fees or charges that won’t be refunded?

Under Georgia insurance regulations, if you cancel during the free look period, you’re entitled to a full refund of all premiums paid with no penalties or deductions. This clean refund policy differs from some other states where insurers may deduct certain administrative costs or fees even during the free look period. For most traditional life insurance policies in Georgia, you’ll receive exactly what you paid, with no hidden charges retained by the insurer.

The only exception to this full refund policy might be for certain variable life insurance products where your premium has been invested in securities. In these cases, Georgia regulations and your specific contract will determine whether you receive your premium back in full or the current market value of your investment portion. Your policy documents will explicitly state which refund method applies to your specific contract. If you have a variable policy and are considering cancellation, review this section of your contract carefully or ask your agent to explain the refund calculation method.

Can I get another free look period if I modify my existing policy?

Generally, modifications to an existing life insurance policy do not trigger a new free look period in Georgia. The free look provision typically applies only to newly issued policies, not to riders, endorsements, or other changes to in-force coverage. This means if you add coverage, change beneficiaries, or make other adjustments to your policy after the initial free look period has expired, these modifications will not come with their own cancellation rights.

However, there is one important exception to this rule. If your existing policy is replaced entirely with a new policy—even from the same insurance company—the new policy will come with its own free look period. Insurance replacements are treated as new contracts under Georgia law, entitling you to all the same review rights you had with your original policy. This protection is particularly important since policy replacements sometimes occur due to aggressive sales tactics, and the new free look period gives you time to ensure the replacement truly benefits you.

When considering significant changes to your life insurance coverage, discuss with Ranwell Insurance whether the changes would constitute a new policy with new free look rights, or merely modifications to your existing coverage. Understanding this distinction can help you make more informed decisions about how to proceed with any proposed changes to your life insurance protection.

Policy Modifications vs. Policy Replacements

Modifications (No New Free Look): Adding riders, changing beneficiaries, adjusting death benefit amounts, changing payment schedules

Replacements (New Free Look Period): Converting term to permanent coverage, switching from one product type to another, changing to a different insurer

Understanding your free look period rights gives you confidence when purchasing life insurance in Georgia. This consumer protection ensures you’re never pressured into keeping a policy that doesn’t meet your needs or contain the terms you expected. Take full advantage of this review period by carefully examining your policy documents and asking questions about anything you don’t understand.

Contact Ranwell Insurance today @ (855) 508-5008 or ranwell.insurance@gmail for good old fashioned southern service that’s as personalized as your grandma’s peach or pecan pie recipes. We shop multiple carriers so you don’t have to — get your free, personalized quote today.